As of late, we have noticed that many of our readers are confused about how to start their investment journey. The primary motive behind investing your hard-earned income is to fight inflation or a general rise in the prices of goods. The purchasing power of cash in hand or your bank account continuously reduces with time. In order to beat inflation and achieve future goals, you need to invest your money in a variety of financial products.

Our primary mission here at marketfeed is to show the path for every individual to become financially independent. We help you make informed decisions in the beautiful world of finance. However, it is important that we start from the very basics and slowly work our way up. So, let us have a clear understanding of some of the best investment options that can help you achieve financial freedom.

Direct Equity

Direct equity means investing in stocks. When you buy stocks (or shares) of a listed company, you become part-owner of the firm (even though it’s a very tiny fraction). This means that you are directly investing in the company’s development and growth. In the long run, stock markets have always beaten inflation and have delivered higher returns than other asset classes. Thus, stocks are always ideal for long-term investments. To directly invest in shares or equity, you would need to open a Demat account.

However, investing in stocks contains a high level of risk. Stock markets are often very volatile, as a variety of factors (including interest rates, government policies, economic figures, company operations) influence the performance of stocks. You will have to actively manage your investments to limit losses. One needs to have a lot of patience and gain market knowledge to get sufficient returns. With time, you will learn how to pick the right stock and time your entry and exit. Target-oriented and well-researched stock market investments can definitely help you beat inflation.

Mutual Funds

If you are not comfortable with investing directly in stocks due to the risks involved, you can always invest in mutual funds. A mutual fund takes money (investments) from different individual and institutional investors who have a common investment objective. This pooled sum of money is managed by a professional fund manager, who invests in securities and assets to generate returns for investors.

You can find equity, debt and hybrid mutual funds as a general classification. Equity mutual funds invest in stocks and equity-related instruments, while debt mutual funds invest in bonds and other debt instruments. Hybrid mutual funds invest in a mix of equity and debt instruments. There are various equity mutual funds based on market capitalization, tax-saving funds, sectoral funds, and much more. As per reports, the 5-year and 10-year returns of these equity fund categories were above 10% as of April 2021.

Mutual funds are a very attractive investment option as you do not have to spend much time and effort tracking them. Instead of investing a large sum of money all at once, you could start a Systematic Investment Plan (SIP) and invest small amounts of money periodically (usually every month) in mutual funds. They are very flexible, as you can begin and stop investing according to your convenience. However, one needs to conduct a proper analysis or study before investing in a particular mutual fund. Element of risk is also present as the returns are dependent on market movements.

Bonds

A bond is a fixed-income instrument issued by companies or even government entities to raise funds. Investors can lend their money to organisations in return for fixed yearly interest. At the time of maturity of the bond, you will receive the initial money you had invested and the interest offered on it. Nowadays, bonds offer fixed returns that are at least 2-3% higher than fixed deposits (FDs). Government bonds in India are an ideal investment option as it provides more than 7% guaranteed returns.

Before investing in bonds, you need to consider and analyse important factors such as coupon rate (fixed interest that the bond pays annually), payment frequency (the number of times the interest is paid to the bondholder), maturity date, and credit rating. A higher-rated bond carries a higher level of safety of investment. AAA-rated bonds are the most secure.

Gold

Gold is one of the best asset classes that can be used to counter inflation. This is because the increase in gold prices and the returns from it have always been able to offset inflation in the past. According to the World Gold Council, for every 1% increase in inflation, there is a 2.6% rise in gold demand. This ultimately leads to an increase in gold prices. However, acquiring and holding gold in the form of jewellery has its own concerns such as safety and high cost.

An alternative way of owning gold is through paper gold or gold ETFs. These are units representing physical gold which may be in paper or dematerialised (electronic) form. One Gold ETF unit is equal to 1 gram of gold and is backed by physical gold of very high purity. The investments made in paper gold are less costly.

What are ETFs?

As the name suggests, an exchange-traded fund (ETF) is a fund that can be traded on the stock exchange. It is a method through which you can buy and sell a basket of assets without having to buy all the components individually. ETFs are managed by finance professionals who own certain underlying assets (such as stocks, bonds, currencies, and commodities). They design a fund to track the performance of these assets and then sell shares of these funds to investors.

ETFs are a great method to diversify your portfolio and manage risks. It is also a cost-effective method of investing and also offers several tax benefits.

Fixed Deposits, Recurring Deposits

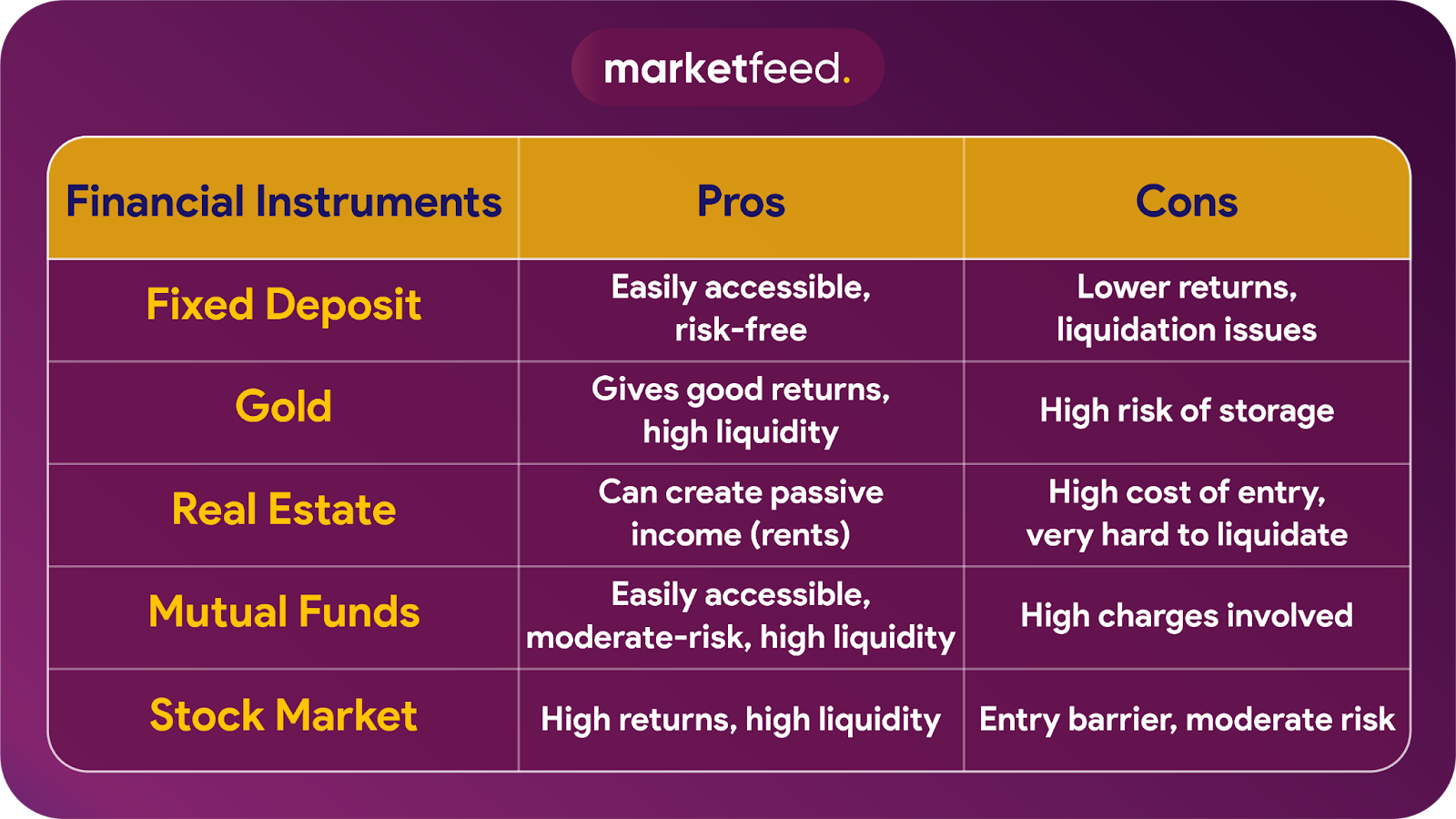

Fixed Deposits (FDs) are an investment option offered by banks and financial institutions. It is something that most of us are familiar with. You deposit a lump sum of money for a fixed period and earn a predetermined rate of interest on it. The interest rate of FDs differs from one bank to another. However, the average rate of FDs in India is only 5-6%, which may be insufficient to beat inflation. FDs are favorable for those investors who wish to receive guaranteed, yet conservative returns.

Recurring Deposits (RDs) are a fixed-tenure investment option provided by banks and other institutions that allow individuals to invest a fixed amount every month for a pre-defined time period. The interest rate on RDs is determined by the institution offering them. RDs also offer complete capital protection as well as guaranteed returns.

Government Schemes

Public Provident Fund (PPF) is a long-term investment scheme provided by the Government of India (GoI) that has a lock-in period of 15 years. Currently, the annual rate of interest offered on PPF is 7.10%. The entire amount withdrawn at the end of the 15 years is entirely tax-free for the investor. You can also take loans and make partial withdrawals if certain conditions are met.

Employee Provident Fund (EPF) is a retirement-oriented investment scheme that helps salaried individuals. EPF deductions are a specific percentage of your salary every month, and the same amount is matched by the employer as well. This entire amount is pooled into your EPF corpus or account every month, and you receive interest on it. Currently, the annual rate of interest offered on EPF is 8.50%. At the time of maturity, the entire amount withdrawn from the EPF corpus is entirely tax-free.

The National Pension Scheme (NPS) is another tax-saving investment option offered by the Government of India. Anyone between the age of 18-65 years can make voluntary contributions to this scheme. Investors who subscribe to NPS will mandatorily stay locked in until their retirement and can earn better returns than PPF or EPF. Historically, NPS has delivered ~8-10% returns every year.

Real Estate

Investing in real estate is one of the best ways to diversify your portfolio. Since the value of a real estate property appreciates (or increases) with time, you can earn exponential returns on it. Acquiring a property and renting it out would be an ideal way to earn passive income. However, the location of the property is the most important factor that will determine its value and also the rental income that can be earned from it. In the case of residential properties, investors must always conduct a thorough study of home loan interest rates, offers provided by developers, and government regulations. Another important factor to consider is that real estate is highly illiquid. Properties cannot be sold off and converted into cash quickly.

If you don’t have adequate capital for acquiring real estate properties, you could always invest in a real estate investment trust or REIT. This is very similar to a mutual fund, wherein you can invest small amounts of money on certain income-generating assets and earn a good return from them. A REIT owns and operates several properties such as complexes, infrastructure projects, healthcare units, apartments, and more. The money pooled in from the REIT is used to manage these assets. And, the income derived from these properties or assets is shared among all investors (or unitholders) of the REIT.

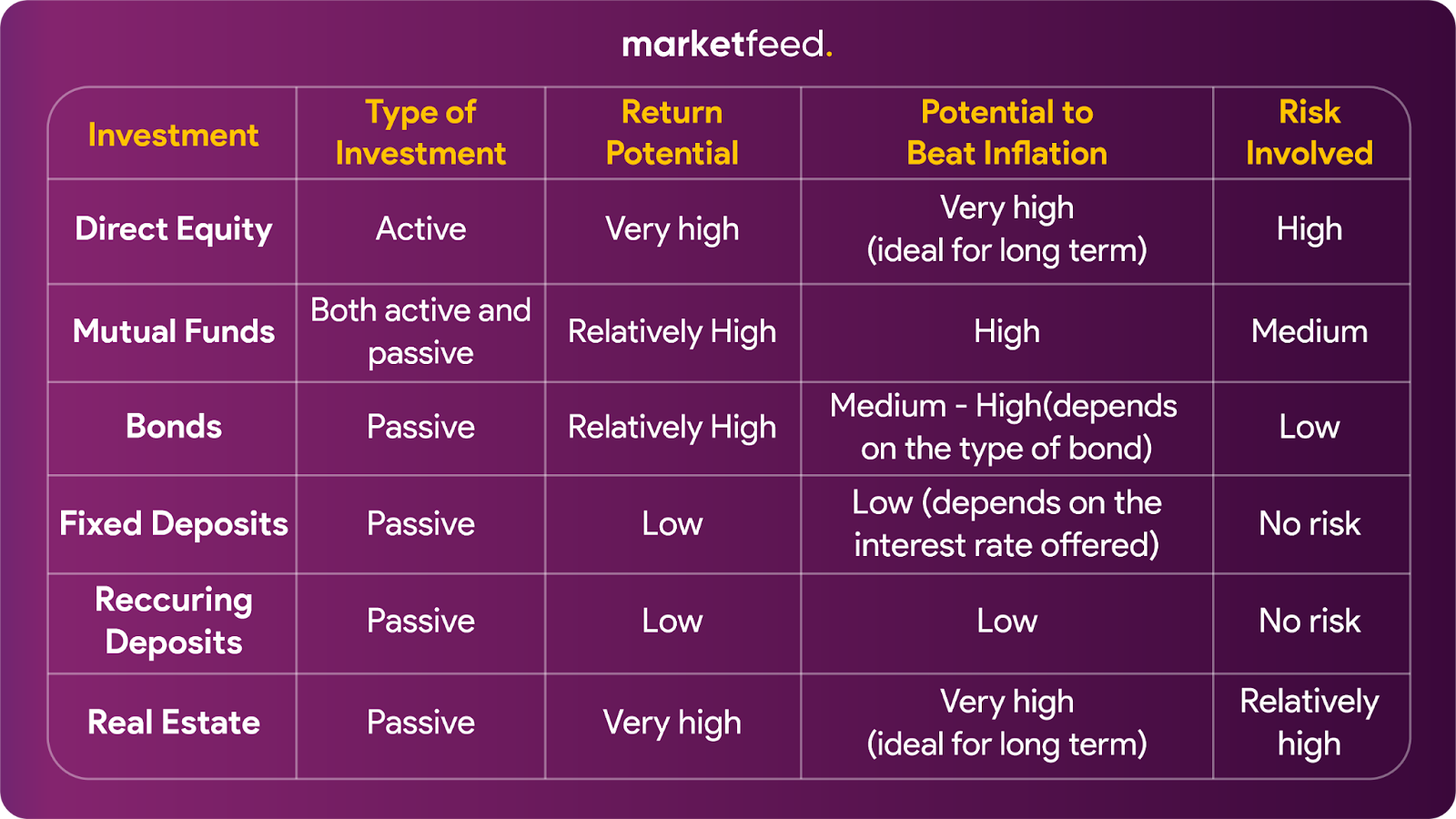

Types of Investments in a Nutshell

Conclusion

Now, you have an idea of how to grow your hard-earned income to beat inflation and lead a better life. However, it is up to you to figure out the right investment that fits your profile and financial goals. Start your investment journey only after carefully going through the risks and costs associated with each of them. Go for those investments that you clearly understand from your own research. At the same time, it is vital that you invest your money in different products and diversify your portfolio. More importantly, make sure you do not fall for scammy schemes that promise high returns in a short period. The sooner you start investing, the longer you will stay invested and earn higher returns.

Open a free Demat account –

Upstox

Zerodha

Happy Investing!