A company communicates its financial performance to its stakeholders through financial statements. Balance sheet is one of the five financial statements that a company provides. It presents a company’s financial position, i.e. its worth. In this article, we will understand what a balance sheet is, why you should analyse it, its contents and where to find it.

What is a Balance Sheet?

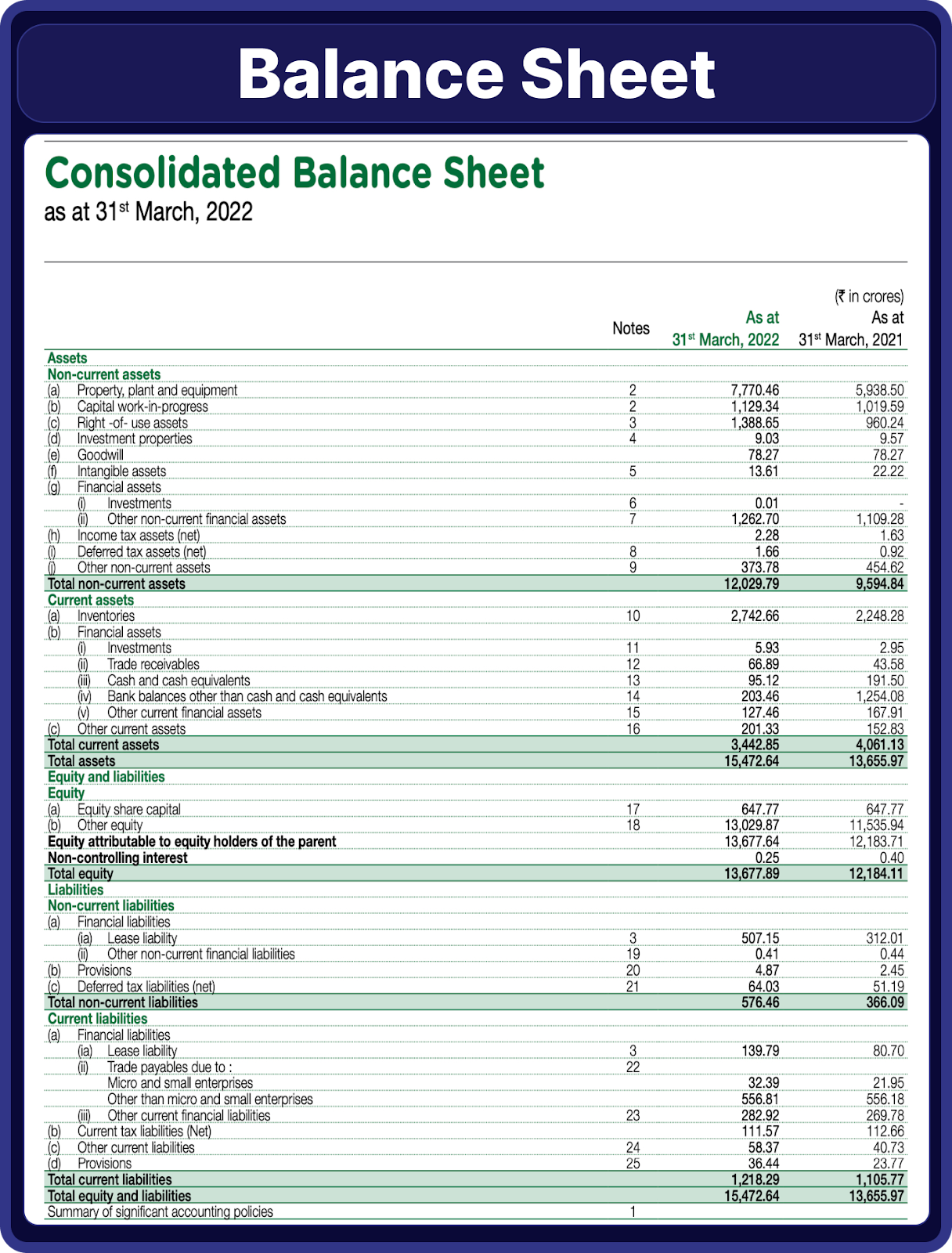

A balance sheet is a financial statement that shows the current financial position of an entity. The balance sheet provides information on a company’s resources (assets) and sources of capital (equity and liabilities/debt) at a given point in time. It shows the net worth of a company. Balance sheet is also known as a statement of financial position or statement of financial condition.

The balance sheet is based on the following equation:

Assets = Liabilities + Capital

Why Should You Analyse a Balance Sheet?

- A balance sheet contains all details regarding how much a company has and how much it owes to others, which can be used to calculate the company’s net worth.

- It shows the details of a company’s different assets and the value of each asset.

- A balance sheet shows the details of a company’s liabilities and how much it owes to others.

Where to Find the Balance Sheet?

You can find a company’s balance sheet from its annual report. An annual report is a company’s yearly report to shareholders, documenting its activities and finances of the previous financial year. It is a 300-400 page document containing all vital information about a company. It is the yearly official communication from the company. The annual report contains information regarding a company’s overall business outlook, industry outlook, financial statements, marketing content, and forward-looking statements.

Standalone vs Consolidated Financial Statements

Companies with subsidiaries have two sets of financial statements in their annual report:

- Standalone financial statements: They only include the financials of a company itself and do not include the financials of their subsidiaries.

- Consolidated financial statements: They include the financials of a company and its subsidiaries.

For example, let’s imagine that Company B is a subsidiary of Company A. The standalone financial statements of Company A will only include the transactions of Company A. Meanwhile, a consolidated financial statement includes the transactions of both Company A and Company B.

We always consider the consolidated financial statements because the business transactions of the subsidiary also affect its parent company, as the ownership lies with the company.

What are the Components of a Balance Sheet?

The main components and the structure of a balance sheet are:

There are two sections in a balance sheet: an asset section and an equity & liabilities section. Even though equity and liabilities are separate components, a balance sheet combines them into a single section named equity and liabilities. We will learn the different elements and their components by analysing the consolidated balance sheet of DMart.

1. Assets

Assets are anything of value that a company owns and controls. These are the resources available to a company. For example, a plant and machinery that the company uses to produce products is its asset. Assets are classified into two types:

Current Assets

Current assets are those assets held primarily for trading or expected to be sold, used up, or realized in cash within one year. This category also includes assets convertible into cash within one operating cycle. An operating cycle is the time period a company takes to convert its raw materials into finished goods. It includes cash and cash equivalents, inventories, short-term investments, etc.

- Inventories are physical products that will eventually be sold to a company’s customers.

- Financial Assets are liquid assets that get their value from a contractual right or ownership claim. Mutual funds, stocks, cash, etc, are financial assets.

- Investments represent the amount that a company has invested into various instruments that can be converted to cash within one year or one operating cycle.

- Trade Receivables refer to the amount that is yet to be received from customers for goods or services sold in credit.

- Cash and cash equivalents show the amount that a company has in the form of cash. It also includes the cash in a company’s bank accounts.

- Bank balances other than cash and cash equivalents show the amount of money in banks held as guarantees and commitments. These balances have restrictions on liquidity.

- Other current financial assets represent all other financial assets that the company holds.

- Other current assets include all the current assets which do not belong to the above categories.

Total current assets represent the sum of the values of all current assets.

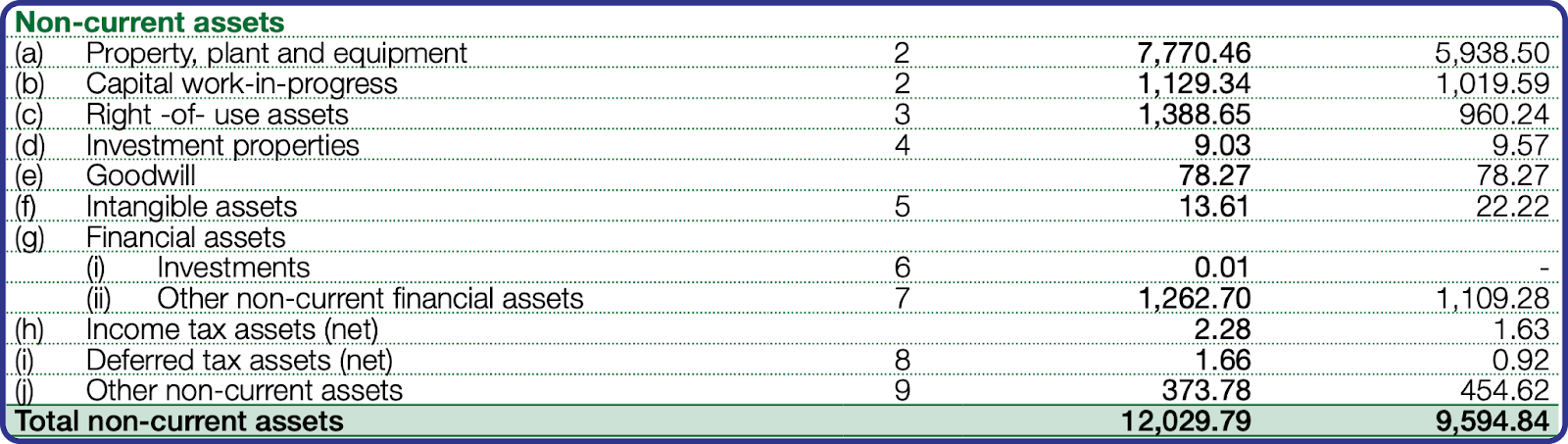

Non-Current Assets (Fixed Assets)

Non-current assets refer to assets not anticipated to be sold or used up within one year or one operating cycle (whichever is greater) of the business. There are two types of fixed assets:

Tangible assets, such as buildings and machinery, are physical assets that can be seen and touched.

Intangible assets are assets that cannot be seen or touched but are characterised by their impact and value, rather than physical presence. Assets like copyrights, patents, goodwill, etc are intangible assets. These assets are shown after deducting depreciation and amortization. Non-current assets include tangible and intangible assets, capital work in progress, investments, etc.

- Property, plant, and equipment represent the value of all the properties, plants, equipment, and machinery that a company owns.

- Capital work-in-progress is the value of tangible fixed assets that are under construction.

- Right-of-use assets are the assets that a company has leased and has the right to use.

- Investment properties are the properties that a company has invested in for purposes other than production. It includes properties that the company may buy for capital appreciation.

- Goodwill is a value addition to the company due to its reputation.

- Intangible assets are assets that do not have a physical form. It includes computer software, patent rights, etc.

- Financial assets under non-current investments are the value of financial assets such as stocks, bonds, debentures, etc that a company is planning to hold for more than one year.

- Income tax assets represent the amount that is to be received as tax refunds, rebates, etc

- Deferred tax assets represent any amount of tax that has been overpaid or paid in advance, which reduces the future tax liabilities of a company.

- Other non-current assets represent the value of all non-current assets that are not included in the above categories.

2. Liabilities

Liabilities are what the company owes. It represents the obligations of a company. Bank loans, money owed to creditors, etc are examples of liabilities. Liabilities are further classified into two types:

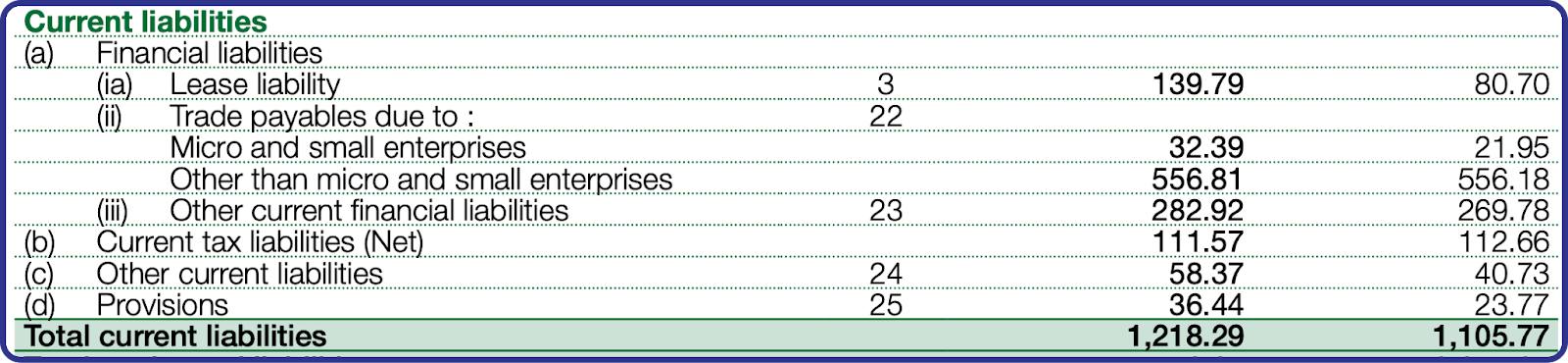

Current Liabilities

Liabilities expected to be settled within one year or one operating cycle of the business are categorised as current liabilities. An example is loans due for payment within one year.

- Financial liabilities are contractual obligations that require payment of cash.

- The lease liability is the amount paid for leases.

- Trade payables are the amount owed to creditors for credit purchases.

- Other current financial liabilities are current financial liabilities that are not included in the above categories.

- Current tax liabilities are the amount payable to tax authorities.

- Other current liabilities represent all the current liabilities that are not included in the above categories.

- Provisions in the current liabilities are the amount set aside from profit as provisions to meet future expenses. Warranty is an example of provision.

Non-Current Liabilities

Liabilities projected to be settled over one year or longer, or beyond one operating cycle of the business, are categorized as non-current liabilities. Non-current liabilities include loans with a repayment period of one year or more. It also includes bonds and debentures issued by a company to finance itself. All the items in this category are the same as items from current liabilities except for the duration, which is more than 1 year in the case of non-current liabilities.

Working capital is the surplus of current assets over current liabilities.

3. Equity

Equity represents the owners’ residual interest in a company’s assets after deducting its liabilities. It is commonly known as shareholders’ equity or owner’s equity. Equity is calculated by subtracting a company’s liabilities from its assets. Simply put, equity represents the amount invested by the shareholders of the company. It also includes reserves and surplus of the company. Surplus is the net profit that the company made.

Non-controlling interest is the equity of DMart’s subsidiaries, not owned by DMart.

In conclusion, a balance sheet tells us what the company is worth. This statement is indispensable for investors, creditors, and management to gauge a firm’s solvency and liquidity. Make sure to download the balance sheet of a company and try to understand what you learned here.