Most financial experts or ‘finfluencers’ teach people everything about long-term investing but miss out on one important topic: How much to invest? It might be because the answer to the question is highly subjective. The amount of money we invest every month varies according to different factors such as age, lifestyle, financial goals, etc. Even though this topic is highly subjective, we have created a financial planning calculator to answer the question “How much should you invest?”

The 50-30-20 Rule

As we discussed in the last chapter, we can use the 50-30-20 rule as a thumb rule to know how much to invest every month. This rule says that we should spend 50% of our total income on basic needs, 30% on our wants, and 20% on investments. However, not everyone can use this rule because income, expenses, lifestyle, and financial goals differ from person to person. To address this issue, our financial planning calculator provides a tailor-made solution for each individual.

How Can Our Excel Calculator Help You?

1. Retirement Goal Planning

It determines the corpus amount that you would need to retire comfortably, and how much to invest every month to achieve the goal. You have to input details like current age, retirement age, pre and post-retirement expenses, etc.

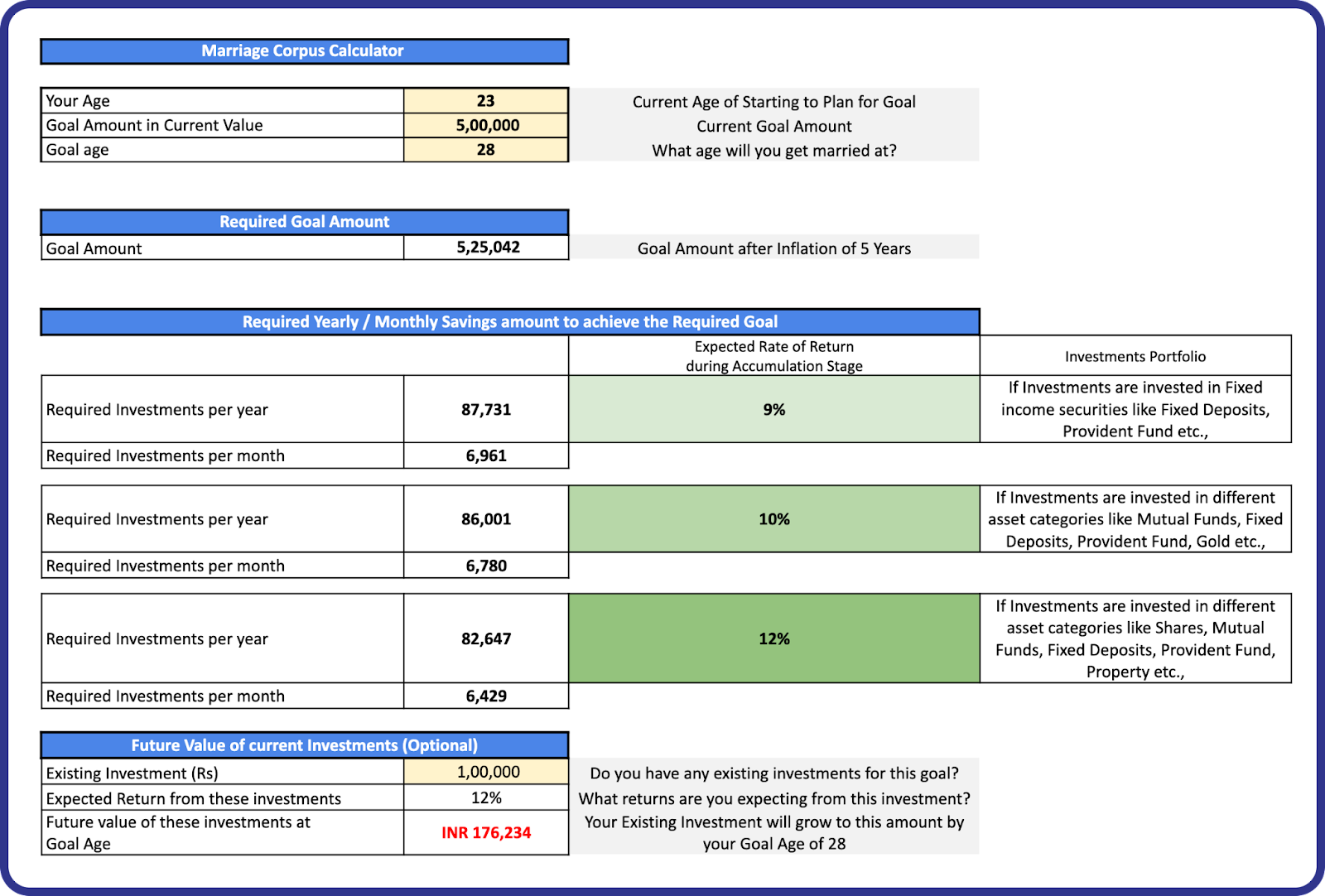

2. Marriage Goal Planning

You can calculate how much to invest every month to build a corpus to take care of your marriage expenses. Input how much it would cost in total if you were to marry today, your current age, and the age at which you expect to marry.

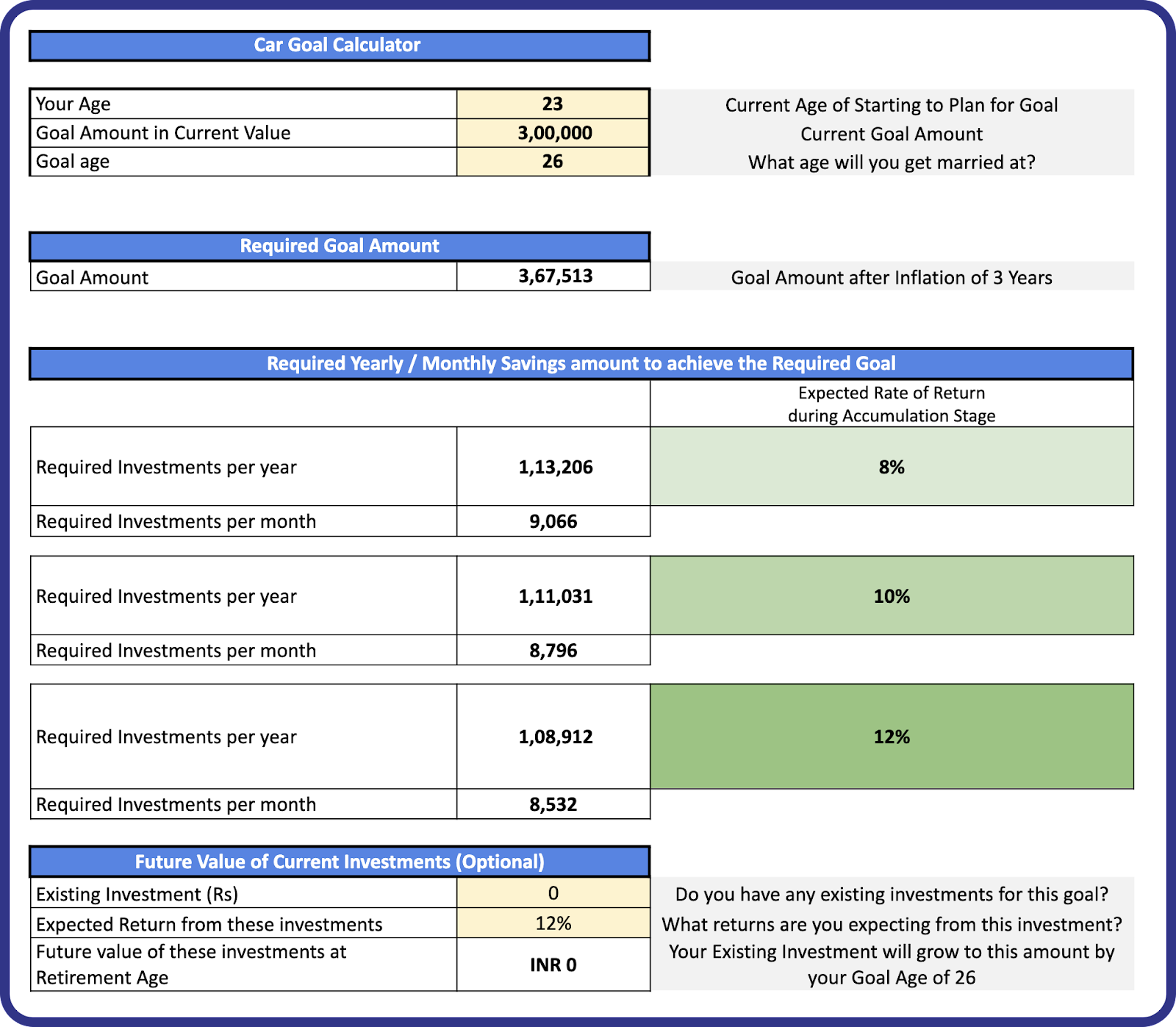

3. Car Goal Planning

You can also plan how much to save and invest every month to achieve the corpus needed to buy your dream car. You have to input how much your dream car will cost if you were to buy it today, your current age, and the age at which you plan to buy the car.

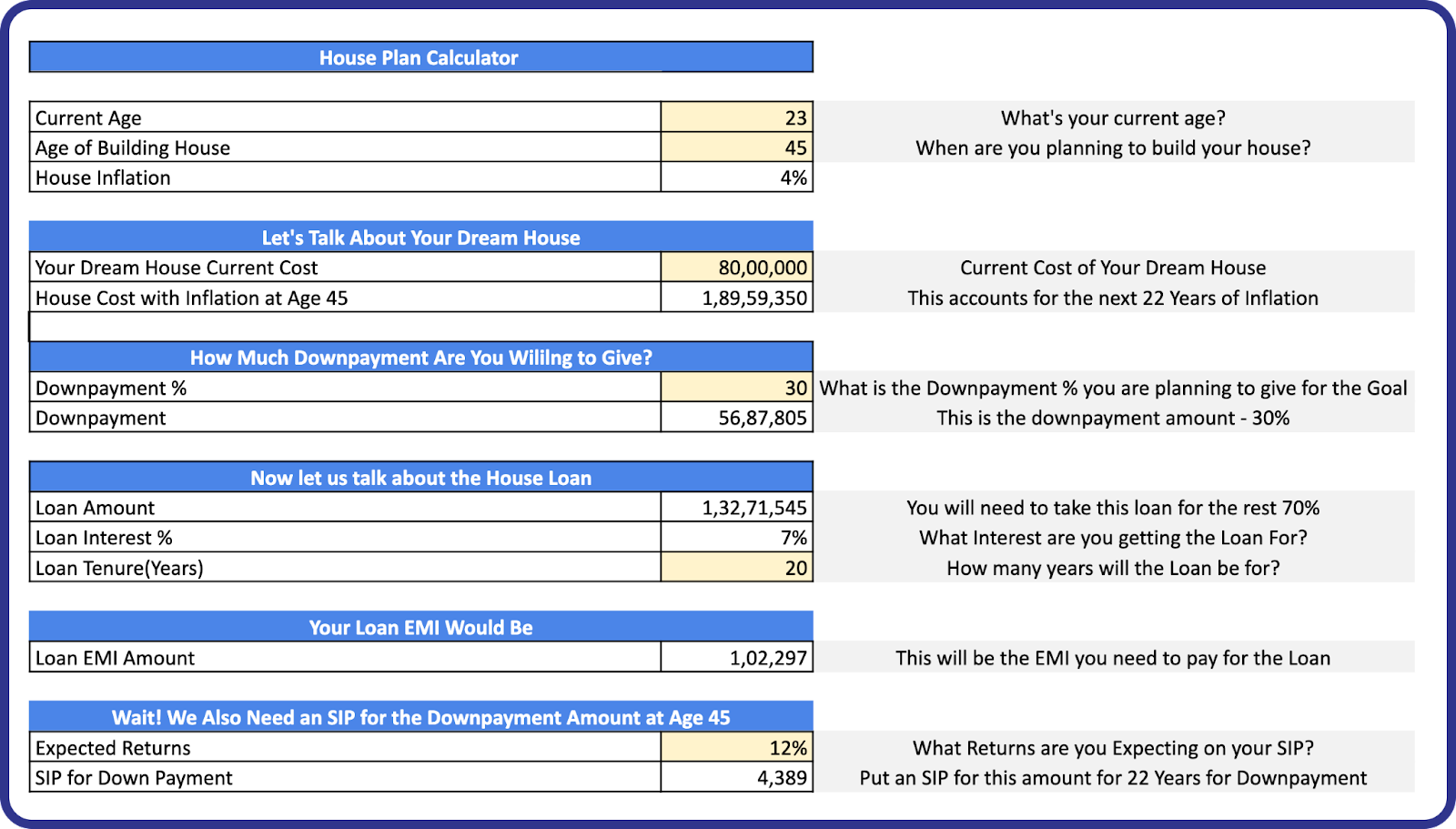

4. House Planning

You can plan to fund the dream home you wish to buy. You have to input how much it will cost to buy or build your dream home today, at what age you would like to buy it, how much you wish to pay as a down payment (in percentage), the tenure of the loan you would take out, and the expected returns on the SIP you’ll do to create the downpayment corpus.

5. Custom Goal Planning

Other than the goals mentioned above, you can also plan for any other financial goals using the custom goal sheet in the calculator.

How to Access the Calculator?

Click here to access the calculator.

It’s a READ-ONLY VERSION. You have to make a copy of the document to edit it.

Instructions to Use the Calculator

1. The link will take you to the read-only version of our Financial Calculator. Click on ‘Make a Copy’ under the File tab to create a copy of the calculator for you to edit. You can also download the file as .xslx to use the calculator on Microsoft Excel.

2. Edit or enter figures in the yellow cells only.

3. Do not edit any cells other than those in yellow as it will interfere with the preset formulas.

4. The calculator has 8 sheets:

- Input data here: Input the data asked in the sheet.

- Marriage goal planning

- Car goal planning

- Pre-marriage contribution to retirement: Input the amount you are willing to invest every month until your marriage and the expected return on the investment. Input goal age and goal amount as 0 if you do not wish to marry. If you are already married, only input the current age and input the rest as 0.

- Post-marriage monthly expense: Input the expenses that you would incur every month assuming that you were married already. If you do not wish to marry, input your current expenses here.

- Retirement planning

- House Planning

- Custom goal planning: you can plan any other financial goals not included in the calculator.

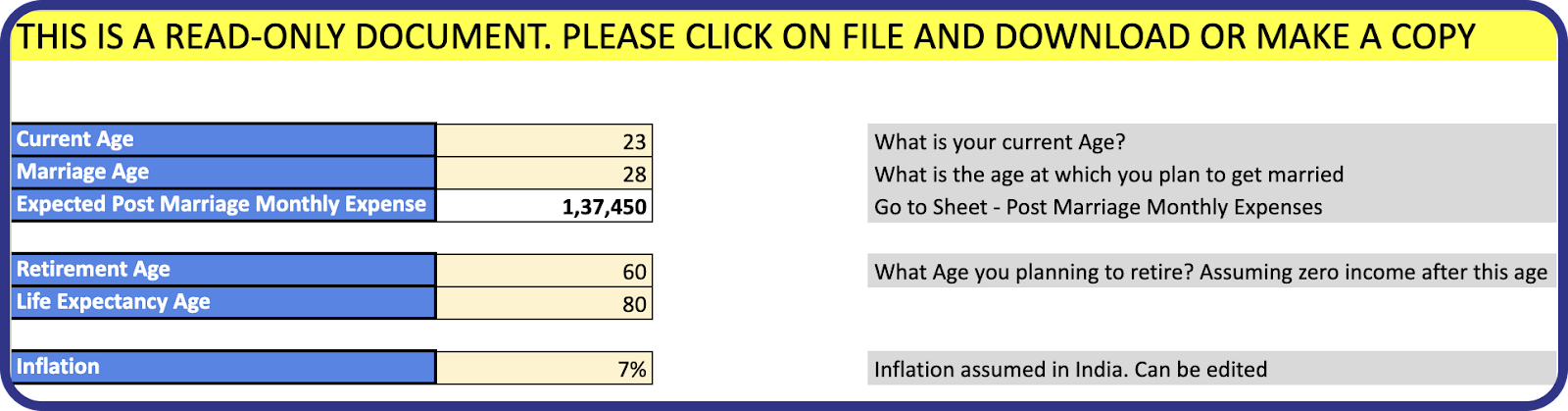

Retirement Goal Planning

Step 1: Input data here

Add current age, marriage age, retirement age, and life expectancy age in the datasheet.

Input marriage age as current age if already married or if you do not wish to get married.

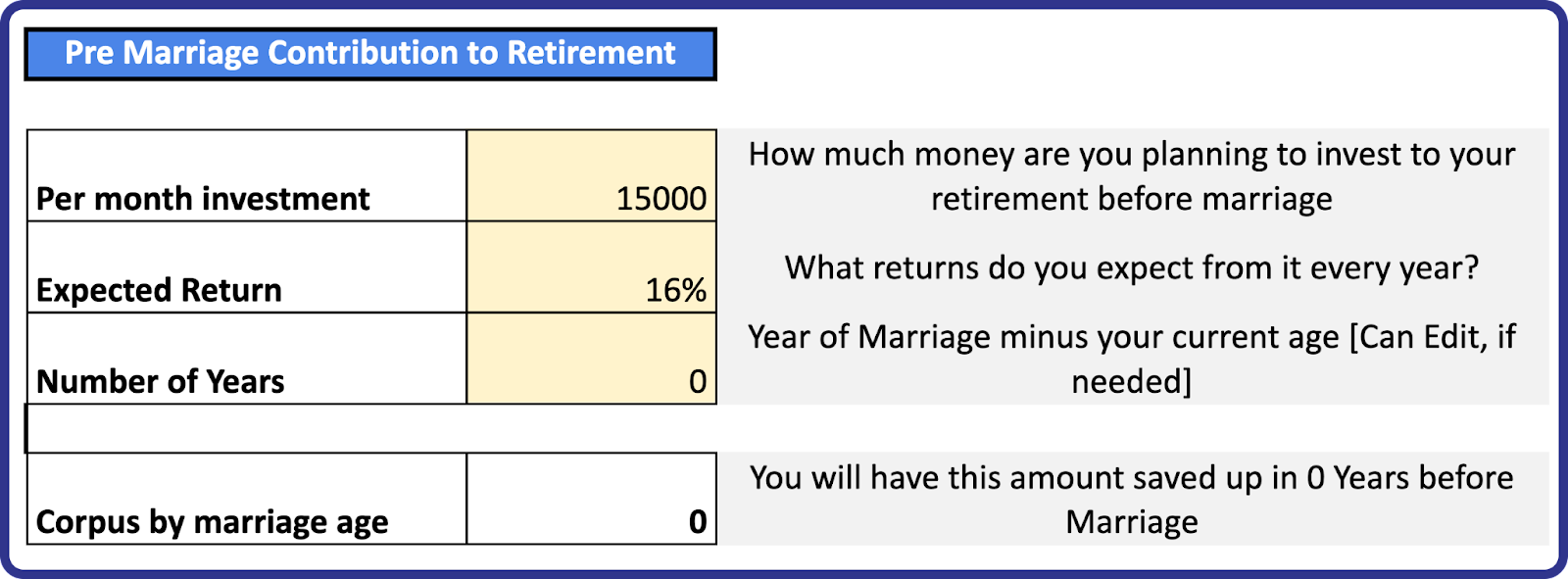

Step 2: Pre-marriage contribution to retirement

- Enter the amount you’re willing to invest every month towards your retirement before you get married and the expected return on that investment.

- The system will automatically calculate the number of years.

- If you do not wish to get married or if you’re already married, enter the amount as 0.

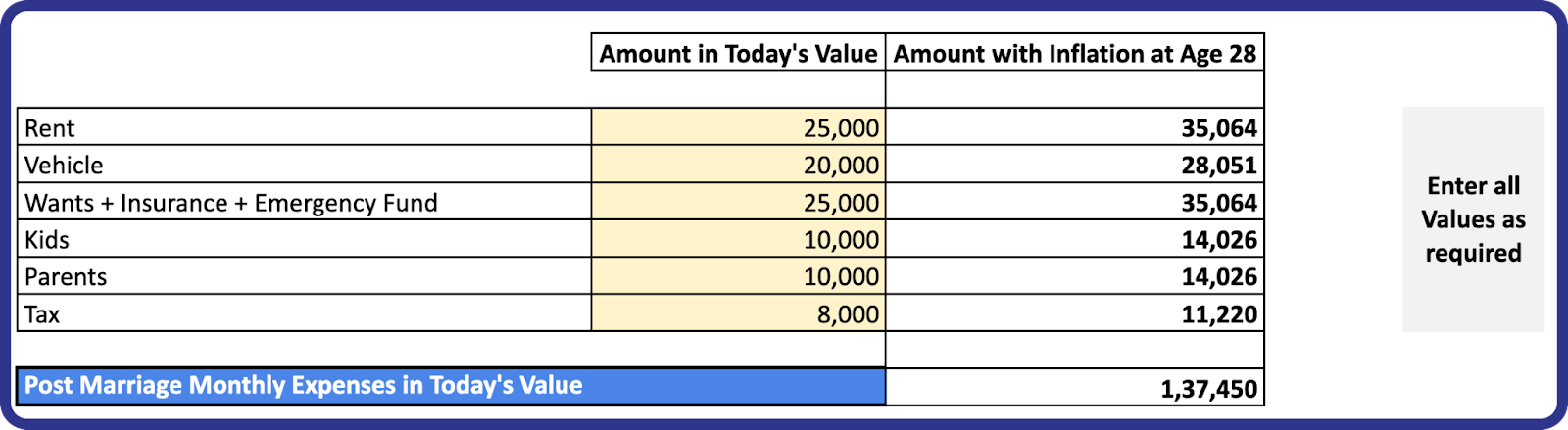

Step 3: Post-marriage monthly expense

- Calculate and enter the various expenses that you would incur if you were married today. If you are already married, input your current total monthly expenses or your current monthly expenses if you do not wish to get married.

- When you enter your wants, make sure that it is a monthly average of the money that you spend on your wants such as movies, trips, new electronics, etc.

- The planner works best only if you’re brutally honest with your answers.

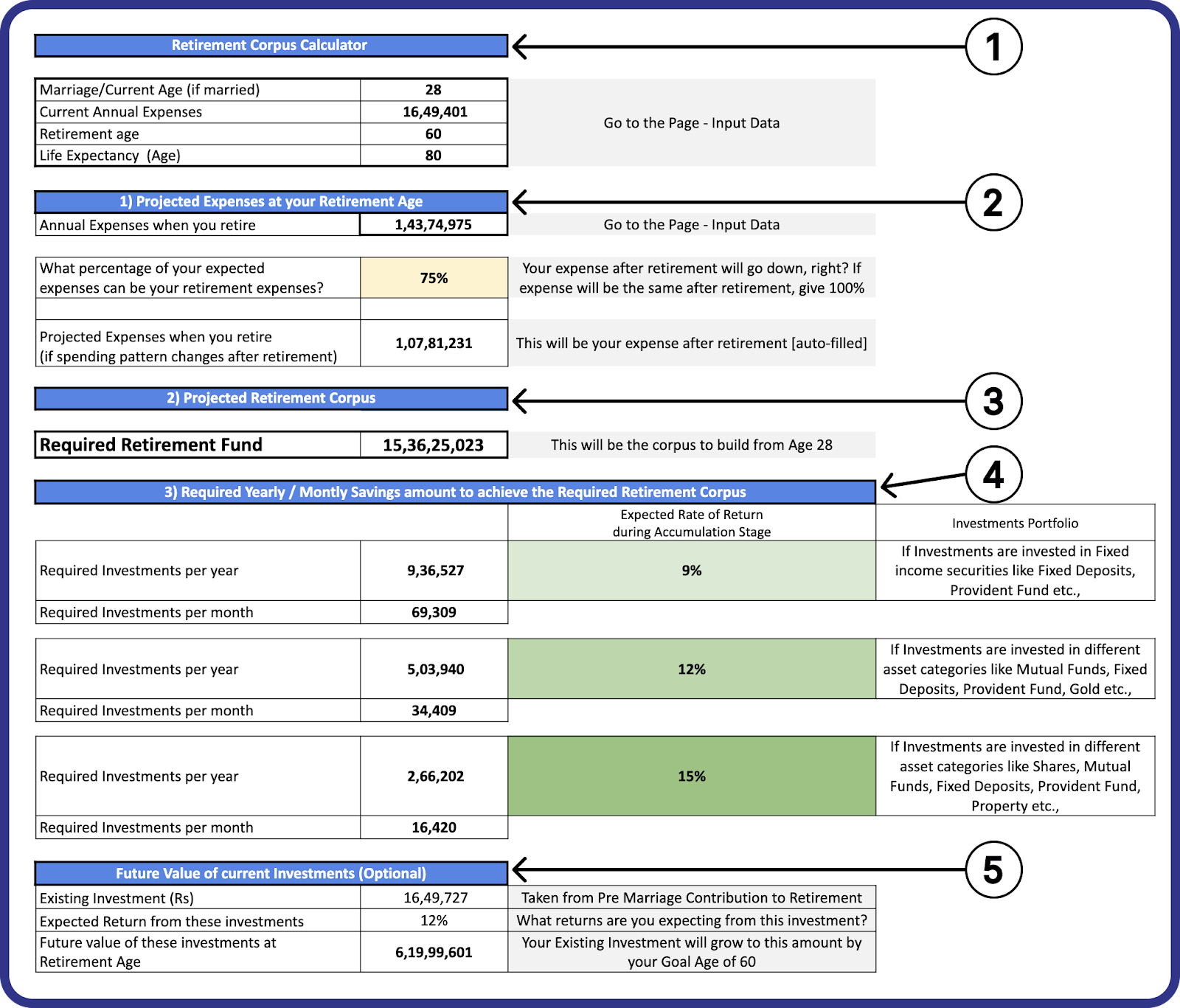

Step 4: Retirement planning

- Enter what percentage of your expected expenses can be your retirement expenses.

1. The data already added in previous sheets will be displayed here.

2. The system will recall data from the input sheet and display your annual expenses at the time of your retirement adjusted for inflation. You also need to enter what percentage of your expenses you expect to incur after you retire.

3. The projected retirement corpus is the amount of money you will need to comfortably retire according to your projected expenses.

4. It’ll show three different investment portfolios with different returns that you can invest in according to your risk appetite. The required investment per month/year is given adjacent to each investment portfolio. The higher the portfolio return, the lower the SIP amount.

5. The future value of current investments is the value of the investment you made in pre-marriage contribution to retirement when you retire.

So, to build a retirement corpus of ₹15 crore that can be used to fund your life’s expenses, you need to invest ₹16,420/month in a portfolio giving 15% CAGR from age 28 till you turn 60. If you build this retirement fund, you can continue to live off of it as you live currently, without having to do any job whatsoever after you retire!

Step 5: Start Investing!

As soon as you’ve selected a suitable investment portfolio, you can initiate an SIP!

Marriage Goal Planning

Step 1: Input data

- Enter your current age.

- Input the amount of money that you would need if you were to marry today.

- Enter the age at which you plan to get married.

Step 2: Input existing investments

- If you have any existing investments or savings that you have been saving up for your marriage, add them to the sheet. If you don’t, enter 0.

- Enter the expected returns from your existing investments.

Step 3: Decide on the investment Portfolio

- Once you enter all the data, the money you would need for your marriage when you get married will be displayed under the required goal amount.

- Choose from one of the three portfolios depending on your risk tolerance.

Step 4: Start your SIP!

After choosing the investment portfolio that suits you best, feel free to kick off a SIP!

Car Goal Planning

Step 1: Input data

- Enter your current age.

- Input the amount that you would need if you were to buy your dream car today.

- Enter the age at which you plan to buy your car.

Step 2: Input existing investments

- If you have any existing investments or savings that you have been saving up for buying a car, add them to the sheet. If you don’t, enter 0.

- Enter the expected returns from your existing investments.

Step 3: Decide on the investment portfolio

- Once you enter all the data, the amount you would need to buy the car when you reach your goal age will be displayed under the required goal amount.

- Choose from one of the three portfolios depending on your risk tolerance.

Step 4: Start your SIP!

Once you’ve picked the investment portfolio you like, you’re ready to start your SIP.

House Goal Planning

The house goal planner assumes that you will make a down payment for the house and take the remaining amount as a loan. If you wish to pay the entire cost of the house in a lump sum, then input the downpayment amount as 100%.

Step 1: Input data

- Enter your current age.

- Enter the age at which you plan to build or buy a home.

- Housing inflation in India has already been added.

- Enter the amount that would cost if you were to buy your home today.

- Enter the percentage of the amount that you are willing to pay as a down payment.

- The amount after deducting the down payment will be taken out as a loan. Enter the tenure of the loan you are going to take.

Step 2: Input existing investments

- If you have any existing investments or savings that you have been saving up for buying/building your house, add them to the sheet. If you don’t, enter 0.

- Enter the expected returns from your existing investments.

Step 3: Analyze the calculations

- Once you enter all the data, the calculations will be presented.

- Analyze how much each of the calculations amounts to.

- Analyze the EMI amount for the loan.

Step 4: Decide on the investment portfolio

- Once you analyze the down payment amount you would need, select a portfolio that falls within your risk appetite to do an SIP. Thus, you would be able to build the corpus needed for the down payment.

Step 5: Start your SIP!

Once you’ve found the investment portfolio that suits you, go ahead and start your SIP!

Custom Goal Planning

You can use the custom goal planner sheet to plan any of your financial goals.

In this article, we discussed how to use marketfeed’s Excel calculator to plan your financial goals. You now know how much to invest every month to achieve your financial goals!