Ever wondered how to figure out what a company is really worth? That’s where valuation comes in – it’s like a magic trick for understanding a business’s true value. Whether you’re new to investing or a pro, getting the hang of valuation basics is key to making smart money moves. In this article, we dive into the basics of valuation and how a company is valued to help you make better investment decisions.

What is Valuation?

In finance, valuation simply means finding the real worth of a company. Valuation is used to determine the price that market participants are willing to pay or receive while selling a business. Thus, value investing is based on the true value of a business compared to its market value. Let us understand what market value and intrinsic value is.

Market Value vs Intrinsic Value

The market value of a business is the worth that the market assigns to it. You can calculate the market value of any publicly traded company by multiplying the share price by the number of outstanding shares. However, the market value may not be the actual value of the business. Sometimes, the market may overvalue a company for reasons such as high demand for its stocks, future plans, market sentiments for that stock, etc.

Although the market value is what the market thinks a company is worth, the firm also has an intrinsic value. Intrinsic value is the true and accurate worth of a company. If the market value of a company is higher than its intrinsic value, then the stock is currently overpriced or overvalued. On the other hand, if the intrinsic value of a company is lower than its market value, then the company is undervalued.

How to Find the Intrinsic Value of a Company?

Finding the actual valuation of a company is a very complex, intensive, and lengthy process. Investment banks put together a team and take multiple days to find the true value of a company. Experts use different methods like Dividend Discount Models (DDM), Residual Income Models, Discounted Cash Flow Models, etc. However, for the purpose of our learning series, we will learn a simplified form of Discounted Cash Flow Analysis.

What is Discounted Cash Flow Analysis?

Discounted Cash Flow (DCF) models work on the concept of the time value of money. It is a concept that says that the value of a certain sum of money is worth more in the future than the same amount of money today because of the potential earning capacity of money. If you had the choice to receive ₹100 today or 1 year later, the choice should be today. This is because, if you receive ₹100 today and you invest that amount in an instrument giving you 5% returns per annum, then by the end of the year, you would have ₹105 with you. Having ₹105 over ₹100 is better at the end of the year.

Discounted cash flow analysis finds the present value of expected future cash flows using a discount rate. From the above example, 5% is the discount rate. A discount rate is the expected return over a period. If you think that the company will grow by 10% for the next 5 years, then the discount rate should be 10%. As the discount rate increases, the intrinsic value will decrease. So, we should take reasonable care while assigning a discount rate and make sure that the rate is fair and realistic.

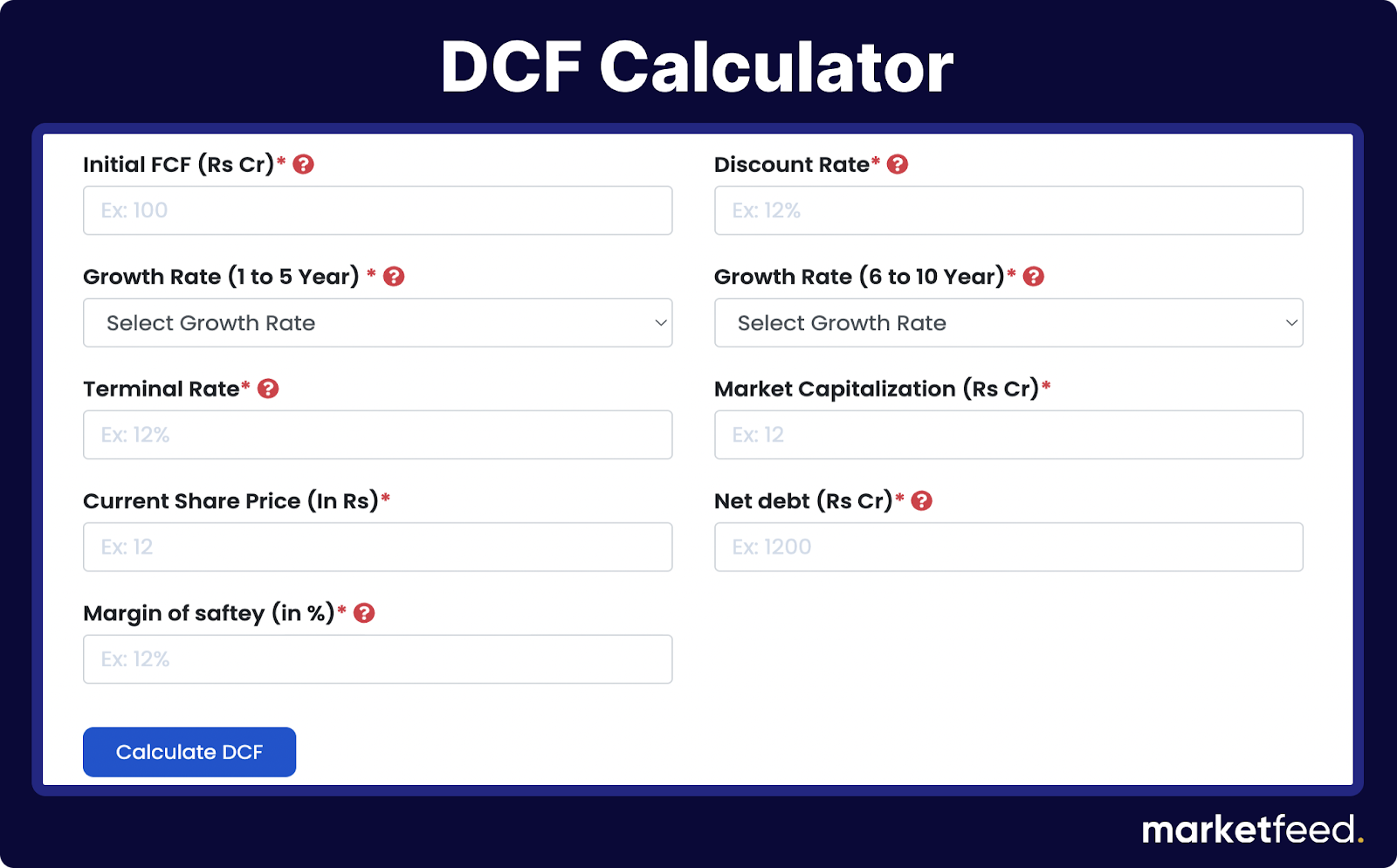

DCF Calculator

To find the intrinsic value of a company, we will be using a Discounted Cash Flow (DCF) calculator. Click here to use the calculator.

Steps to Calculate Intrinsic Value

Step 1: Enter the initial FCF

FCF stands for free cash flow. Free cash flow = Net Cash flow from operating activities – Capital expenditure. Enter the three-year average FCF of a company.

Step 2: Enter the Discount Rate

The discount rate refers to the required rate of return. It is the return rate that you are expecting from a similar alternative investment.

Step 3: Enter Growth Rate (1 to 5 years)

It is the rate at which the company might grow in the next 1 to 5 years. Large and well-established companies will have relatively low growth rates. You can also use the average growth rate of revenue or profit for the past 5 years and use that rate here.

Step 4: Enter Growth Rate (6 to 10 years)

It is the rate at which the company might grow in the next 6-10 years after the initial period.

Step 5: Enter the Terminal Rate

It is the rate at which the company is expected to grow 10 years from now. It is calculated by assuming the constant growth of a company beyond a certain period. 5% and below is a fair terminal rate.

Step 6: Enter the Market capitalization

The market capitalization can be calculated by multiplying the total number of outstanding shares by its current share price. It can be easily found from screener.in, Tickertape, etc.

Step 7: Enter the Current Stock Price

Step 8: Enter the Net Debt

Net debt can be calculated by deducting cash and cash equivalents from a company’s total debt/liabilities. This data can be calculated from the balance sheet.

Step 9: Enter the Margin of Safety (MoS)

The margin of Safety provides discounts for uncertainties in the business.

Step 10: Click ‘Calculate’

The calculator gives two values:

- DCF value per share shows the estimated intrinsic value.

- Fair value shows the intrinsic value per share after deducting the margin of safety.

If the intrinsic value derived is higher than the market price, then the stock is undervalued and if the intrinsic value is lower than the current market price, then the stock is overpriced.

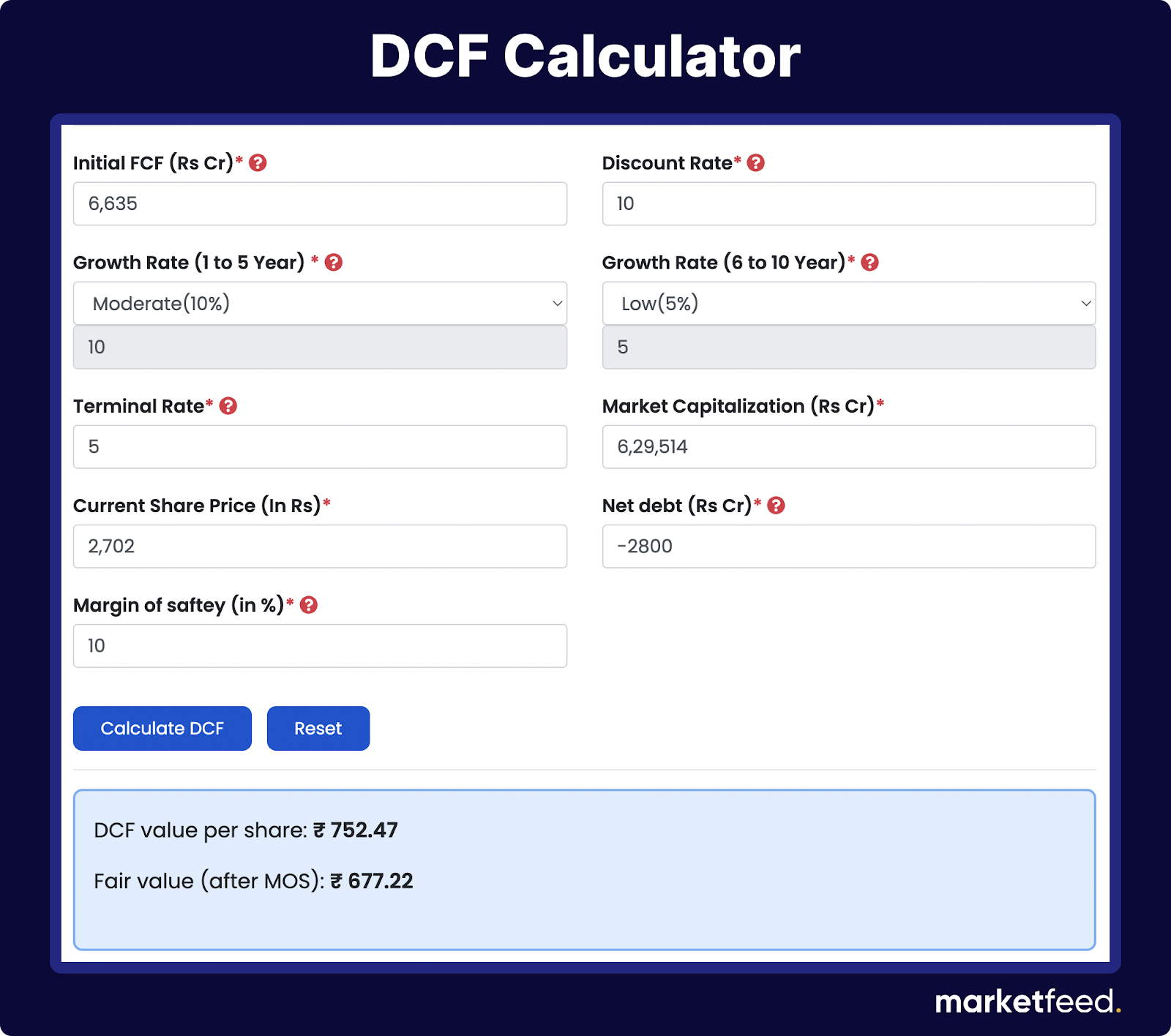

An Illustration

Let us use the calculator to find the intrinsic value of Hindustan Unilever (HUL). The values are entered as per the above instructions:

Assuming that the current share price of HUL is ₹2702, the DCF value or intrinsic value per share is ₹752.47. The fair value or intrinsic value after the margin of safety is ₹677.22. The stock price of HUL is 3 times more overpriced than its estimated intrinsic value.

We have learned now how to find the intrinsic value of a company. This value can be used while making decisions when it comes to value investing. However, we don’t give much importance to intrinsic value in the case of growth investing.

In conclusion, valuation is not just about numbers; it’s about unlocking the potential of a company’s true value. So, as you navigate the world of finance, use these insights to guide your journey and make informed choices!

Also read: 5 Best Steps to Find Quality Stocks in India