Ever wondered how to figure out what a company is really worth? That’s where valuation comes in – it’s like a magic trick for understanding a business’s true value. Whether you’re new to investing or a pro, getting the hang of valuation basics is key to making smart money moves. In this article, we dive into the basics of valuation and how a company is valued to help you make better investment decisions.

What is Valuation?

In finance, valuation simply means finding the real worth of a company. Valuation is used to determine the price that market participants are willing to pay or receive while selling a business. Thus, value investing is based on the true value of a business compared to its market value. Let us understand what market value and intrinsic value is.

Market Value vs Intrinsic Value

The market value of a business is the worth that the market assigns to it. You can calculate the market value of any publicly traded company by multiplying the share price by the number of outstanding shares. However, the market value may not be the actual value of the business. Sometimes, the market may overvalue a company for reasons such as high demand for its stocks, future plans, market sentiments for that stock, etc.

Although the market value is what the market thinks a company is worth, the firm also has an intrinsic value. Intrinsic value is the true and accurate worth of a company. If the market value of a company is higher than its intrinsic value, then the stock is currently overpriced or overvalued. On the other hand, if the intrinsic value of a company is lower than its market value, then the company is undervalued.

How to Find the Intrinsic Value of a Company?

Finding the actual valuation of a company is a very complex, intensive, and lengthy process. Investment banks put together a team and take multiple days to find the true value of a company. Experts use different methods like Dividend Discount Models (DDM), Residual Income Models, Discounted Cash Flow Models, etc. However, for the purpose of our learning series, we will learn a simplified form of Discounted Cash Flow Analysis.

What is Discounted Cash Flow Analysis?

Discounted Cash Flow (DCF) models work on the concept of the time value of money. It is a concept that says that the value of a certain sum of money is worth more in the future than the same amount of money today because of the potential earning capacity of money. If you had the choice to receive ₹100 today or 1 year later, the choice should be today. This is because, if you receive ₹100 today and you invest that amount in an instrument giving you 5% returns per annum, then by the end of the year, you would have ₹105 with you. Having ₹105 over ₹100 is better at the end of the year.

Discounted cash flow analysis finds the present value of expected future cash flows using a discount rate. From the above example, 5% is the discount rate. A discount rate is the expected return over a period. If you think that the company will grow by 10% for the next 5 years, then the discount rate should be 10%. As the discount rate increases, the intrinsic value will decrease. So, we should take reasonable care while assigning a discount rate and make sure that the rate is fair and realistic.

DCF Calculator

To find the intrinsic value of a company, we will be using a Discounted Cash Flow (DCF) calculator. Click here to use the calculator.

(Source: Finology)

Steps to Calculate Intrinsic Value

Step 1: Enter the initial FCF

FCF stands for free cash flow. Free cash flow = Net Cash flow from operating activities – Capital expenditure. Enter the three-year average FCF of a company.

Step 2: Enter the Discount Rate

The discount rate refers to the required rate of return. It is the return rate that you are expecting from a similar alternative investment.

Step 3: Enter Growth Rate (1 to 5 years)

It is the rate at which the company might grow in the next 1 to 5 years. Large and well-established companies will have relatively low growth rates. You can also use the average growth rate of revenue or profit for the past 5 years and use that rate here.

Step 4: Enter Growth Rate (6 to 10 years)

It is the rate at which the company might grow in the next 6-10 years after the initial period.

Step 5: Enter the Terminal Rate

It is the rate at which the company is expected to grow 10 years from now. It is calculated by assuming the constant growth of a company beyond a certain period. 5% and below is a fair terminal rate.

Step 6: Enter the Market capitalization

The market capitalization can be calculated by multiplying the total number of outstanding shares by its current share price. It can be easily found from screener.in, Tickertape, etc.

Step 7: Enter the Current Stock Price

Step 8: Enter the Net Debt

Net debt can be calculated by deducting cash and cash equivalents from a company’s total debt/liabilities. This data can be calculated from the balance sheet.

Step 9: Enter the Margin of Safety (MoS)

The margin of Safety provides discounts for uncertainties in the business.

Step 10: Click ‘Calculate’

The calculator gives two values:

DCF value per share shows the estimated intrinsic value.

Fair value shows the intrinsic value per share after deducting the margin of safety.

If the intrinsic value derived is higher than the market price, then the stock is undervalued and if the intrinsic value is lower than the current market price, then the stock is overpriced.

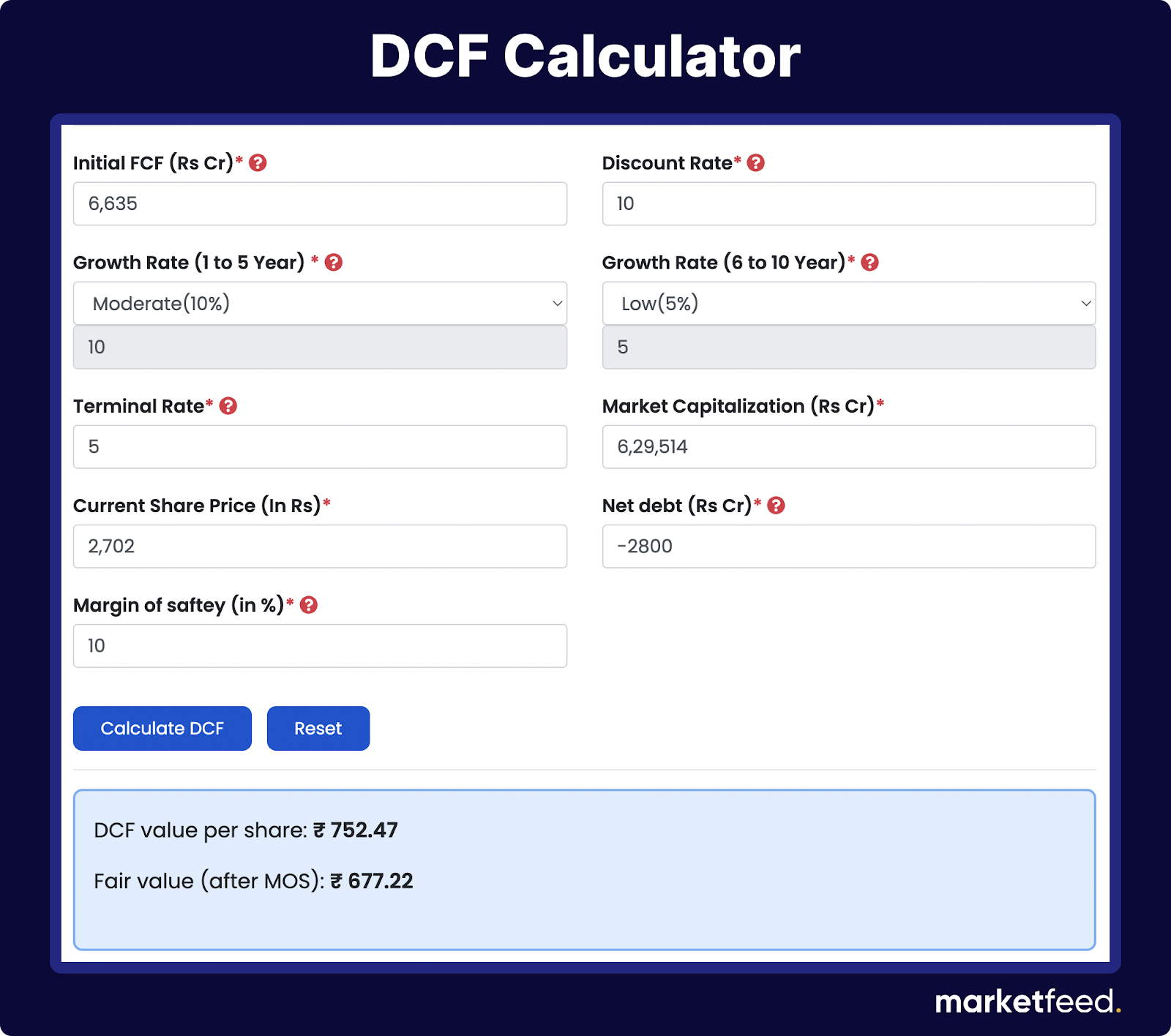

An Illustration

Let us use the calculator to find the intrinsic value of Hindustan Unilever (HUL). The values are entered as per the above instructions:

(Source: Finology)

Assuming that the current share price of HUL is ₹2702, the DCF value or intrinsic value per share is ₹752.47. The fair value or intrinsic value after the margin of safety is ₹677.22. The stock price of HUL is 3 times more overpriced than its estimated intrinsic value.

We have learned now how to find the intrinsic value of a company. This value can be used while making decisions when it comes to value investing. However, we don’t give much importance to intrinsic value in the case of growth investing.

In conclusion, valuation is not just about numbers; it’s about unlocking the potential of a company’s true value. So, as you navigate the world of finance, use these insights to guide your journey and make informed choices!

Have you ever wondered what the stock market is and how it works? If yes, you’re not alone. The stock market can seem confusing and intimidating for people who don’t know how it works. But don’t worry! In this article, we shall learn what the stock market is, how it works, and who market participants are.

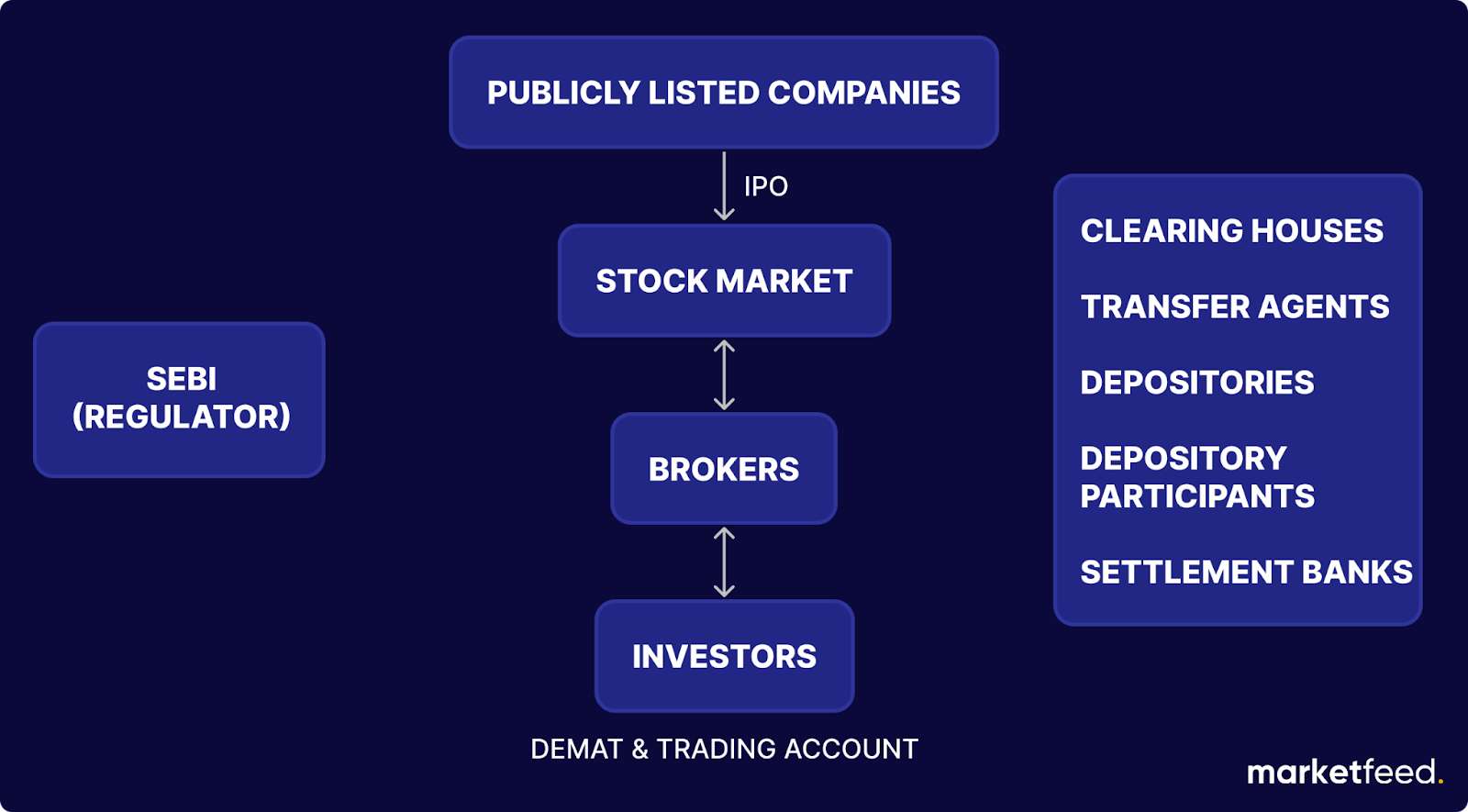

Given below are the different participants in the stock market. We’ll understand more about them through a story.

Let’s Look at a Story!

Mr. Jignesh, an owner of a renowned supermarket in Bengaluru, has been successfully running his business for the past ten years. The supermarket has been generating decent revenue and is highly profitable. His business also has goodwill (proprietary or intellectual property and brand recognition). When it comes to business, there are two things you must understand:

Ownership of a Business Jignesh completely owns and runs the supermarket, and the profit is not shared with anyone else.

Valuation of a Business Anything and everything has a value attached to it, even a business. The business has been generating income for Jignesh for the past ten years, so it is valuable. The valuation of a business is the economic value of how much a person has to pay to acquire 100% of the business from him. Let’s assume that the supermarket is valued at ₹1 crore.

Since Jignesh is growing old, he feels he doesn’t want to work as much as he did and is looking for a partner to operate the business in return for 50% of the ownership of his business. He decided to share his business with a partner, Ms. Riya.

What are Shares?

Shares represent units of ownership of a company. A shareholder is entitled to a part of the profit that the company generates.

The ownership of Jignesh’s supermarket was divided into 1000 equal shares. The value of each share can be mathematically expressed as:

Value of 1 Share = Total Valuation / Total Number of Shares

= 1,00,00,000 / 1000

= ₹10,000 per share.

Riya agreed to acquire 500 shares (50%) of the supermarket in consideration of the value of those shares in Cash.

Valuation = Total Number of Shares x Value of Each Share

Riya paid ₹50,00,000 to Jignesh, and they both became partners in the supermarket business.

A few years later, the business expanded with several profitable outlets across Bengaluru. Now, Jignesh and Riya want to open 200 more stores nationwide, for which they need a large amount of capital. The easiest way to get funding or capital is by taking out a loan from a bank and using the business’ assets as collateral. However, this carries the risk of falling into a debt trap. If they are unable to repay the loan for some reason, the assets will be seized by the bank to recover the loan. Jignesh and Rita did not want to deal with these issues.

An alternative would be to find more people who are interested in becoming part-owners of the business across Bengaluru. Even then, they may not be able to find enough people to do so. At this point, Jignesh becomes aware of the stock market. If they convert their company into a Public Limited company, they can raise capital from thousands of investors across India and other countries. The process of issuing shares to the public to raise capital for a business is known as an Initial Public Offering (IPO).

What is the Stock Market?

A stock market is a place where shares of publicly listed companies are traded. It is a physical place or institution where shares are bought and sold.

So Why Do Companies Go Public?

To Raise Capital: The company can gather funds for many objectives, such as paying liabilities (loans) and funding its future expansion projects.

Reward Founders & Early Investors: The founders and early investors of a company hold a good portion of the shares in their entity. They can sell these shares to the public and the proceeds go directly to them rather than to the company. It can be considered as a reward for all the time and effort they put in to build the company from the ground up. So going public can give them an early exit.

What are Stock Exchanges?

A stock exchange is a financial institution where different participants come together to buy and sell securities(shares). It provides the infrastructure for these activities. The term Stock Market is an umbrella term for a collection of Stock Exchanges.

The two major Stock Exchanges in India are:

Bombay Stock Exchange (BSE)

National Stock Exchange (NSE)

BSE is older than NSE, which explains why more companies are listed on the BSE than NSE.

Coming back to the story, Jignesh’s company had a total of 1000 shares, out of which they decided to issue 15% of the shares to the public. Thus, 150 shares are being offered to the public.

1000 x 15% = 150

How Many Shares Will a Company Have? Who Decides That?

A company’s promoters can decide how many shares it should have. Some firms may have thousands of shares, while others may have lakhs or even crores of shares.

For example, the valuation of Jignesh’s company was ₹1 crore in the beginning. But the business has grown over the years, and now the valuation stands at ₹2 crores, bringing the value of each share to ₹20,000.

Why do Investors Exist? What are their Objectives?

The two main objectives of investors are:

1. Capital Appreciation – When a company grows, the price of its shares increases. If investors buy the shares of a company when the prices are low and sell them when the prices increase, they can make good profits via capital appreciation.

2. Earn Dividends – When a company makes profits every year from its operations, it distributes a portion of the profits to shareholders as dividends. However, it is not necessary for them to declare dividends every year. It’s the company’s choice whether to issue dividends or not. The company may fully retain its profits for future capital needs or may give out a part of the profit and retain the rest.

In short, the objective of a public limited company is to raise capital for its funding needs and the investors’ objective is to grow their money. But the real question is, how does the stock market fit into this?

Why do Stock Markets Exist?

The stock market provides an avenue for a public company to raise capital from investors in consideration of shares. Investors will be able to grow their savings and wealth through capital appreciation and dividends. The stock market is the facilitator for the two parties.

What are Primary Market and Secondary Market?

The stock market is divided into two:

1. Primary Markets It is a market wherein a firm issues securities/shares to investors directly (via an initial public offering or IPO). These sale proceeds go directly to the issuer to finance their capital requirements.

2. Secondary Markets It is the market where previously issued securities are bought and sold among investors. These sale proceeds go to the person who holds the securities.

In our story, many people wanted to buy shares of his company after the IPO. However, the company does not issue any more shares as the IPO is already done. So these new investors can only buy the shares from those already holding them.

When such transactions happen between investors in the secondary markets, the price of the share gets updated. If an existing shareholder sells the stock to another person for ₹20,100, the price of all the shares of the company gets updated to ₹20,100. Consequently, the net worth of the shareholders increases as the price of the shares they hold increases.

Who Decides the Price of a Stock?

The two reasons which decide the price of a stock are:

Company’s Actual Valuation: A company’s value fluctuates as the revenue, profit, and goodwill change. The future prospects of the company also contribute to the valuation. If the revenue and profits go down, the valuation may also decrease, which causes the share price to drop. However, if the revenue and profit increase, the valuation could also rise.

Demand & Supply: The market forces of supply and demand also play an important role in deciding the share price. If the demand for the stock increases, then its price also increases since supply is limited. If the demand for the stock decreases, then its price also decreases since the supply is the same. Demand for the stock depends upon market sentiments, which refers to the overall attitude of investors toward the company. If the market sentiment is positive, then the demand for the stock will be high, thus driving the stock price up. Demand for the stock will be less if the market sentiment is negative.

Why Do Stock Prices Fluctuate Every Second?

The Last Traded Price (LTP) refers to the price at which the previous share transaction took place. The stock market has lakhs of participants, and transactions happen every second. If a person sells a stock for ₹150, then the LTP at the time will be ₹150. The very next second, if a stock is sold for ₹149, then the LTP changes to ₹149. This is the reason why stock prices fluctuate every second.

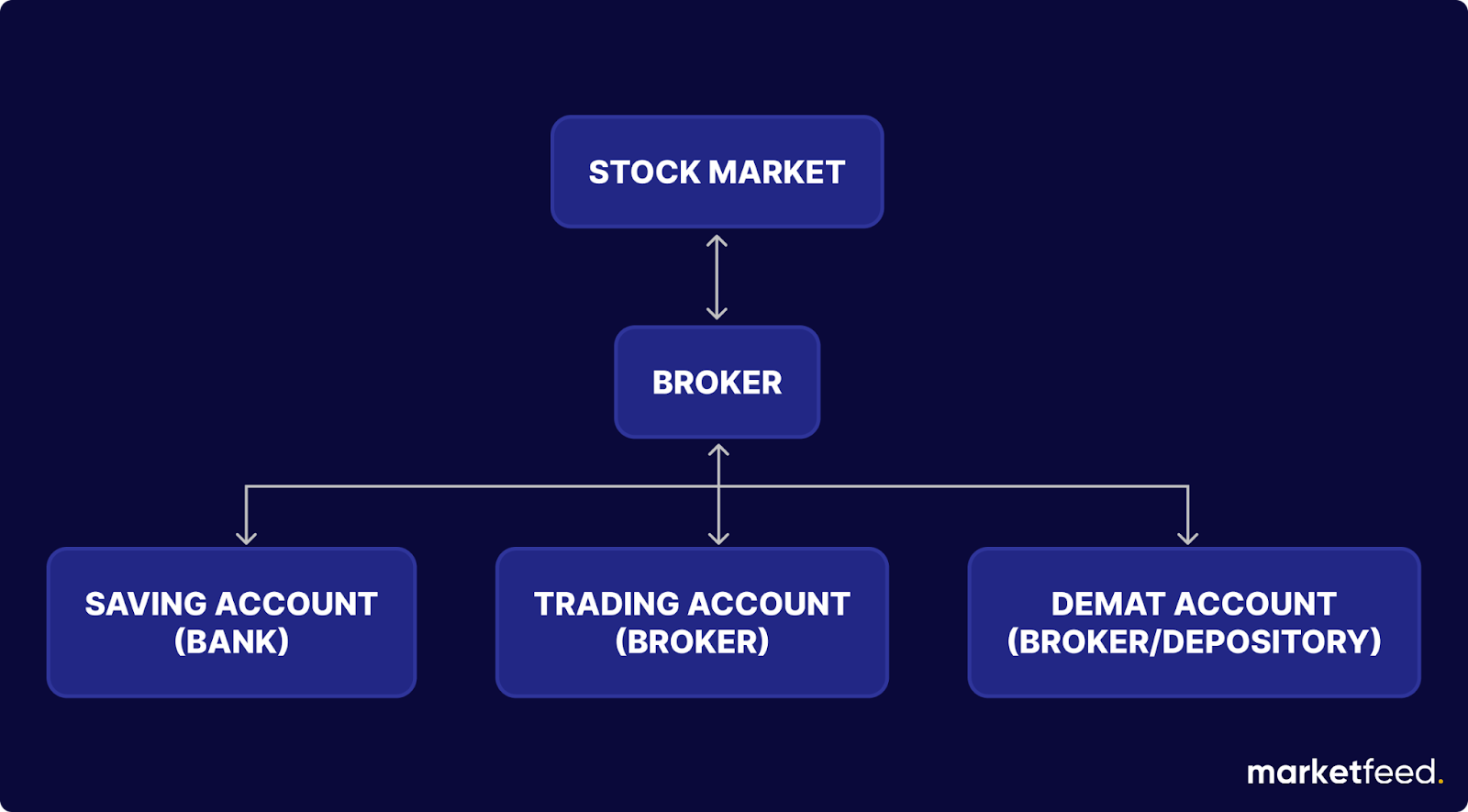

Who are Brokers?

If you want to buy a stock, you cannot do it directly from the stock market. We have to approach a stockbroker, and the broker will transact on our behalf. A broker is an intermediary that facilitates transactions in the stock market. If you want to buy a stock, your broker will find a seller in the stock market on your instruction and facilitate the transaction between you and the seller.

Before technology evolved, an investor had to physically visit the broker’s office and instruct them to buy the stock. The broker would then physically go around the stock market, find a seller, and conduct the transaction. But now, technology has evolved, and transactions can be conducted via our phones. Brokers are accessible on computers and smartphones, and investing & trading are as easy as ever.

It is absolutely necessary to have an account with a broker to participate in the stock market. As intelligent stock market participants, we must have multiple broking accounts for different purposes. We can use one account for our long-term investing activities and another one for trading. Successful traders use multiple broking accounts for different trading strategies.

How Does a Broker Work?

There are two accounts that we open with a broker. Even though they are two separate accounts serving different purposes, both of them come in a bundle.

1. Demat Account A Demat account or dematerialisation account allows you to hold your shares in an electronic format. It converts the physical shares into an electronic form, therefore dematerialising them. Demat accounts are maintained under depositories.

Earlier, the proof of ownership of shares, bonds, or debentures was in the form of physical share certificates. However, this system had many drawbacks, such as the risk of losing the certificate, fire hazards, getting wet, or even a mismatch in the signatures.

2. Trading Account A trading account acts as an interface between the investor’s bank savings account and a broker. For the broker to conduct trading activities on our behalf, they need money. We transfer the money we have in our savings account to a trading account with which the broker then conducts trading activities. Money can be transferred using net banking or UPI.

If we want to buy a stock, we instruct the broker to buy the stock, and the broker uses the money we have in our trading account to conduct the transaction. Similarly, when we sell a stock, the proceeds of the sale come directly into the trading account.

An Illustration to Understand How Demat & Trading Account Works

Arun wants to buy a share of Mahindra & Mahindra (M&M) from the stock market. The first step that Arun should take is to open a Demat and trading account. Arun opens a Demat & trading account with a leading broker and deposits money into his trading account by transferring from his bank savings account via UPI.

When the market opened at 9:15 AM, Arun placed an order with his broker to buy 1 quantity of M&M stock. The market price of M&M at the time was ₹1000. His trading account was debited ₹1000 by the broker to finance the transaction. Apart from this, a small amount was deducted as taxes and charges.

Even though the transaction was completed, the stock will only be transferred into his Demat account after T+1 days, which means he will receive the stock in his Demat account on the next working day.

While selecting brokers, we should choose the brokers that satisfy our various investing and trading needs. YOu can open a Demat and trading account using the links given below:

(Full disclosure: These are affiliate links. Do use the links if you wish to support us at no extra cost. ❤️)

Click here for step-by-step instructions on how to open a Demat and trading account.

What are Depositories?

If your shares are held by the broker, there is a risk of the broker running away with the shares they have. As a remedy, all Demat accounts are maintained by depositories. A depository is an institution that acts as a custodian of Demat accounts and shares. A Demat account is opened by a depository participant, who acts as an intermediary between the depository and investors.

There are two depositories in India, which are governed by the Government of India:

1. CDSL – Central Depository Services Limited 2. NSDL – National Securities Depository Limited

Who are the Other Facilitators?

The other facilitators part from brokers, depositories, and depository participants are:

Clearing Houses – It is an intermediary between buyers and sellers of financial instruments. It is an agency or separate corporation of a futures exchange responsible for settling trading accounts, clearing trades, collecting and maintaining margin monies, regulating delivery, and reporting trading data.

Transfer Agents – A transfer agent keeps records of who owns a publicly traded company’s stocks and bonds. They also ensure investors receive dividends on time.

Settlement Banks – It refers to a customer’s bank where payments or transactions are finally settled and cleared for customer use.

What is a Market Regulator?

The Indian stock market is a place where transactions worth lakhs of crores of rupees take place. The Securities and Exchange Board of India (SEBI) is a regulatory authority established under the SEBI Act 1992. It’s the principal regulator for stock exchanges in India. SEBI’s primary functions include protecting investor interests and promoting and regulating the Indian securities markets. It is a government organisation. SEBI exists as the watchdog to make sure nothing wrong is happening in such a massive money-involved ecosystem.

Throughout the article, we discussed the various participants in the stock market and how they all work together in the stock market. We’ve also understood the basics of what the stock market is, who its participants are, and how it works!

We often come across a lot of different financial ratios with complex names and become confused about the kinds of metrics to use when analyzing different companies listed in the stock market. In this article, we will discuss how to analyse the debt and valuation of a company (by using Tata Steel as an example).

Understanding Debt and Valuation

Debt refers to the total amount of money that a company owes to external creditors or lenders. It can arise from various sources, including loans, bonds, lines of credit, and other forms of borrowing. When a company borrows money, it agrees to repay the borrowed funds over time, often with interest. Companies take in debt for financing operations, expanding their business, investing in new projects, acquiring assets, or managing cash flow fluctuations. Debt can be an important tool for companies to raise capital and achieve their growth objectives. However, it also comes with the responsibility of making regular interest payments and eventually repaying the principal amount borrowed.

Meanwhile, valuation means finding the real worth of a company. Market participants use it to determine the price they are willing to pay or accept when selling a business. Thus, value investing is based on the true value of a business compared to its market value.

The market value of a business is the worth that the market assigns to it. To calculate the market value of a publicly traded company, multiply its share price by the number of outstanding shares.

Intrinsic value is the true and accurate worth of a company. It is the anticipated or calculated value determined through fundamental analysis.

If the market value of a company is higher than its intrinsic value, then the stock is currently overpriced or overvalued. On the other hand, if the intrinsic value of a company is lower than its market value, then the company is undervalued.

Debt Analysis Ratios (Leverage Ratios)

For a company, debt (leverage) is like a double-edged sword. They can scale their business and improve sales with the help of debt funds. However, if not used wisely, the interest to be paid for these borrowings can eat up the company’s profits. It could also lead to a crunch in the cash reserved for future operations.

The following are the different types of leverage ratios:

1. Debt-to-Equity Ratio

Equity is the value attributable to the shareholders of a company. It is calculated by subtracting liabilities from the value of the assets. The debt-to-equity ratio tells us how much borrowings are present in a company compared to its equity.

Debt-to-Equity Ratio = Total Debt/Total Equity

We can find the total equity of a company in its balance sheet. By adding the borrowings from the current and non-current liabilities, we get debt. For Tata Steel, the ratio stood at 0.76X in FY23, which means that for every ₹1 equity in the company, there exists ₹0.76 as debt. A higher Debt-to-Equity ratio indicates a higher amount of debt compared to equity.

From the graph shown above, we can conclude that Tata Steel has been able to reduce its debts, although it has increased slightly this year. The company’s Debt-to-Equity ratio is also aligned with the industry average. We can also conclude that the steel sector is capital-intensive, and each manufacturer has to raise funds through debt to conduct its operations.

2. Interest Coverage Ratio

The interest coverage ratio helps us to know how much the company can earn with respect to its interest payment. It is also known as the debt service coverage ratio.

Interest Coverage Ratio = Earnings Before Interest & Tax (EBIT) / Finance Cost

To calculate EBIT, we add Finance Cost (listed as an expense) to the Profit Before Tax (PBT). For Tata Steel, the Interest Coverage Ratio stands at 5.29, which means for every ₹1 paid as interest, the company can generate ₹2.29 as revenue. A decreasing interest coverage ratio tells us that the company does not generate enough revenue to service its debt.

In the graph above, Tata Steel’s interest coverage ratio was higher than peers in FY22 but fell to the industry average in FY23.

Valuation Ratios

As stock market investors, it is always ideal to buy shares of a company when it has a cheaper valuation. Valuation is the process of determining the true value of an asset or company. For example, the real estate prices of a particular plot surge when there is an announcement of a new township or tourism project. The ones who bought the plot earlier at a cheaper rate tend to enjoy the higher valuation of the property.

Similarly, investors can measure the valuation of each stock they invest in.

1. Price-to-Earnings (P/E) Ratio

The Price-earnings ratio gives you an insight into how much the stock market participants are willing to pay for the stock for every ₹1 profit generated by the company.

Price-to-Earnings Ratio = Current Market Price/Earnings Per Share (EPS)

To calculate EPS, we divide the net profit of a firm by the total number of its shares. Tata Steel’s P/E stands at 14.57, meaning that for every ₹1 profit generated by the company, investors are ready to pay ₹14.57.

Tata Steel is slightly undervalued compared to peer companies. Meanwhile, JSW Steel is valued at a P/E of 39.89, making it a more expensive option.

Every industry/sector has a different range of valuation. Thus, we cannot define a standard P/E range for all stocks. Therefore, we must compare the valuation to its industry averages.

2. Price to Sales (P/S) Ratio

We used Earnings Per Share (EPS) for calculating the P/E ratio. However, changes in tax slabs, new accounting rules, one-time payments, etc. can influence EPS. To overcome this, we can consider the total sales of a company to find its valuation. A low price-to-sales ratio (P/S) means that the company is relatively undervalued.

Price-to-Sales (P/S) ratio = Current Market Price/ Sales Per Share

To calculate Price-to-Sales ratio, we divide a company’s revenue from operations by the total number of shares. The P/S of Tata Steel stands at 0.52, which means that for every ₹1 earned as revenue, the company’s investors value it 0.52 times.

Tata Steel has a low P/S ratio.

3. Price to Book (P/B) Ratio

Suppose a company ends its operations after liquidating assets and settling all debts. Any final amount remaining within the firm has to be distributed amongst its investors. This amount is known as the book value of a company.

The sum of the total equity and cash reserve from a company’s balance sheet is its book value. By dividing the book value by the total number of shares, we get the book value per share.

Price to Book Ratio = Current Market Price/Book Value Per Share

For Tata Steel, the P/B ratio stands at 1.24, meaning that the stock is trading at 1.24 times its book value.

Here, JSW Steel has a P/B ratio of 3.15, which means it has a higher valuation. Conservative investors can consider stocks whose P/B ratio is close to 1. For modern and asset-light businesses, P/B will always be on the higher side.

Using Debt and Valuation Analysis for Investing

In the world of finance and investment, making informed decisions is key to success. Two essential tools that play an important role in this process are debt analysis and valuation analysis. Let’s explore why these tools are vital for investors seeking to make smart investment choices:

Risk Mitigation: Debt analysis allows investors to assess a company’s financial health by examining its debt levels. This helps in understanding the risk associated with an investment. High debt can be a red flag, indicating potential financial distress, while low or manageable debt levels can instil confidence in an investment’s stability.

Valuation Analysis: It involves estimating the intrinsic value of an asset or company. By comparing this value to the current market price, investors can determine whether an investment is overvalued or undervalued. Making decisions based on valuation analysis can prevent overpaying for assets and enhance long-term returns.

Portfolio Diversification: Understanding the debt and valuation metrics of different investments enables investors to build a diversified portfolio. A well-diversified portfolio spreads risk, reducing the impact of poor-performing assets and increasing the potential for overall returns.

Long-Term Success: Debt and valuation analysis provide the foundation for a disciplined investment strategy that considers both short-term fluctuations and long-term growth prospects.

Finding Opportunities: Valuation analysis can uncover undervalued assets or companies with growth potential. These opportunities might not be apparent without a systematic assessment of valuation metrics.

Enhanced Returns: Making investments based on thorough analysis can lead to improved returns over time. By buying undervalued assets and avoiding overvalued ones, investors increase their chances of profiting from market inefficiencies.

Limitations of Debt and Valuation Analysis

While debt and valuation analysis are valuable tools for investors, it’s essential to acknowledge their limitations to make well-rounded investment decisions. Here are some key limitations to consider:

Incomplete Information: Financial statements can sometimes lack crucial information, and companies may use accounting methods that make their financial health appear better than it actually is. This can lead to inaccuracies in debt and valuation analysis.

Market Sentiment: Market sentiment and investor behaviour can heavily influence stock prices and valuations. These factors may not always align with a company’s fundamentals, making it challenging to predict short-term market movements.

Economic Factors: Economic conditions (such as recessions or economic booms) can significantly impact the performance of companies and their debt obligations. Debt analysis may not fully account for these external factors.

Industry Specifics: Different industries have varying debt norms and valuation metrics. What’s considered acceptable in one industry might not apply to another. Ignoring industry-specific dynamics can lead to inaccurate conclusions.

Future Uncertainty: Debt and valuation analysis rely on historical data and assumptions about the future. Unexpected events, changes in market conditions, or shifts in a company’s strategy can disrupt these assumptions and render analyses obsolete.

Limited Scope: Debt and valuation analysis often focus on quantitative aspects, overlooking qualitative factors like company management, industry trends, and competitive dynamics. These qualitative factors can significantly impact a company’s performance.

Note: Never try to analyse a company with only one kind of ratio. Using multiple ratios and comparing them with metrics of peer players across a specific time period will give us a comprehensive insight into a company.

A stock buyback refers to the situation when a company decides to buy back its own shares from its shareholders at fair market value. In a stock buyback, a company reabsorbs a part of its ownership and rights and reduces the total number of shares in the market. A company can decide to buy back its shares from the open market, retail, institutional or non-institutional shareholders. One point to note here is that the buyback of equity shares cannot exceed 25% of the total paid-up equity shares.

Why Would a Company Buy Back its Own Shares?

When a Company Believes it is Undervalued

When a company believes it is undervalued or when it believes that the shares are trading at a cheap price, it may announce a buy back. When a company does so, the number of outstanding shares decreases and there is a subtle buying pressure and a bullish sentiment that gets created.

Improving Financials

A company performs a buyback when it wants to make its fundamental financial figures seem good. By reducing the number of shares in the market, the company’s Earnings per Share (EPS), Return on Assets (ROA), and Return on Equity (ROE) see a positive impact because of the buyback. Earning Per Share: The formula for EPS calculation is (Net income – Dividends/ Average Outstanding Shares). When the number of outstanding shares reduces, the EPS will increase.

Return on Assets: The ROA is calculated by dividing the Net Income by the number of Assets. In a buyback, the company’s ‘Share Capital’ or the portion of the company’s equity that is listed, is counted as an ‘asset’ of the company. When this ‘Share Capital’ reduces, so do the company’s total assets. This increases the Return on Assets of a company.

Return on Equity: The ROE is calculated by dividing the Net Income by the shareholder’s equity. A buyback decreases the shareholder’s equity, thereby increasing the Return on Equity.

When it Has Too Much Cash Lying Idle

When a company has too much cash lying idle and not many projects to invest in, it may opt for a buyback of shares. This excess cash is given back to its investors. When a company buys back its shares, it reabsorbs and retains its ownership of the company. This may give a company more control over the decisions of the company.

To Avoid Unfriendly Takeover by Other Companies

Sometimes companies may not want hostile takeovers from unwanted companies. To ensure that a hostile takeover does not happen, companies often tend to announce buybacks. One such example is the hostile takeover of Mindtree by L&T Infotech. Mindtree had planned for a major share buyback to wall the unfriendly takeover by L&T Infotech, but later decided against it.

A share buyback comes with many challenges. The question of why the company is spending money on the buyback, instead of investing the money to make the company better. It may give an unrealistic picture of the financial health of the company since a change in shareholding is not reflective of the cash flow or performance of a company. There might be regulatory barriers that a company might face in a buyback. Companies performing a buyback might decrease dividend payout. Overall buyback is a very powerful tool to promote positive sentiments about a company in the market.

How Do I Apply for a Buy Back?

You can apply for the buyback through offline and online mediums. The company that has announced the buyback will send a physical offer letter to its shareholders. The shareholders can fill out the form and send it to the necessary address or scan and send a digital copy where required.

On the other hand, if you wish to participate online, then each broker has a separate process to enroll for a buyback. Contact your broker to know more!