A company communicates its financial performance to all stakeholders through financial statements. The statement of profit and loss (P&L) or earnings statement is the first of five statements that a company provides. It presents a company’s financial result, i.e. profit or loss. In this article, we will understand what a statement of profit and loss is, why you should analyse it, its contents and where to find it.

What is a Statement of Profit & Loss?

A statement of profit and loss presents information on the financial results of a company’s business activities over a particular time (usually a quarter or year). It is also known as income statement, P&L statement, statement of operations and earnings statement. The income statement communicates how much revenue a company generated during a period and the costs incurred for generating that revenue.

The basic equation underlying the income statement is ‘Income – Expense = Profit’.

Where to Find Statement of Profit and Loss?

You can find the statement of P&L from the annual report of a company. An annual report is a company’s yearly report to shareholders, documenting its activities and finances of the previous financial year. It is a 300-400 page document containing all vital information about a company. It is the yearly official communication from a company. The annual report contains information regarding a company’s overall business outlook, industry outlook, financial statements, marketing content, and forward-looking statements.

You can download a company’s annual report from its website or other sources like screeners.

Standalone vs Consolidated Financial Statements

Companies with subsidiaries have two sets of financial statements in their annual reports: standalone financial statements and consolidated financial statements. Standalone financial statements only include the financials of a company itself and do not include the financials of its subsidiaries. On the other hand, consolidated financial statements include the financials of the company and its subsidiaries.

For example, let’s imagine that Company B is a subsidiary of Company A. The standalone financial statements of Company A will only include the transactions of Company A. Meanwhile, a consolidated financial statement includes the transactions of both Company A and Company B.

We always consider consolidated financial statements as the business transactions of the subsidiary also affect its parent company, as the ownership lies with the company.

Why Should You Analyse the Statement of P&L?

- To Understand Income Growth: The statement of profit and loss provides all details about the growth in a company’s revenue and income.

- To Study Expenses: Expenses and other areas where a company spends money can only be analysed from the income statement. We should also compare the expenses of a company to its peers to understand how efficiently it can create revenue.

- To Understand Profitability and Growth: It is necessary to understand the profitability of a business. The final result of the income statement is the profit/loss. Profitability is a measure of an organisation’s profit relative to its expenses. We should analyse the growth in revenue, profits and expenses to understand if the company is growing.

What are Notes to Accounts?

Notes to accounts, also known as footnotes or financial statement notes, are additional explanations, disclosures, and details provided in a company’s financial statements. They accompany the main financial statements (such as the balance sheet, income statement, and cash flow statement) to provide further context, explanations, and additional information that cannot be conveyed in the primary financial statements alone.

These notes help investors, analysts, and auditors to better understand the company’s financial performance and position. Notes to accounts typically cover topics like accounting policies, contingent liabilities, significant events, changes in accounting methods, and other relevant details to ensure transparency and compliance with accounting standards. They are an integral part of a company’s financial reporting and provide important context to interpret the numbers presented in the primary financial statements.

What are the Components of a Statement of Profit and Loss?

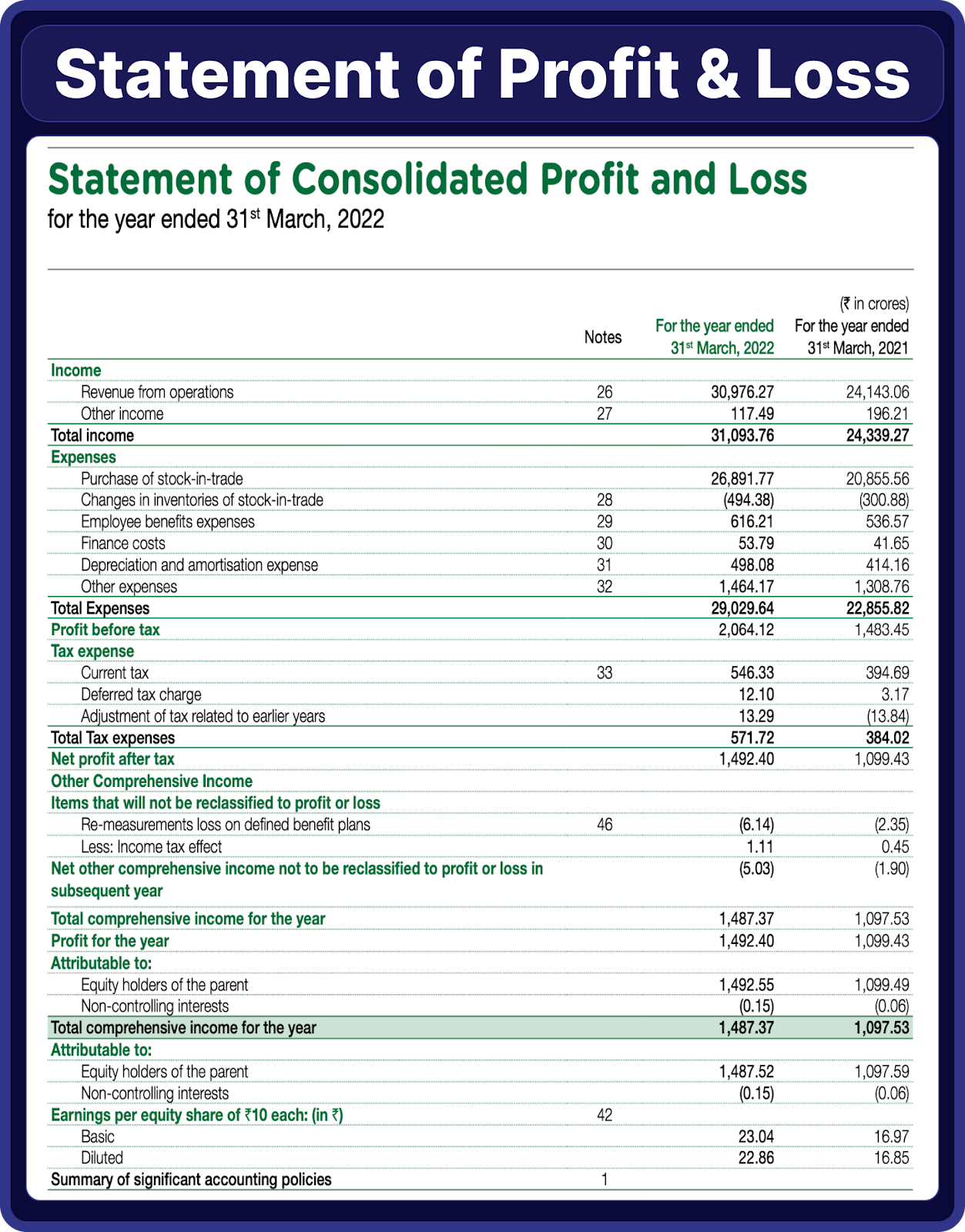

The main components and the structure of a statement of profit and loss are (we’ve taken the example of DMart here):

There are four columns in the income statement. They are particulars, notes, current year financials, and previous year financials. The particulars of the income statement are:

1. Income (Topline)

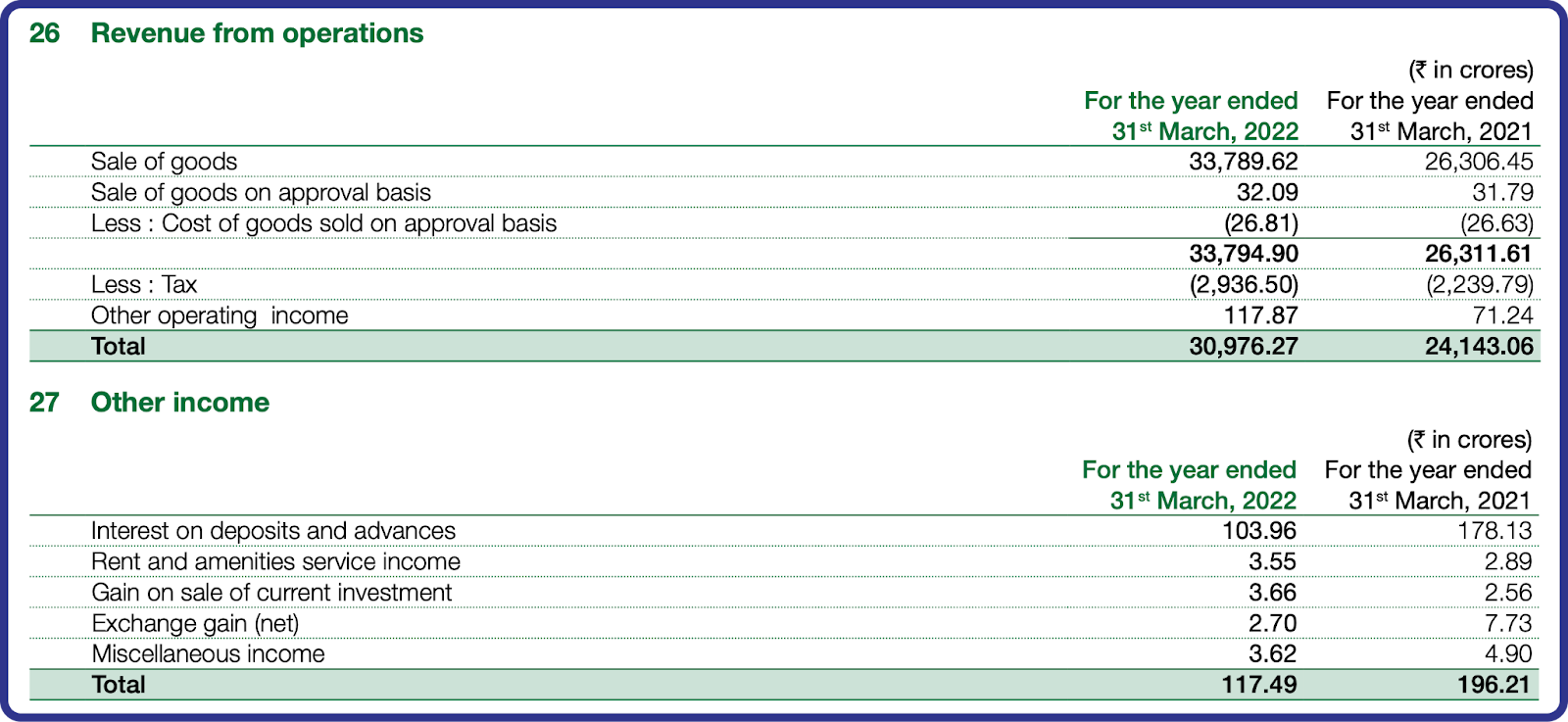

The first section in the income statement is income or topline. Revenue or turnover generally refers to the amount charged for the delivery of goods or services in the ordinary activities of a business.

- Revenue from operations is a company’s revenue from operating activities or its main activities (things a company does to bring its products and services to market).

- Other income is the income from non-operating activities (like investment income, gains or losses from foreign exchange, interest income, etc).

- Total Income is the sum of revenue from operations and other income.

Its respective notes give a detailed breakdown of revenue from operations and other income.

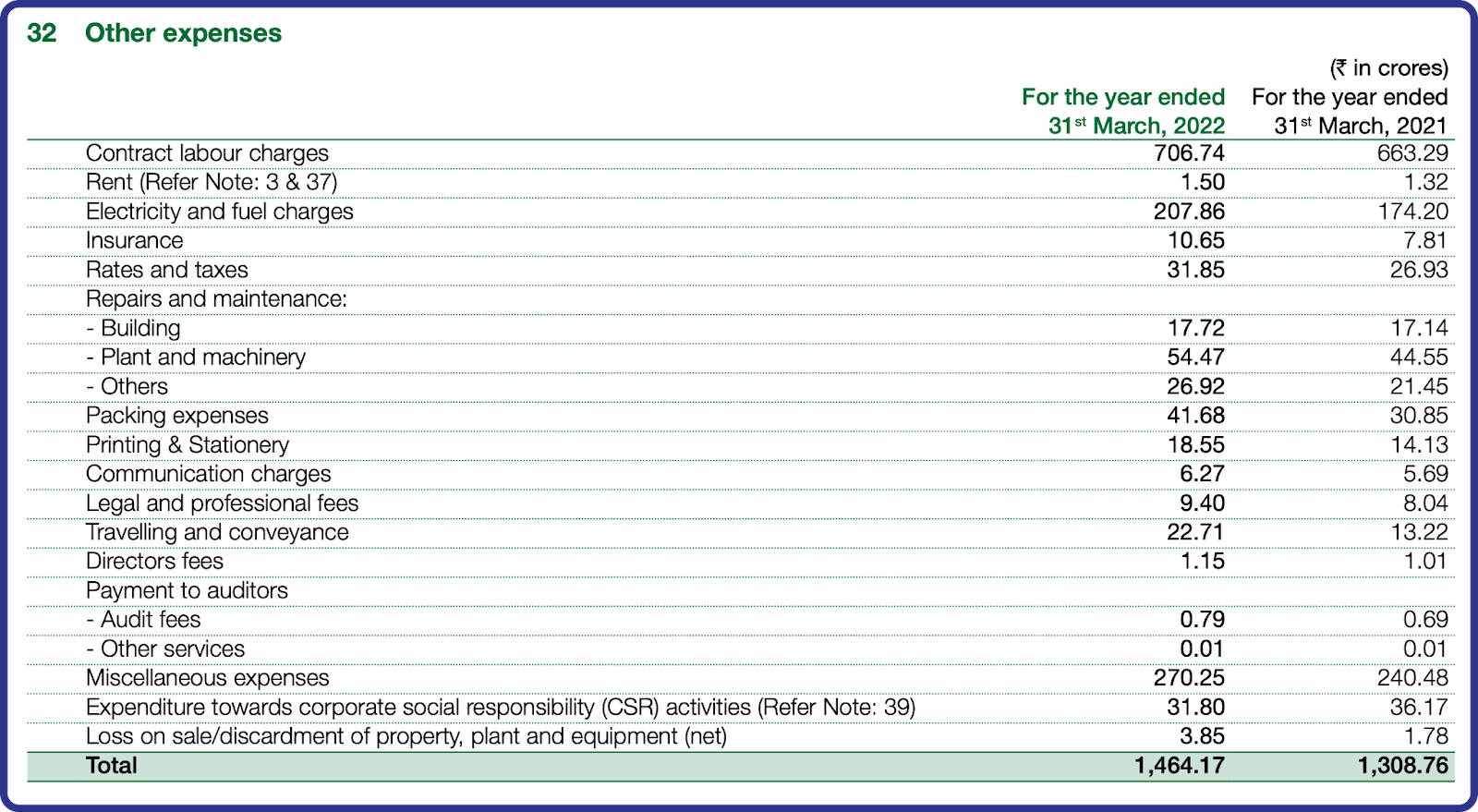

2. Expenses

Expenses reflect outflows, depletions of assets, and incurrences of liabilities in the course of the activities of a business.

- Purchase of stock-in-trade contains the expense incurred for the purchase of products that are to be sold and related expenses. Since DMart operates retail outlets, its major expense will be the purchase of stock.

- Changes in inventories of stock-in-trade are the difference between the amount of the last period’s ending inventory and the amount of the current period’s ending inventory.

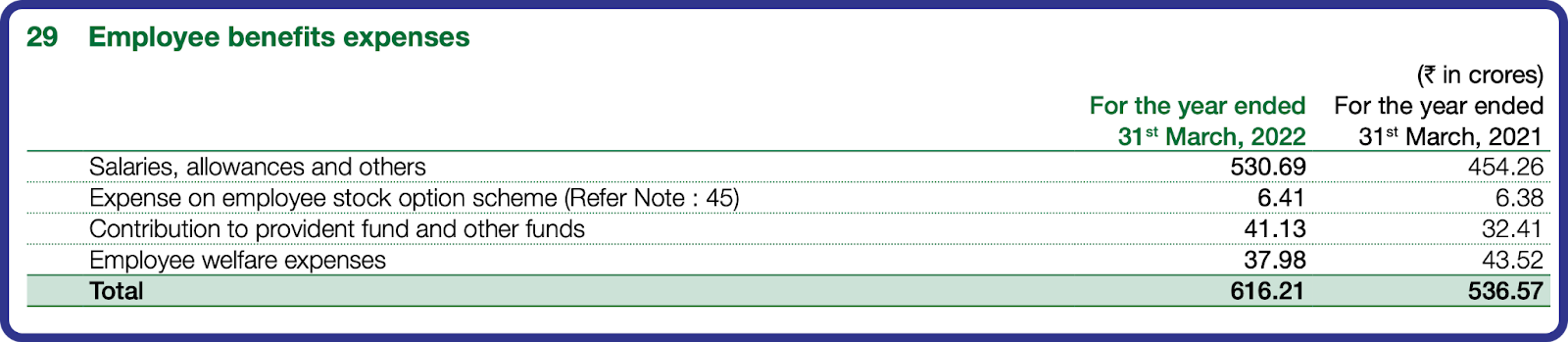

- Employee benefits expenses are the costs incurred for the benefit of employees. It contains salaries and wages, welfare expenses, etc.

- Finance costs refer to the cost, interest, and other charges involved in the borrowing of money to build or purchase assets.

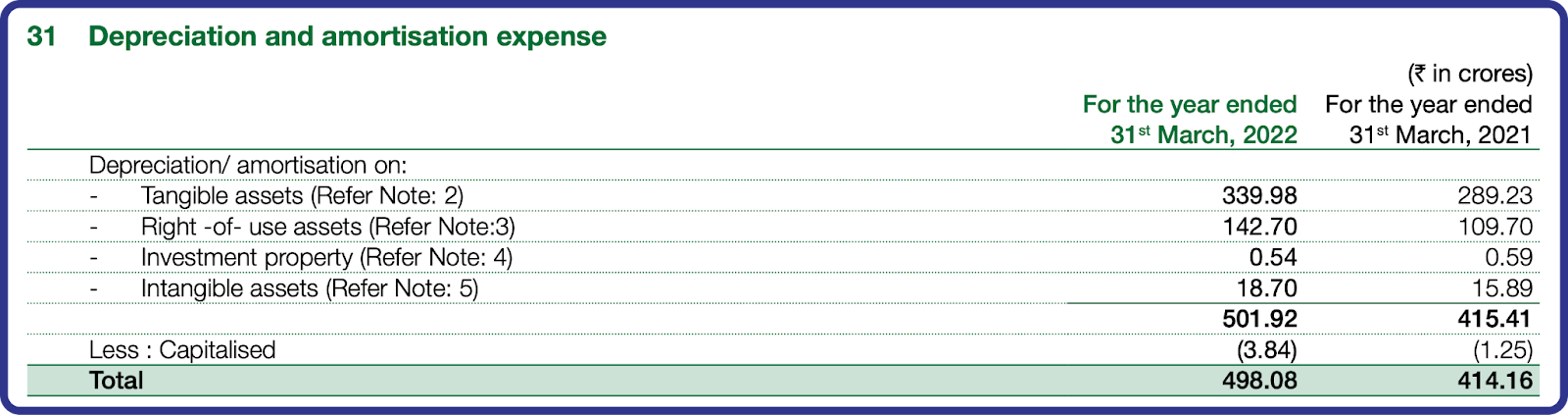

- Depreciation and amortization expenses are the expenses incurred due to the loss of value of assets. Depreciation is the reduction in the value of a tangible asset over time due to wear and tear. Amortization is the reduction in the value of intangible assets such as goodwill.

- Other expenses are all the expenses that do not fall within the above categories.

You can go through all the notes to accounts to view the split-up of each cost.

Total expenses are the sum of all the expenses.

3. Profit Before Tax (PBT)

Profit before tax is the difference between revenue and expenses, but before deducting tax liabilities. PBT = Total Income – Total Expenses.

4. Tax Paid

When a company makes profits, it must pay taxes to the government. This line provides comprehensive details on taxes. Meanwhile, notes to accounts provide in-depth information about all tax expenses. It is not necessary to analyse it.

5. Profit / Loss After Tax

Profit after tax (PAT) or bottom line represents the total profit earned after subtracting all expenses and taxes from revenue.

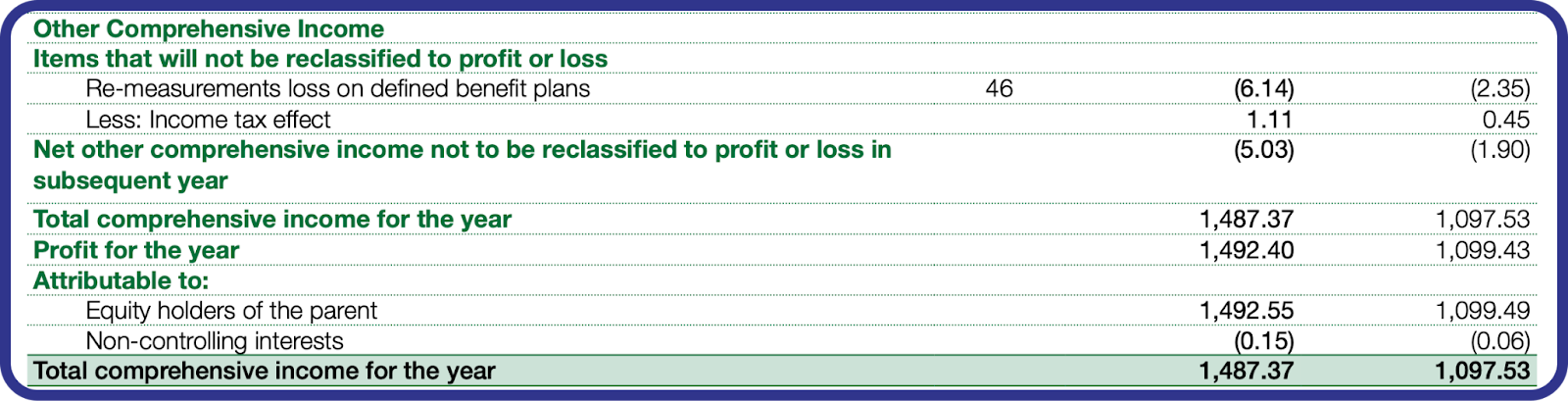

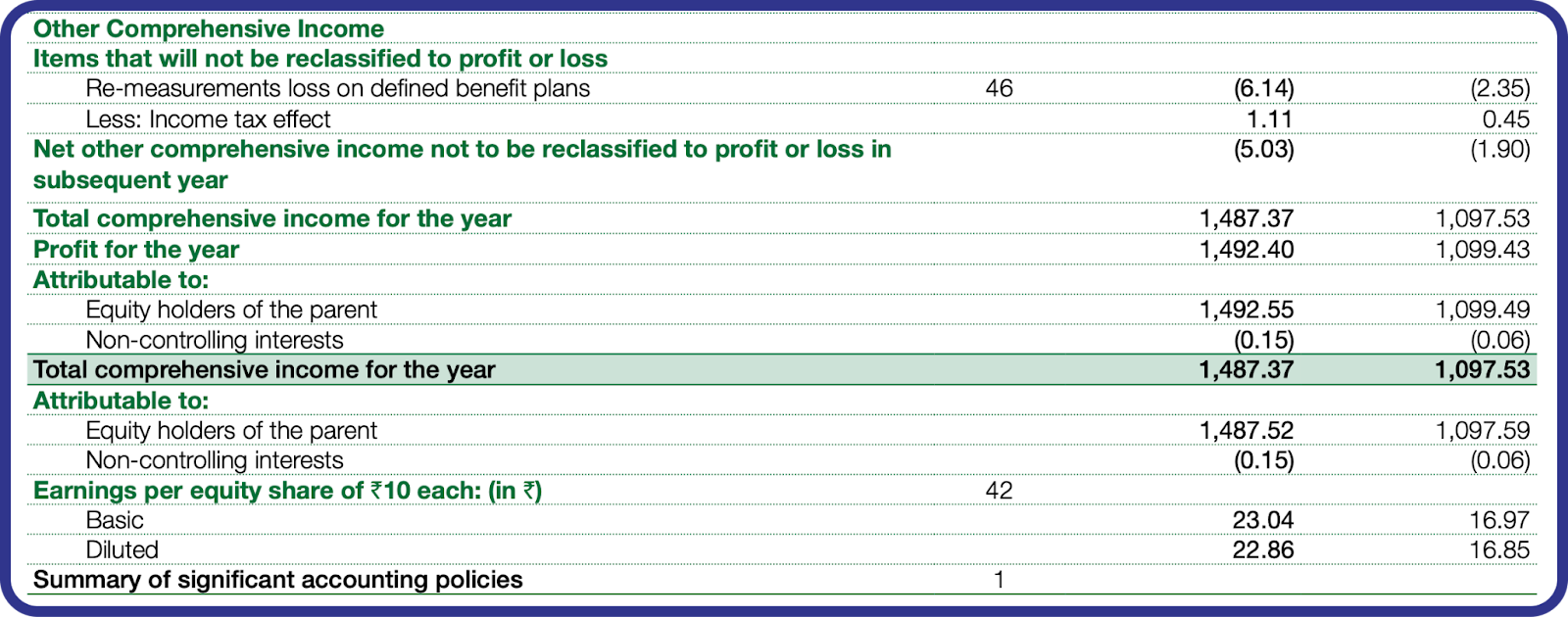

6. Other Comprehensive Income

In business accounting, revenues, expenses, gains, and losses that are yet to be realized and not included in the net income on an income statement are mentioned under other comprehensive income (OCI). It comprises both net income and other revenue and expense items excluded from the net income calculation.

Foreign currency translation adjustments, unrealised gains or losses on derivatives contracts accounted for as hedges, unrealised holding gains and losses on a certain category of investment securities, and certain costs of a company’s defined benefit post-retirement plans that are not recognised in the current period are the most common items treated as other comprehensive income. It is not necessary to analyse other comprehensive income.

7. Profit Attributable to Equity Holders of the Parent and Non-Controlling Interests

The profit after tax in the consolidated income statement includes the financials of the subsidiary companies as well. Meanwhile, non-controlling interest is the portion of a subsidiary company’s stock that is not owned by the parent corporation. It signifies the profit allocated to the other owners of a subsidiary company.

The profit attributable to equity holders of the parent is the profit allocated to the parent company itself.

8. Earnings Per Share (EPS)

Earnings per share is the monetary value of earnings per outstanding share of common stock for a company. It is a key measure of profitability and is commonly used to evaluate stocks. The higher the EPS, the better. EPS includes retained earnings and dividends. Basic and Diluted EPS are the two types of EPS in the financial statements.

Basic Earnings Per Share (EPS) is a financial metric that represents a company’s profit allocated to each outstanding common share. It is calculated by dividing the net income by the total number of common shares. Basic EPS provides a straightforward view of a company’s earnings on a per-share basis.

Diluted Earnings Per Share takes into account potential dilution from securities like stock options and convertible bonds. It assumes all such securities are exercised or converted, potentially increasing the number of shares outstanding. Diluted EPS is typically lower than basic EPS, as it considers the impact of potential future share issuances. If the Diluted EPS is higher than the basic EPS, then the diluted EPS will be the basic EPS.

In conclusion, a statement of profit and loss outlines a company’s revenues, expenses, and net profit for a specific time period. This statement is indispensable for investors, creditors, and management to gauge a firm’s profitability. Make sure to download the income statement of a company and try to understand what you learned here!