A few days back, Shapoorji Pallonji Group decided to sell off its 18.4% stake in Tata Sons. The Shapoorji Pallonji Group(SP Group) is headed by Pallonji Mistry and his son, ex-Tata Chairman Cyrus Mistry. The Mistrys and Tatas have been associated with each other for the past 70 years. Their relationship has turned sour in the past few years.

The reason why SP Group and the Tatas were in news was since SP Group which has been hit by a liquidity crunch intended to raise capital by putting their 18.4% stake as collateral. This did not go down well with Ratan Tata. He did not want their stake to go in the wrong hands. A battle followed in the courts. How did Ratan Tata’s relationship with Cyrus Mistry turn sour? Why is SP Group selling its complete stake in Tata Sons? Let us find out what lead the long-time friends turning into foes.

Cyrus Mistry Ratan Tata’s Blue Eyed Boy

Ratan Tata had immense faith in Cyrus Mistry. In fact, it was him who declared Mistry as his successor as Chairman of Tata Sons in 2013. Shortly after he was appointed as chairman, many of his business decisions did not go down well with Ratan Tata. Tata felt that many of Mistry’s decisions were against the ethics and morals of the company and that some of his decisions didn’t do justice to the Tata name. After all, Tatas are admired for their ethics.

Ratan Tata earlier offered Mistry to resign voluntarily, he even asked his close confidante Nitin Nohria, also the Dean of Havard Business School and Director at Tata Sons, to convince Mistry to resign voluntarily. Mistry failed to comply. He was voted out as chairman by the Tata Sons Board on 24 October 2016. Thereafter he was voted out of every possible board, making the bitterness between Ratan Tata and Cyrus evident.

Why does SP Group want to Sell Off Their Stake?

SP Group hasn’t done very well in the past few years. The company has accumulated a lot of debt. The company works mostly in the real estate and infrastructure sector which hasn’t performed well over the past year. When COVID struck, the situation worsened. SP Group currently owes debt worth Rs 28,000 crores.

In the past, SP Group has already pledged a few its shares in Tata Sons to raise a capital close to Rs 1,437 crores. However, SP Group missed the deadline for payment. This was worth worrying for many at Tata Sons.

Tata’s Worry

While SP Group still owed the debt, it decided to raise capital by pledging shares it has in Tata Sons. They wanted to raise money to finance themselves by keeping Tata Sons shares as collateral. In case SP Group fails to pay, the shares might be transferred to the creditor. This did not go down well with Ratan Tata since he did not want Tata Sons’ shares to go into the hands of an unfriendly investor.

Tata Sons Board approached the Supreme Court. The plea was to restrict the SP Group promoters from raising capital by pledging their shares in Tata Sons. Their plea was that under the company’s articles of association (AoA), the board of Tata Sons has the first right to buy the shares at fair market value. The move shattered SP Group’s hope of raising the capital of Rs 3,750 crores from Canadian Investor Brookefield as well.

Coming To A Common Ground

Recently, SP Group confirmed their intentions of selling their complete 18.4% stake in Tata Sons. SP Group said in an official statement: “a separation from the Tata Group is necessary due to the potential impact this continuing litigation could have on livelihoods and the economy”.

The best-case scenario for SP Group would be to get a fair value for its stake in the Tata’s in order to get their company out of a liquidity crisis. The value of the 18.4% stake which SP Group has in Tata Sons is 1.78 lakh crores or $24 Billion. Such a big amount may not be covered at one-go but in parts, a proposed by Tata Sons.

Apart from a few companies like TCS, none of the Tata Companies have faired well this quarter owing to the COVID-19 pandemic. For Tata Sons, the problem of arranging funds and deciding on the fair value of the purchase still remains. Tata has set up a team for contingency fund planning, which shall decide on how to arrange funds to buy out the stake owned by the Mistrys.

TCS’s buyback has given Tata Sons some relief. Tata Consultancy Services’ buyback of shares has infused close to Rs.11,000 crores in Tata Sons. This gives Tata some liquidity to begin the acquisition in parts if it decides to do so.

Also recently, there were unconfirmed reports about Walmart investing around $25 Million into Tata Group’s proposed ‘super app’, which will bring all of Tata’s Retail channels under a single app. The amount to be invested by Walmart and the amount which Tata shall give to SP Group is a close figure… What do you think is cooking up?

We had talked about Majesco on The Stock Market Show, earlier this week. While going through the fundamentals of the company, we found some very interesting things. So let’s discuss!

Share Price of Majesco Limited

27th March 2020: Rs 218.75

7th October 2020: Rs 844.90

Within 6 months, Majesco Ltd. has given a staggering return, as shown above. This makes us wonder why this stock is not catching much attention. We bring you everything you should know before you choose to invest in this stock.

(Disclaimer: We are not advising you to buy or sell any stock. This is only for educational purposes only.)

About Majesco Ltd

Majesco provides insurance software solutions, consulting and other technology-related services for the existing insurance companies. The company was incorporated as Minefields Computers Private Limited on 27th June 2013. Later, the name was changed to Majesco Ltd. Interestingly, the company is listed on the US Stock Exchange NASDAQ, as well.

The company masters in services related to cloud-computing, microservices-based and API-enabled services. They are one of the first companies to move to the cloud. Thus, giving them a headstart for the future. It offers insurance software solutions for General Insurance, Life, Annuities (L&A), and Pensions & Group or Employee Benefits providers. Majesco is present in several countries like India, Malaysia, Thailand, Canada, Singapore, New Zealand, The United States and more.

On a global level, the company offers its services to more than 190 insurance carriers. Few of its clients are Religare Life Insurance, AON, Burns & Wilcox, Erie Insurance, Hansard Global PLC, IDBI Federal Life Insurance, Sun Life Malaysia, US Assure and many more.

Business Strategy

Majesco projects itself as an InsurTech partner. InsurTech means involvement of technology in the insurance industry. It provides insights to insurance companies to help them accelerate their digital transformation. With the help of Machine Learning, Robotic automation, AI and IoT (Internet of Things) company aim to improve its efficiency and reduce costs.

As mentioned before, Majesco provides cloud-based solutions to its clients. Total cloud revenue from P&C (Property and Casualty insurance) amassed to Rs 302.82 crores. Similarly, Total cloud revenue from L&A (Life and Annuities) amassed to Rs 116.82 crores. In the last one year, the company has witnessed a revenue increase of 35.6% in its cloud subscription business.

Financial Performance

FY19-20 was a year of dominance for the company. Global and Indian economy had been volatile before the pandemic, yet the company continued its upward trajectory. They saw robust growth in their top line (revenue) as well as in the bottom line(net profits). Majesco’s total revenue saw a modest rise of 5% from Rs 1,016.20 crores to Rs 1,040.48 crores last year. But, their profits increased by more than 25%. Their net profit at the end of FY18-19 was Rs 71.74 crores. It increased to Rs 90.22 crores in FY19-20.

(Source: Annual Report 2019-20)

(Source: Annual Report 2019-20)

By digging deep into the company’s financials, we got great insights. Majesco registered an increase in their expenses from Rs 916.14 crores to Rs 959.87 crores. This increase was chiefly due to a 5% increase in employee benefit expenses. It shows that the company is further looking to invest in its human capital and aims to keep its employees happy. At the same time, the company’s finance cost has been decreasing. This is again a positive sign because a company is paying less interest on its debt. Thus, the company is managing its liabilities well.

Earnings per share is an important metric to check how much a shareholder is gaining from an investment. It shows the company’s total profitability. To further know more about the EPS, click here. In just one year, Majesco’s EPS has grown by more than 26%. Last year, the company’s EPS was 19.14 which rose to 24.28 by FY19-20. With the proposed share buyback, EPS will rise even further.

Strong Cash Position

Liquidity is very important for any company to remain stable. The most liquid asset is Cash. The amount of cash within a company’s cash flow statements explains how well the company is doing. Majesco’s cash position in the last year has shown exceptional growth. Total cash and cash equivalents at the end of FY18-19 was Rs 109.86 crores. This has grown 3X times to Rs 342.95 crores in FY19-20.

(Source: Annual Report 2019-20)

In an age where companies are borrowing to expand, Majesco’s non-current liabilities have actually decreased by 20%. Last year, this amount was amassed to be Rs 71.95 crores which has fallen to Rs 56.58 crores.

Two possibilities arise when a company has a good amount of cash with themselves. Firstly, they either look to invest for further expansion and secondly, they can go for a share buyback. The second option gives the promoters a stronger hold on their company. They become more flexible in making decisions. A share buyback also signals the positive confidence of promoters in their organisation.

Majesco Limited is currently exploring the path of utilizing the cash to buy back the shares. On October 8, the company’s board approved the proposal to buyback up to 74,70,540 fully paid equity shares at Rs 845/share. Shares of Majesco are currently trading above Rs 870. You can go through the company’s annual report or through its investor presentation to find out more.

On 5th October, all eyes were focused on the 42nd Goods and Services Tax (GST) Council meeting. An important decision had to be made with respect to the ‘compensation cess issue’. There always seems to be a lot of complicated terms and facts surrounding this topic. Let us understand with clarity, how this issue came about. When it comes to a matter of such great importance, why are the Central government and states facing difficulties in reaching an agreement?

What is the GST Compensation Cess?

Taxes collected by the Government can be divided into Direct Taxes and Indirect Taxes. The Goods and Services Tax (GST), which was introduced in India on 1st July 2017, has replaced the indirect tax structure for the entire country. It is based on the slogan ‘One Nation, One Tax, One Market’. One of the advantages of GST is that it integrates different taxes like Central Excise, Service Tax, Sales Tax, Luxury Tax etc. into one consolidated tax. It prevents multiple taxes being imposed on goods and services.

GST is further divided into three parts- Central GST, State GST, and Integrated GST. These are taxes that can be passed on to another entity or individual. For example, when a particular product is manufactured in Tamil Nadu but is consumed in Kerala, then the revenue from GST collection is given to Kerala (the state where the product was consumed). Due to this feature of GST, certain manufacturing states of India believed that they would suffer from losses in revenue. Thus, the GST Compensation Cess was launched by the Central Government to compensate for any revenue loss that would come up in these manufacturing states. Cess is nothing but a tax imposed on a tax amount. You may have seen GST Cess in the bills you get from the your petrol pump. Anyway, when this relief for states was introduced, the GST Bill stated that the cess would be imposed for a period of 5 years, ie, till 1st July 2022.

It might be interesting to know that GST Compensation Cess is applicable to certain specified products such as Pan Masala, Cigars, Tobacco, Cigarettes, Petrol, LPG, Motor Cars and Vehicles. These products can be categorized as luxury, sin, and demerit goods. So products which the governments think you should not use or use less or ones which are used only by the rich are included in these lists.

How is GST Compensation Cess amount calculated?

While calculating the amount for GST Compensation Cess, the growth rate of a state is assumed to be at 14% per year. Based on this information, a state’s projected revenue that they could have earned in absence of GST, is calculated. The total compensation cess payable to a state will be the difference between the projected revenue (for the financial year) and actual revenue collected by the state.

States vs the Centre

Now that we have an idea about GST and GST Compensation cess, let us know why there has been a ‘GST compensation row’ and why states are not happy with certain decisions.

As we all know, revenues of state governments have dried up due to the ongoing Covid-19 pandemic. The states have high expenses, and GST collections have gone down. As a relief measure, the Central Government assured that all states would be compensated, and that they will not face a shortage of tax money. The amount calculated as the total of GST revenue shortage and revenue shortage due to Covid-19 (these are separate estimates calculated by the Centre) was Rs 2.35 lakh crore. With this new estimate, the Centre established two options during the previous GST Council meeting, which was held on 27th August:

In consultation with the Reserve Bank of India (RBI), the Centre would give states a special window to borrow Rs 97,000 crore, that could be paid back after 5 years. This amount was calculated as the GST revenue shortage.

States could directly borrow Rs 2.35 lakh crore from the market, but this would come at a higher cost.

Things have been tense since this announcement took place. A majority of the states have already opted for the first option. However, ten states and union territories, which include Kerala, West Bengal, Delhi, Tamil Nadu, Punjab, and Chattisgarh have completely refused to accept both options and started protests. In both the cases, the states are responsible of borrowing and paying back this allocated ‘funds’. What these states have demanded is that the Centre should borrow the required funds, not the states, and that it should be allocated to them.

What happened at the 42nd GST Council meeting?

After the 42nd GST Council Meeting on 5th October, the Centre and States governments have not yet reached an agreement on the compensation borrowing options. However, major new updates were given by Finance Minister Smt. Nirmala Sitharaman:

The borrowing limit has been increased to Rs 1.1 lakh crore, instead of the first option that was mentioned earlier. This would be the new amount for the GST revenue shortage.

The Centre would release a compensation of Rs 20,000 crore to all the States, which would help cover the revenue loss during 2020-2021.

Another amount of Rs 25,000 crore will be released for Integrated GST (or IGST). IGST is charged when there is movement of goods from one state to another.

The GST Compensation Cess would be applicable even after the specified 5 year period, ie, it would go beyond June 2022 to meet the revenue gap.

From 1st January, small businesesses whose annual turnover is less than Rs 5 crore will not have to file monthly tax returns, need to file it only quarterly. And payment of taxes can be made using a challan. This would give relief to a lot of small taxpayers

Since the beginning of this financial year, no compensation cess has been given to the states. An important factor we must understand is that states are now at the forefront of fighting Covid-19, and they need much more resources than the Centre. Finance Ministers of states have already asked the Government to reverse its decision of making the states borrow. But the Centre has suggested that they are not willing to change the options. The next GST Council meeting is scheduled for 12th October.

As investors, we need to go through market news on a daily basis, as it would help us make important decisions. During the past few weeks, you might have read or heard about GMM Pfaudler. The company comes under India’s heavy engineering sector and is now under the scanner of regulatory authorities due to serious allegations of insider trading. Let us dive into the details of how the multibagger stock came into the spotlight, and how its latest offer for sale is too good to be true.

Company Profile

Firstly, we shall look into a brief history of the company, and how it has evolved over the years. GMM Pfaudler was established as a joint venture of Gujarat Machinery Manufacturers (GMM) and Pfaudler Inc. (an American multinational company that invented glass-coated steel). Ever since the technical collaboration began in 1987, the company has been a leading supplier of essential glass-lined and non-glass lined equipment for the pharmaceutical and chemical industriesaround the globe.

In 1999, US-based Pfaudler increased its stake in GMM to 51%, and it was at that point when the company was renamed GMM Pfaudler. Since the demand for their products is always high, the company has been showing great potential ever since its inception in the Indian market. It is notable that in 2015, Deutsche Beteiligungs AG (DBAG), a German equity company, acquired Pfaudler Inc.

Over the past few months, the company’s stock was rising sharply and had outperformed the Nifty 500 index. Its earnings grew by 27.7% over the past year. There has been a 6-time increase in share price since March 2018 to a high of approximately Rs 6,900 per share in August 2020.

GMM Pfaudler manufacturing plant in Gujarat. (Picture sourced from the company website)

Recent Developments

The company’s low-float stock (these are stocks with a low number of shares and more institutional ownership) has shown a decline of 35.97% since August 2020 on the NSE. This specific period in time becomes very important, as the company makes a major announcement. GMM Pfaudler would buy a 54% majority stake in its parent company, the Pfaudler Group, for $27.43 million (~Rs 202 crore). This stake would be acquired directly, and through its subsidiary called Mavag AG, while 26% would go to Indian promoter Patel Family, and the rest 20% would remain with the German company DBAG. It is interesting that GMM Pfaudler is buying stake in the international Pfaudler group. To fund this acquisition, GMM Pfaudler and its subsidiary will use its own reserve of earnings up to Rs 75 crores ($10 million) and also take on a debt of Rs 130 crore ($17.4 million). The question that comes to mind is, was this a necessary transaction?

In September, another major development that took place was their new issue of an offer for sale (OFS). An OFS refers to a method by which the promoters of a company sell a part of their existing shares and get an exit.

It was on 22nd September that GMM Pfaudler announced an offer for sale at a floor price of Rs 3,500 per share. This was a 33% discount from the previous closing of Rs 5,241. What this means is a sale of a 17.6% total stake of the promoters at a very high discounted rate. This could actually be a strategy to bring in high-quality, long-term investors into the company.

Things have been quite chaotic since then. What happened just before this announcement is what potential investors are worried about. A lot of positions were taken in the Stock Lending and Borrowing Mechanism (SLB) in NSE. In simple terms, SLB is a method by which traders can borrow shares that they do not already own, or can lend stocks that they own. So, a lot of shares were borrowed using SLB, and shorted (sold) during the OFS. It is quite strange when we check the SLB data, as it shows that a lot of activity has taken place from 11 August to 25 September- a total of 87,283 shares were borrowed. Also, the management did not produce a caution statement when stock prices went through the roof with abnormally high valuations, as this would have helped new investors to think about investing at high prices. Promoters of GMM Pfaudler had been selling shares below Rs 3,845, which might imply that lower prices are reasonable for them. This is what led to the allegations of insider trading, as the ‘insiders’ did not buy shares themselves, and rather, were trying to sell them off.

In the days that followed, stocks of GMM Pfaudler started declining by a maximum daily limit of 10% to Rs 4,717. The lowest price touched by the stock during this period was at Rs 3,432 on 29 September, which was even below the OFS price. On that day, Plutus Wealth Management, a UK-based financial advisor, bought 1,65,000 shares of GMM Pfaudler at Rs. 3,528.75 per share from the open market. On the same day, stock prices were locked in a 5% upper circuit at Rs. 3,821. For further clarity, an upper circuit refers to the price of a stock that cannot be traded beyond a specified limit on a particular day. After this update of acquisition of shares by Plutus Wealth, what we saw the next day was a further 5% rise in share prices of GMM Pfaudler, to Rs 4,012.

The Managing Director, Tarak Patel has addressed these allegations, stating that the company would help or assist any regulator who would investigate the serious claims. It is noteworthy that GMM Pfaudler’s insiders (or promoters) DBAG, would own roughly 32% stake and the Patel family would have 22% even after the offer for sale. The MD also stated that the promoters would remain with the company for a minimum of 3 years, and are not presently cashing out their stake. SEBI or other regulatory bodies would investigate the matter, and check for any irregularities in the company’s records.

An important takeaway of this whole situation as explained by experts is the fact that investors need to be very careful, and be aware of the risks involved when investing in a company whose valuations are very high. And when huge discounts are given for an Offer for Sale (OFS), it means that even the promoters don’t believe in the current valuation of the company. The stock currently trades below Rs 3,800 (as of 6 October).

The world around us is changing at a very rapid pace due to advancements in technology. Like other countries, India has also undergone a lot of changes. One of the major reasons for this transformation in India is Mukesh Ambani-led Reliance Jio. Ever since Reliance Communications (RCom), Mukesh Ambani’s brainchild, was snatched away from him by his younger brother, Asia’s richest man was planning his comeback to telecom. Today, we are going to dig deep into what could be one of the most exciting businesses in Indian history.

A Brief Profile of Reliance Jio

Reliance, through Jio, aims to transform India into a digital society. Their mantra is quite simple: connect everyone and everything, everywhere.Jio’s services span across various sectors. From cloud and media to gaming, healthcare, education and much more.

Jio came into the market in 2016 with only 4G services. Yes, no 2G, no 3G, just 4G. Before its launch, they made sure that they had a robust and stable infrastructure to support future growth. It came to the market by offering customers three months of free services followed by free calls and various data plans. With this disruptive move, they were able to start a price war in the telecom sector.

But this disruption was easier than you think. Internet Service Providers (ISPs) do not incur any additional cost if you use 100MB of data or 1GB of data, so Jio came in by offering high data plans but did not lose out any money because of it, which is the best kind of disruption. Their infrastructure was strong enough to back the large number of users who joined their network.

Jio vs Bharti Airtel & Vi

Reliance Jio was India’s first telecom operator to offer the 4G Voice over LTE (VoLTE) services. This essentially meant that voice calls were placed through the internet, and hence no separate infrastructure was needed for calls. They were able to offer free national roaming as well, with their pan-India license.

On the other hand, Bharti Airtel and other Telcos stuck to their 2G and 3G services and hardly ventured into the 4G market. Their weak strategy towards the investment in new infrastructure created several obstacles for them to move into 4G completely. If Airtel wants to set up a tower in a village, it has to first set up its 2G tower, then install 3G towers, and then maybe install 4G towers. But Jio only installs 4G towers and provides high-quality data, very efficiently.

Also remember, neither did Jio invent 4G nor did they invent VOLTE. These were widely used technologies in international markets that old players did not implement due to less flexibility of high debt and old-school thinking. Even now, companies like Airtel and Vi have failed to move into 4G services completely.

According to the Telecom Regulatory Authority of India (TRAI) data, Jio’s total number of subscribers has steadily increased over the years from zero to 38.8 crore in March, making it the market leader. Airtel and Vi have 28.36 crore and 29.11 crore, respectively, in their March quarter earnings numbers.

Jio’s average per capita data consumption was 11+ GB per month for the previous financial year. With rising population and more awareness, the requirement for smartphones will only increase Jio’s customer base. Unlike other players, Ambani had the game-changing idea of providing cheap data and charging for other services like the ones below.

Source: Reliance’s Annual Report 2019-20

Who Rules the Market?

Telecom Regulatory Authority of India (TRAI) stated that the top five telecommunication operators in India are Reliance Jio, Bharti Airtel, Vodafone Idea, BSNL and MTNL. Reliance Jio dominates the industry with a 33% market share. They are followed by Bharti Airtel and Vi with 28.35% and 28.05% market share respectively. (Data as of February 2020)

Jio’s Performance

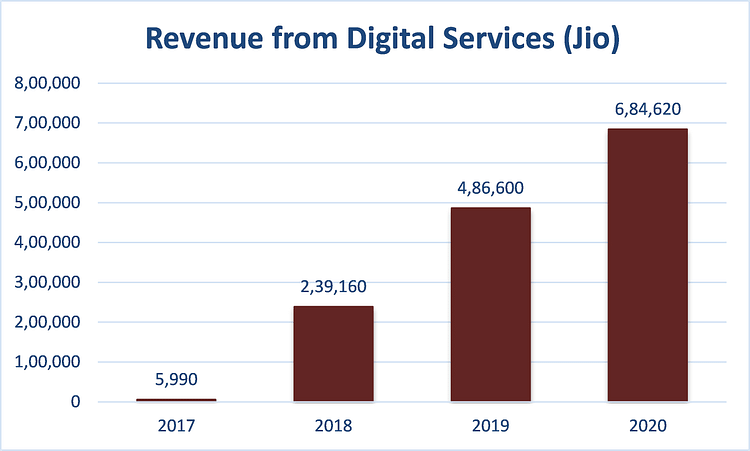

In 2017, Reliance Jio had a mere share of 0.2% in RIL’s total revenue. That year, they were making losses for the company. Fast-forward three years, Reliance Digital Services are booming at neck-breaking speed. Their share in Reliance’s total revenue has increased to more than 8%.

The biggest positive has been noticed on the bottom line side. Reliance Jio was the reason for more than one-fifth (20.5%) of the total profits to the company this year. It recorded a revenue worth Rs 5,990 crore in 2016. This increased to Rs 6,84,620 crore in 2019-20. A mighty increase of 226% in CAGR terms for the last four years.

Source: Author’s own creation

Jio recorded an Average revenue per user (APRU) of Rs 130.6 per month for the quarter ending March 2020. Their APRU increased to Rs 140.3 for the first quarter of FY21 which ended in June. Average data per usage increased to 12.3 GB per month per user in Q1FY21. This number was 11.3 GB per month per user for the quarter January-March 2020. In fact, Jio had the highest user engagement last year in the world with 5 hours spent by each subscriber per day on the Jio ecosystem.

The founder of Airtel, Sunil Mittal has mentioned multiple times that the company needs an average revenue per user (ARPU) of Rs 300 or more to survive from its current level of Rs 147. Yes, he says that this metric should double for Airtel to survive! Meanwhile, Jio is looking comfortable at its current levels and making profits while Airtel and Vi are facing huge losses. This is again tied into the logic of selling data for cheap and charging for other services.

Acquisitions by Reliance Jio

Saavn

Saavn is one of the most popular music streaming platforms in India. In 2018, Reliance merged its product, JioMusic, with Saavn by acquiring a nearly 80% stake. The merged entity was named JioSaavn so that the audience can know still associate themselves with Saavn as well as understand the presence of Jio. This backed Jio to directly compete with their telecom rival, Bharti Airtel’s Wynk, in a different sector.

Embibe

Reliance Jio ventured into the EdTech sector by acquiring an almost 73% stake in Embibe in 2018. Bengaluru-based Embibe is an artificial intelligence-based education technology provider and a competitor to Byju’s. Embibe is a very powerful entity which depends on AI and analytics to find the weaknesses of students.

It points out where the students are lagging whether is it time management, stamina, knowledge, confidence, accuracy or speed. In the middle of the pandemic, when companies were finding a way to survive, Reliance Jio invested Rs 500 crore in Embibe in April. This was the second investment in the EdTech startup in 2020. Early in February, Embibe raised a funding of nearly Rs 90 crore from Reliance Industries.

Haptik

In the first half of 2019, Reliance Jio announced that will hold about 87% of Haptik by investing Rs 700 crore over the next five years. Out of this Rs 700 crore, Rs 230 crore has already been paid. This acquisition was another move from the company to expand itself into voice-based and AI-enabled conversational products. If you were a Samsung user in 2014, you would have noticed the Hand logo of Haptik. The company has some big clients in the form of Future Retail (which is bought by Reliance Retail now. Click here to read more about it), KFC, Coca-Cola, Oyo Rooms, Samsung and more.

Reverie

In the same year, Reliance acquired Bengaluru-based technology service startup Reverie. Approximately 83.3% of the startup’s equity stake was acquired by Reliance Jio. Reverie is another company which offers voice-based products. It offers voice assistant ‘Gopal’ in 12 Indian languages like Hindi, Bengali, Marathi, Gujarati, Telugu, Tamil and more.

Tesseract

Reliance acquired a stake of 80-85% in Mumbai-based VR startup Tesseract in August of 2019. At RIL’s 43rd AGM, Isha Ambani unveiled the JioGlass which was built by Tesseract. This JioGlass is designed to enable 3D virtual rooms and conduct holographic classes. Thus, building a completely different and exciting virtual experience.

Hathway Cable and DEN

Reliance Jio acquired a 51.3 % stake in Hathway Cable & Datacom and a 66 % stake in Den Networks. This deal went through in 2019 when Reliance received the Competition Commission of India’s nod to proceed. The main reason behind this move was to procure a substantial market to launch its ambitious high-speed broadband network under JioGigaFiber. This Jio product is a fibre-to-the-home (FTTH) broadband service. It aims to provide ultra-high-definition experience on television sets, voice-activated virtual assistance and virtual reality gaming.

Shaping India’s digital future?

There are 45 crore unique smartphone users in India until March 2020. Jio has successfully become the face of Indian digital transformation.

India is still finding it very hard to contain the coronavirus. While global sentiments are weak, big players like Google, Facebook, General Atlantic, KKR, Abu Dhabi Investment Authority, and other companies are investing in Reliance Jio. This shows the high level of confidence of global leaders in the Jio model. It’s not only the investment or the funds which are coming in. But, also the guidance and suggestions from the top global leaders who are running these companies. Jio has now four strategic partners Facebook, Intel, Qualcomm and Google.

Now, Reliance Jio is coming up with plans to get 2G subscribers from Airtel and Vi to convert. An ultra-cheap Rs 4,000 smartphone is in the works to get more people in India familiarised with the internet and other services. If this happens, the user base of Jio will expand further and the market share of other telcos might shrink again. An India-made 5G solution is also ready for testing from Jio.

With Jio already being the market leader, and showing no plans to slow down, it has surely cemented its position in the Indian telecom space within 4 short years. Will it turn out to be the only player, and make the sector a monopoly? Will have to wait and watch for that.

IPO’s are at a boom right now. We covered all the details of CAMS IPO you wanted to know before it was launched a few days back. Today, we are going to talk about the Initial Public Offering (IPO) of Angel Broking.

The Angel Broking public offer is the 8th IPO in 2020, and the 7th after COVID-19 lockdown. SBI Card, Rossari Biotech, Mindspace Business Parks REIT, Happiest Minds, Route Mobile, Chemcon Speciality Chemicals and Computer Age Management Services (CAMS) are the previous seven companies to launch their IPO this year.

About the company

Angel Broking Ltd is one of India’s oldest stockbroking houses. It was incorporated in 1996. It provides broking, margin funding, advisory and financial services. The company also conducts research services and gives out investment advice.

Currently, Angel Broking is the fourth largest broker on NSE (in terms of active clients) with a market share of 6.3% as of June 2020. It has several applications like Angel Broking Mobile, Angel BEE, SpeedPro and NXT. As of June 30, 2020, Angel Broking mobile application had more than 4.3 million downloads. Also, it’s Angel BEE mobile application had nearly 1 million downloads.

The company was forced into adopting discount broking system, after the coming of new age brokers like Zerodha.

IPO Details

Angel Broking plans to raise to Rs 600 crore through the book-building issue. It will be a fresh issue of Rs 300 crore and an offer for sale of Rs 300 crore. Offer for sale means that the current promoters of the company are getting an exit. On Monday, Angel Broking raised nearly Rs 180 crore from more than 20 anchor investors. They have been allotted 58.8 lakh shares for Rs 306 each.

The quota for retail investors is fixed at 35%.QIB and NII quota are fixed at 50% and 15%. The leading book managers for this IPO are ICICI Securities Ltd, Edelweiss Financial Services Ltd and SBI Capital Markets Ltd.

One market lot consists of 49 shares. For retail investors, the minimum lot is 1 and the maximum lot is 13. That means a retail investor has to pay at least Rs 14,945 to bid for the issue. Maximum limit says that a retail investor cannot invest more than Rs 1,94,922 (13 Lots X 49 Shares X Price). The tentative date for IPO’s listing date is 5th October 2020.

IPO Date

Sep 22, 2020 – Sep 24, 2020

Issue Type

Book Built Issue IPO

Issue Size

Up to Rs 600 crore

Fresh Issue

Up to Rs 300 crore

Offer for Sale

Up to Rs 300 crore

Face Value

Rs 10 per equity share

IPO Price

Rs 305 to Rs 306 per equity share

Market Lot

49 Shares

Min Order Quantity

49 Shares

Listing At

BSE, NSE

Financial Highlights

Angel Broking’s total revenue from operations was Rs 724.62 crore in FY20. Total revenue for the month ending June or Q1FY21 was Rs 238.42 crore. During this period, Angel Broking earned 14.65% of the income from interests and 85.21% from fees and commissions. As of June 30, 2020, they have more than 21.5 lakh operational broking accounts.

Angel Broking’s Revenue and Profit After Tax is growing at a CAGR of 15% and 32% respectively. Their ROE has remained stable at 15.2 from 2019 to 2020, which is nothing extra-ordinary. The broking firm’s client base has increased from 10.6 lakh in FY18 to 21.5 lakh as on June 2020. Thus, at a CAGR of38.61%, which even though it looks good is not as good as peers. In the first quarter of FY21, they have seen a monthly client addition of 1.15 lakh clients on an average.

2017-18

2018-19

2019-20

Revenue

738.5

737

710.5

PAT

101.1

76.7

86.6

EPS

14.04

10.65

12.03

(Values are in crore rupees)

The Pros

Angel Broking is the fourth largest broking house based on active clients after Zerodha, ICICI Securities and RKSV (Upstox).

Robust client base through the online and digital platform. They also have a strong sub-broker network.

Track record of strong financial performance over the years.

Ability to use technology to cut down on costs which gives them a larger net profit margin.

Huge untapped brokerage industry. Retail trading has taken a quantum leap. Domestic broking industry’s revenue has increased by 10.5% CAGR between FY15-FY20.

Experienced management team leading the business.

The Cons

A lot of competition in the market already. Its listed peers are ICICI Securities Ltd., Geojit Financial Services Ltd., IIFL Holdings Ltd., Motilal Oswal Financial Services Ltd. and JM Financial Services Ltd. Its unlisted peers are Zerodha, RKSV Securities and 5Paisa Capital, etc. New age brokers are coming in with newer and faster tech faced products which Angel Broking may find hard to follow.

Their valuation is on a bit higher side. Its valuation is 26.84 times FY20 earnings.

Emerging low-cost brokers will pile more pressure on the company in the future to retain their clients.

Do make your own studies before investing in any company. To get a complete idea of the company, you can find the red herring prospectus submitted by Angel Broking, here.

You must have heard about the FinCEN leaks through marketfeed. Not many news outlets have given clear information about this major scandal, here is what we found.

FinCEN Leaks are a set of documents and data that have been collated by ICIJ or International Consortium of Investigative Journalists. These documentshave flagged a number of transactions made through huge international markets like HSBC, Deutsche Bank, JP Morgan, Bank of New York Mellon, Barclays etc.

These transactions were made on behalf of politicians, corporations, shell companies, businessmen, and others. They are mostly fraudulent in nature and were used to sponsor political campaigns, sporting events, corporate transactions, terrorist organizations, and many illegal and corrupt activities as well. The total amount of transactions in these papers sums up to Rs 1.46 crore crores, yes crore crores. You can try counting the number of zeroes.

Share prices for the listed banks and companies began to fall all across the world once the news was out. Let us find out what exactly was wrong with these transactions.

What was wrong with these transactions?

If one of us needs to transfer money from one bank in India to another bank in a different country, it cannot happen directly. If the transaction happens in US dollar, it HAS to go through a US Bank.

All suspected or confirmed fraudulent transactions in the US need to be reported to FinCEN or Financial Crimes Enforcement Network, a part of US Department of the Treasury. Banks or Financial institutions report these suspected transactions in the form of SAR or Suspicious Activity Report.

Enforcement Agencies in the USA like the FBI, use this data from the SAR to track fraudulent transactions and flag these wrongdoers, or so they say.

Banks that fail to report fraudulent transactions or file a SAR on time are penalized by the USGovernment. Keeping this in mind, the banks made it a point to keep a track of fraudulent transactions and file SARs when needed.

HERE’S THE CATCH!The banks can charge a transaction fee, even on these fraudulent transactions that they report. The banks kept reporting the fraudulent transactions and kept charging the transaction fee. Essentially, the banks made money for “reporting” the crime, when they should have “blocked” such a fraudulent transaction.

The banks kept filing SARs on these fradulent transactions and kept charging transaction fees when the right thing to do was to block or deny such a transaction.

The SARs report kept piling up until they were leaked by internal sources. These international group of journalists kept connecting the dots based on the transactions, linking them to powerful people around the world.

This leak showed how certain the banking system all across the world facilitated fraudulent transactions from right under the system’s nose.

What about India?

Around 44 banks were listed in the data dump, including the country’s largest bank, State Bank of India. The fraudulent transactions reportedshows that Indian banks received more than ₹3,500 crores ($482 Million) from outside the country and transferred ₹2,900 crores ($406 Million) from India. Investigative journalists are trying to connect the dots of these transactions.

So far they have found Jindal Steel, IPL Sponsoring, Gangster Dawood Ibrahim and some terrorist organisations linked to the leaked papers. Shares of Indian banks have fallen strongly, and are continuing to fall. Jindal Steel has lost almost 20% of its market cap in the last 2 trading days alone.

Also, shares of major banks around the world have fallen. Stock prices of HSBC, one of the world’s largest banks, have hit a 22-year low because of this scandal, falling even below COVID-crash levels. Global markets are falling.

How was this made possible and what can be the future course of action?

The FinCEN links were made by a dedicated group of investigative journalists at ICIJ, Buzzfeed News and 108 other agencies all across the world. The project spanned over 16 months involving partners from 88 countries.

“In all, an ICIJ analysis found, the documents identify more than $2 trillion in transactions between 1999 and 2017 that were flagged by financial institutions’ internal compliance officers as possible money laundering or other criminal activity — including $514 billion at JPMorgan and $1.3 trillion at Deutsche Bank.” read the ICIJ website.

There is no official statement by either of the companies or FinCEN itself with respect to the leaks. HSBC was fined multiple times previously for similar fraudulent transactions earlier, yet it played a major part in the FinCEN leaks. Fines may be imposed, licenses may be cancelled, those held responsible may be prosecuted, but will things get better from here? That is something only the respective Governments can answer.

To know more about the figures, people involved, processes in FinCEN leaks, ClickHere.

India is not famous for many hostile takeovers. But in 2019, we saw one such story unfurling. Today marketfeed brings you the story of one such rare takeover which took place last year.

L&T founded a lot of excess cash on their books by the end of FY19. When a company has extra cash, they generally have three options to use that cash. Firstly, roll out more dividends to make shareholders happy. Secondly, buyback shares from the open market to gain more control of the firm. This also gives a signal to the investors that the current market price of the company is lower when compared to its valuation. Thirdly, invest the extra cash to expand the company to fund future growth rate.

In June 2019, Larsen and Toubro Ltd (L&T) successfully completed India’s first hostile takeover of a software development company. L&T increased its stake to 60% in the Bengaluru-based company, Mindtree Ltd, to gain a controlling interest in the company.

Failed buyback and dividend approach

Larsen and Toubro Ltd (L&T) desired to buy back outstanding shares from the market. They went into the market with a bid of $1.5 billion. Their plans were disrupted by the regulator Securities and Exchanges Bureau of India (SEBI). They did not allow the buyback offer to go through because the debt to equity ratio of L&T would have crossed 2:1 after that. This would have violated the compliance norms laid down by SEBI.

To pay more dividends to the shareholders was also thought about. But that proposition was scrapped. In 2016, L&T gave out mind-boggling dividends. The value of dividend was almost 33% of the annual profit of the company that year. If they would have increased the dividend further, it would have set very high expectations among the shareholders. In future, if the market had contracted, it would become very hard for the company to pay out a high amount of dividend. So to control shareholder’s expectations, L&T decided not to go with this approach.

Why name it as a hostile takeover?

When the management of the target company doesn’t want the takeover to take place, it is referred to as a hostile takeover. How can a company be sold to another company against their wants? Well, running a corporate business is different from buying/selling of a random consumer product. Mindtree Ltd. is a listed company. Many individual investors and promoters held some percentage of the company’s total shares outstanding. After buying 60% of company’s total equity shares through different mediums, L&T completed this acquisition.

How did it happen?

VG Siddhartha (founder of the cafe chain Café Coffee Day) was the single-largest non-promotor shareholder in Mindtree. He had a 20.32% stake in Mindtree Ltd. L&T got in touch of him and convinced him to sell his stake at Rs 980 per share. This amassed to almost Rs 3,500 crore. Following this, they did an on-market purchase of around 15% capital shares.

L&T didn’t stop there and ventured forward to buy further stake in Mindtree from the open market. They offered to purchase 50.9 million shares of Mindtree from public shareholders for Rs 980. Large investors rushed to sell their holdings and the offer was subscribed 1.2 times. By spending Rs 4,988.82 crore more, L&T was able to buy the 31% additional stake in MindTree.

Mindtree’s opposition

It was quite obvious that the promoters of Mindtree were completely against the imminent hostile takeover by L&T. They issued multiple public statements expressing their anger and concerns for the organisation and its shareholders. They even went on to dub the takeover as a grave threat to the company.

Promoters kept on unconditionally oppose the attempt by L&T by saying that it will lead to the destruction of the company which has been running successfully since last 20 years. They did not see any strategic advantage in the deal and feared that their long-term vision of the company will be broken if the takeover takes place. One of the statements from their promoters (Krishnakumar Natarajan, Subroto Bagchi, Parthasarathy N.S. and Rostow Ravanan) is as follows:

“A hostile takeover by Larsen and Toubro, unprecedented in our industry, could undo all of the progress we’ve made and immensely set our organisation back. We’ve also carefully created a differentiated corporate culture made up of our amazing Mindtree Minds. A hostile takeover by Larsen & Toubro, unprecedented in our industry, could undo all of the progress we’ve made and immensely set our organization back. We believe it’s in the best interests of our shareholders, Mindtree Minds, and our organization overall to continue opposing this takeover attempt.”

Benefits to LTI

Mindtree had a broad range of offerings and experience in layer and cloud services. The infotech arm of L&T, LTI (Larsen & Toubro Infotech), is a global technology consulting and digital solutions Company. It has a strong presence in banking, financial services and insurance (BFSI) verticals.Mindtree had a robust hold on media and retail and consumer verticals. The two entity had very little clients overlap. Thus, making the two work on a single page will overall benefit L&T. The portfolio of clients will widen and give more opportunities to the firm as a whole. So ultimately, the deal was done to strengthen LTI and its operations, although they have not been merged yet.

What could have saved Mindtree from this takeover?

As said before, a hostile takeover in India is not common. So how did Mindtree find itself in this position? It was because of their peculiar shareholding pattern. The promoters were said to hold only 13.32% of its shares. Generally, the promoters of a company hold almost 50% of the organisation’s shares.

The promoters should have followed the strategy of declaring DVR (Differential Voting Rights) shares.(To know more about Differential Voting Rights Shares, click here). These DVR shares aids promoters to ward off hostile takeovers by issuing shares with fractional voting rights. These type of shares allows the promoters to raise capital without diluting control of the company.

Mindtree’s shareholding pattern did not allow the promoters to exercise their voting powers as they were in minority. L&T approached other investors and bought their shares to complete the hostile takeover against the wants of original promoters. Had there been DVR Shares in place rather than normal common equity shares, Mindtree would have still been operating as a different organisation.

Recent news

Krishnakumar Natarajan is one of the founders of Mindtree. Last week, he and his family have sold over 42 lakh shares of Mindtree. After this sale, their combined shareholding has reduced to only 2.29%. Earlier it stood at nearly 5%. The stake of Krishnakumar is now merely 1.96%. This transaction has been carried out in multiple tranches between April 30 and September 14.

Usually, promoters and founders have a high stake in their company. But since the hostile takeover of the company last year, Mindtree’s major decision takers are continuously leaving the company. Selling of shares by the promoters or the founders of the company usually gives a negative hint to the investors. But on the day that this stake sale was announced publicly, share prices jumped. It happened because the founders of the company exiting means that the new board appointed by L&T can work more easily. See you next time, with another interesting story.

Are you searching about an IPO on google? marketfeed covers that for you! Click here to understand what is an IPO. Here, let’s talk about the Initial Public Offering (IPO) of CAMS.

About the company

Computer Age Management Services (CAMS) is a Mutual Fund Transfer Agency which has been a part of the Indian Financial services segment for over two decades. The company was founded in 1988. NSE Investments Limited, HDFC Bank group, Warburg Pincus LLC and Acsys Investments Private Limited are the owners of Computer Age Management Services.

Today, the CAMS serves as India’s largest registrar and transfer agent of mutual funds. It acts as a technology-enabled service solutions partner (investor interface, dividend processing, brokerage computation, etc.) to Private Equity Funds, Banks, Private Life Insurance, etc. It has 278 customer service centres all over India and has three back-office delivery centres in Chennai. According to CRISIL (Indian rating agency), Based on average assets under management (AAUM), CAMS has an aggregate market share of 70%, which is huge.

IPO Details

CAMS drive a major chunk of its revenue from the mutual fund’s services business. Almost 87% of revenue is contributed by fees they take from Mutual Fund houses. Rest 13% comes from other business. These are non-Mutual-Fund business like verification and maintenance of the KYC records of investors for use by finance institutions. CAMS charges fees based on the size of Asset Under Management (AUM). Higher the AUM, higher the fees. They also follow the policy to charge higher fees on Equity Mutual funds when compared to Debt Funds.

NSE Investments Limited (NSEIL) holds 37.48% stake in CAMS. They are looking to liquidate their stake via an Offer-for-sale.

One market lot consists of 12 shares. For retail investors, the minimum lot is 1 and the maximum lot is 13. That means a retail investor cannot invest more than Rs 1,91,880 (13 Lots X 12 Shares). The tentative date for IPO’s listing date is 1st October 2020.

CAMS’ revenue has increased by aCAGR of 13% from 2016 to 2020. Their Profit after Tax (PAT) has increased by CAGR of 15.2% during the same period. Revenue of the company has seen consistent growth. As the Indian Mutual Funds industry expands in the future, more revenue will be generated by the company.

Over the span of 5 years, companies AUM has increased from Rs 13,50,000 crore to Rs 27,00,000 crore. Return on Equity (ROE) stood at 32.1% for last year. They are able to attain this high ROE for some time now. The average ROE from 2018 to 2020 is 31.4%.

2017-18

2018-19

2019-20

Revenue

650

711

721

PAT

160

130

173

EPS

33

26

35

Revenue and PAT are given in crores

The Pros

CAMS faces very limited competition in the market they operate in. None of their peers are listed. Their closest competitors are Sundaram BNP Paribas and Karvy. Hence, the company is planning to gain even bigger market share in the near future.

The company believes in client stickiness. Their top 10 clients have a healthy relationship of 19 years with the company.

The high potential of the industry and the company to grow in the future makes it a lucrative offer for the investors.

CAMS has 4 out of the top 5 mutual funds and 9 out of the top 15 mutual funds as their clients. Thus, the company has the biggest clients to serve in the mutual funds’ industry.

The Cons

As we stated earlier, around 87% of the company’s revenue comes from their core business, i.e. Mutual Funds. They use more of paper-based MF transactions to generate revenue but slowly the industry is shifting towards digitalization.

CAMS have their valuation on a bit higher side. Their price-to-book value is 34,61 times FY20 EPS.

Do make your own studies before investing in any company. You can find the red herring prospectus submitted by CAMS, here.

India’s retail market is estimated at Rs 60 Lakh Crores in FY 2019-20 and is expected to grow at a CAGR of 10% over the next 5 years to reach Rs 90 Lakh Crores by FY 2024-25. It accounts for around 10% of the country’s GDP. Only around 8-10% of the retail market is organised retail, the remaining 92% fall under unorganised retail.

To protect the interest of agriculturists and small retailers in India, the government has a restricted FDI policy for the retail sector. You can read more about FDI in the retail sector here.

Reliance Retail Ventures Limited (RRVL) is a subsidiary of Reliance Industries Limited. It was founded in 2006. It is one of the largest retailers across India by revenue. Reliance Retail has about 11,748 stores all across India, with 70% of them being consumer electronics stores. Additionally, it owns 328 warehouses or 310 Mn Sq. Ft of warehousing space.

Talking Numbers

Reliance Retail Revenue Contribution By Segment (Source: Company Annual Report)

Reliance Retail’s generates maximum revenue from Connectivity, which essentially is the from the sale of recharge coupons of Reliance Jio (the conglomerate’s telecom arm) and Jio Store. The Consumer Electronics Segment is next accounting for almost 28% of Total Revenue in FY20 followed by Grocery at 21%, Fashion and Lifestyle at 8% and Petro Retail at 8%.

Ever seen those Reliance gas stations? They are actually owned, managed and marketed by Reliance Retail. All of the gas stations fall under the Petro Retail Segment. Reliance Retail owns around 519 of such Petro retail outlets all over the country.

Reliance Industries and its subsidiaries have been in the news a lot lately. This is because they have been on an acquisition and fundraising spree. Over the past decade, Reliance Retail has grown tremendously. The charts given below shows Reliance Retail’s growth over the past 5 years in terms of Profit After Taxes and EBITDA.

EBITDA and Profit After Tax for Retail(FY15-FY20)

During COVID, Store functioning was severely impacted by lockdown and restrictions. Consumer Electronics and Fashion & Lifestyle business remained suspended in April and partially in May/June. Around 50% of stores were fully shut throughout the quarter, 29% were operational partially.

Grocery stores continued operations with limitations and logistical challenges. Operations across the network including supply chain were disrupted by sporadic changes in regulations. Due to the current pandemic situation Reliance Retail did face a revenue drop of 17%.

Performance of Reliance Retail Venture Limited During COVID-19 (Q1FY21) (Amount: Rs. Crore)

Reliance Retail saw a 21% growth across fully operational businesses of Grocery and Connectivity.

Brands and Subsidiaries of Reliance Retail

Reliance Fresh Reliance Smart JioMart Reliance Market Reliance Digital Jio Store Other Partner Brands

Reliance Petro Retail (Reliance Petro Marketing) Outlet.

With refined e-commerce especially in Grocery, JioMart, the newest member of Reliance Retail is expected to rise and it matters a lot to Reliance Retail, but why?

Why does JioMart matter?

Reliance Retail has ventured into the digital commerce space with JioMart in January, 2020. JioMart services were launched across 200 cities on a pilot basis. JioMart also uses WhatsApp ordering feature for consumers through its partnership with Facebook.

JioMart will operate on the Online to Offline business model. This means that it will connect with local retailers and deliver goods to customers by procuring them from the nearest store located in the customer’s vicinity.

This separates JioMart from its competitors like Amazon and Grofers who follow the Warehouse Model, where they stock pile inventories in warehouse spread over various locations.

JioMart will therefore save on fixed costs and other costs associated in maintaining the warehouses. Moreover, it can onboard any retailer in any part of the country into its system.

JioMart order flow is now 4 times more than what it was before the lockdown period.

Future of Reliance Retail

Reliance Industries Limited announced the acquisition of Future Group for Rs 24,713 crore, aiming to boost its presence in the offline retail market. Reliance Retail Ventures Ltd (RRVL), acquired the retail & wholesale businesses along with the logistics & warehousing businesses of the Future Group.

Reliance Retail will have access to around 1800 stores across Future Group’s Big Bazaar, FBB, Easyday, Central, Food hall formats, which are spread in over 420 cities in India.

To Read More about the Future Group Deal, Click Here.

Also, Reliance Retail acquired a majority equity stake in Vitalic Health Pvt. Ltd./ NetMeds for an amount of ~Rs. 620 crores. This marks a presence of Reliance Retail in the Pharma-Retail segment as well.

Reliance Retail acquired 100% stake in Shri Kannan Departmental Store Private Limited (SKDS)for a consideration of Rs 152.5 crores. SKDS is engaged in the business of retailing fruits & vegetables, dairy, staples, home & personal care and general merchandise to consumers. SKDS currently operates 29 stores across Coimbatore and nearby areas.

Reliance Brands Limited, another subsidiary of Reliance Retail acquired 100% equity shares of Hamleys Global Holdings Limited GBP 67.96 million. Reliance Lifestyle Holdings Limited, a subsidiary of the Company, runs and operates the Indian franchise of the Hamleys brand and has 88 stores in India. This acquisition will catapult RBL to be a major player in the global toy retail industry. (Source: Company Press Release)

Reliance Retail has also acquired men’s apparel company John Players in March,2019 for an undisclosed amount.

Investments flowing in

Silver Lake picked up a 1.75% stake in Reliance Retail Ventures for ₹7,500 crore. Earlier this year, Silver Lake invested Rs 10,202 crore in Jio Platforms, RIL’s digital services platform.

KKR & Co. is in advanced talks to invest at least $1 billion in Reliance Retail in what could be another U.S. investment following Silver Lake’s deal. Read More Here.

ADIA is in discussions to invest about $750 million at a valuation of roughly $57 billion, while PIF could funnel as much as $1.5 billion into Reliance Retail. (Source: Financial Times)

There have been reports of Reliance Retail offering 40% stake to Amazon for $20 Billion as well. This news report caused Reliance Industries Limited(RIL) shares to surge 7.2% in the markets.

What sets Reliance Retail apart?

Investment demands are pouring in so hard, that there have been reports of Mr. Mukesh Ambani, Chairman of Reliance Industries Ltd, has had to put investors like Soft Bank and Carlyle Group on a waiting list.

However, what remains common in all the investment rumours is the word “people familiar with the matter”. It is the people familiar with the matter and is anonymous to the public who are making disclosures about these deals. No confirmation has been obtained from the companies what so ever. One should keep their eyes and ears open before making any inferences.

With the Future Group in its pockets, Reliance’s Grocery segment can prove to be a tough competition for other retailers like D-Mart, Grofers, BigBasket and many more.

Additionally, Reliance Retail has its venture JioMart as its blue-eyed boy. JioMart is doing something which other retailers have failed to do so. It wants to include your next-door convenience store into its retail-ecosystem. Geographically too Reliance Retail intends expanding its trail. With the acquisition of Shri Kannan Departmental Stores, it’s set its foot in the state of Tamil Nadu’s niche retail market.

Reliance has managed to extend its wings in multiple retail segments like Toys, Pharma and Fashion & Lifestyle. Reliance has bagged investments and acquisitions for its Jio and Retail platforms, while Oil and Petroleum still continue to be a major source of income, it seems Reliance doesn’t want any sector to remain untouched by it.

On Sept 11, 2020, the Securities and Exchange Board of India(SEBI) released a crucial circular regarding the asset allocation in Multi-Cap mutual funds. Summary of the circular is as follows:

All Multi-Cap funds will allocate at least 75% of the funds to Equity as compared to the earlier 65%.

Out of the amount set for Equities, a minimum of 25% each shall be allotted to Large Cap, Mid Cap and Small Cap each, respectively. The was no such limit set earlier on the allocation within equities in Multi-Cap funds.

All the existing Multi-Cap Funds shall ensure compliance with the above provisions within one month from the date of publishing the next list of stocks by AMFI, i.e January 2021.

AMFI or Association of Mutual Funds in India releases a list every 6 months on which stocks are Large Cap, Mid Cap and Small Cap.

Why did SEBI do so?

Large-cap funds required a minimum 80% in large-cap stocks, Mid-cap fund required minimum 65% in mid-cap stocks, Small-cap fund required minimum 65% in small-cap stocks. There was no such requirement for Multi Cap funds, except that they needed to invest 65% in Equity stocks.

A Multi-Cap fund is one that can invest in all segments by market capitalization i.e. Large Cap, Mid Cap and Small Cap. There was no obligation earlier as to where a Multi Cap fund could invest.

Taking advantage of this, fund manager across India would allocate most of their funds to well-performing large-cap stocks as this would reduce the risk involved and ensure steady returns. They also had the flexibility to invest in well-performing Mid Cap and Small Cap stocks.

This made the funds, lesser “Multi-Cap” in nature and more of large cap in nature causing a skewed allocation of funds.

Name

AUM(Rs. Cr)

Large Cap

Mid Cap

Small-Cap

Kotak Standard Multicap Fund

29,965.94

72%

28%

0%

HDFC Equity

19,381.37

83%

13%

4%

Motilal Oswal Multicap 35 Fund

11,427.26

87%

9%

5%

UTI Equity

11,144.25

64%

31%

5%

Aditya Birla Sun Life Equity

10,884.43

67%

26%

7%

SBI Magnum MultiCap

8,991.12

73%

20%

7%

Franklin India Equity Fund

8,375.15

76%

17%

7%

Average Investment

75%

21%

4%

The table above shows a list of Top 7 Multi-Cap mutual funds sorted by AUM(Asset Under Management). As seen in the table above it is clear that most mutual funds have allotted more than 50% of their funds in Large Cap stocks. This, if not completely, substantially makes the fund, a Large-Cap fund. This is why SEBI set a floor for the amount invested in each segment.

SEBI’s new regulation where it allots 25% per cent each to Large Cap, Mid Cap and Small Cap shall leave the other 25% at the fund manager’s discretion.

New Structure as Proposed By SEBI for Multi Cap Funds

How Will This Impact The Market?

It is clear now that there will be a divestment in Large cap Stocks. There will be an investment spree in Small Cap and Mid Cap stocks as well, but will this affect market rates much? Let us find out.

According to AMFI, the total Asset Under Management for Multi-Cap Funds is Rs 145,907.04 Crores. Out of this Rs 145,907.04 Crores, there will be a divestment of almost Rs 34,000 Crores-Rs 36,000 Crores which is almost 23-25%, in Large Cap stocks.

The amount taken out from Large Cap stocks will be invested in Mid-Cap and Small-Cap stocks.However, this shall happen over a period of 3-4 months and should be a gradual process instead of a sudden one.

The investment in Mid Cap stocks by Multi-Cap funds will increase by ~4%(nearly Rs.5800 Crores). Moreover, investment in Small Cap stocks by Multi-Cap funds will increase by ~21%(nearly Rs. 29000 Crores).

What does it mean for a retail investor or a mutual fund holder?

SEBI released another circular on 13th September which clarified a lot of speculations. In fact, AMFI welcomed the step and fund managers took on to Twitter to calm investors.

All the points listed above might not happen at all. There is a high probability that mutual fund houses might decide to merge their current Multi-Cap Mutual Funds with other Large Cap Funds or Large Cum Multi-Cap. There is also an option given by SEBI to convert these multi-cap funds to large-cap funds or any of their choice. Fund houses can also give you an option to move your funds to a fund of your choice.

The amount of outflow in Large Cap funds is about 4-5% of total AUM of Equity Mutual Funds. So impact on market might be significant but not large in magnitude.

To ensure that there is no haphazard in terms of market stability, this transition shall be a gradual process, which will avoid major fluctuations in mutual funds and stock prices. This will also give a time of 3-4 Months to mutual fund houses to figure out and plan the next course of action so there is no need for panic across the board.

Vodafone-Idea Group has re-branded as ‘Vi’ as it looks for a fresh start. The company announced the move after the Supreme Court gave its verdict on the AGR dues case (Read More Here). In the verdict, the apex court gave Vodafone-Idea Ltd, a period of 10 years to clear its pending dues of Rs 54,754 crore.

Many of us still don’t the amazing journey of the brand where it moved from Max Touch to Orange to Hutch to Vodafone to Vodafone Idea and finally now to Vi. So come let’s learn about this journey, both from the perpectives of Vodafone and of Idea.

What is now Vodafone-Idea Ltd is actually a result of a mixture of Mergers and Acquisitions. From Max Touch to Orange to Hutch to Vodafone Idea to Vi. The Indian economy became an easier playing ground for private sector telecom companies in the early 1990’s. Both today’s Idea and today’s Vodafone were early movers in the field.

The Journey of Vodafone

Vodafone India didn’t just start out as Vodafone. At first, it was Hutchison Max Telecom Ltd (HMTL), a joint venture between Hong Kong based Hutchison Whampoa and India’s Max Group. The company was established in 1992 and commercially called Max Touch.

In the year 2000, the company was rebranded to Orange.

In 2005-06, Max group sold its entire 41% stake to Hutchison, and exited the partnership. Meanwhile Essar Group entered as a strategic partner in the equation.

BPL, another telecom player, was merged with Hutchison Essar in 2004.Furthermore, the company rebranded itself from ‘Orange’ to ‘Hutch’ in 2005, after facing an issue with international copyrights.

Thereafter, it also targeted business users and high-end post-paid customers which helped Hutch to consistently generate a higher Average Revenue Per User (ARPU) than its competitors. By adopting this focused growth plan, it was able to establish leading positions in India’s largest markets providing the resources to expand its footprint nationwide.

Vodafone, which was a leading telecom operator in UK entered the Indian market and acquired the entire 67% stake of Hutchison in February 2007. The company was soon rebranded to Vodafone India. Vodafone later went on to buying out the entire company from other promoters Essar Group and Li Ka Shing Holdings in 2011.

The Journey of Idea

In another side of the story, Aditya Birla Group’s Idea was slowly building up their business as well. Idea Cellular began as Birla Communications Limited in 1995 after GSM licenses were won in Gujarat and Maharashtra circles.

As part of their expansion plans, American telecom giant AT&T was roped in as a strategic partner by Birla in 1996. In 1997, in order to expand into more geographical areas, a tie-up with Tata Communications led by Ratan Tata was also formed. The merged entity was known as Birla AT&T and Tata Communications Ltd, commonly known as BATATA.

The company name was changed to Idea Cellular in 2002 after a series of changes following mergers and joint ventures. In 2004, AT&T exited the partnership to concentrate on their US operations. In 2006, Tata Group exited the partnership as well as they wanted to launch their own telecom brand, which later failed anyway. So after all the partnerships ended, the Birla Group led the company alone until the eventual merger with Vodafone in 2018.

We hope you remember the popular telecom operator Escotel (fun fact : They were the first telecom operator to start operations in Kerala in 1996). Interestingly, Escotel was merged with Idea in 2004 (Another fun fact : Escotel was the disastrous telecom wing of Tractor manufacturer Escorts Ltd).

Four days later after Vodafone entered the country in 2007, Idea Cellular launched its IPO and raised ₹2,125 crores. The IPO was oversubscribed by 57 times. It is interesting to note that the paths of Vodafone and Idea have crossed many times like two soulmates, and ultimately ending up in their merger.

The Merger

The first merger between Vodafone and Idea was approved by The National Company Law Tribunal (NCLT) on 30th August 2018. As per the scheme of the arrangement, Vodafone India and Idea would merge to form a single listed entity.However, both continued to operate two separate brands until September 2020.

Share Holding Pattern of Vodafone Idea Ltd

With Jio entering the Indian telecom sector in 2016, current players in the industry were put in a very tough spot. Mukesh Ambani’s Reliance came into the scene with deep pockets and huge offers. The sudden drop in voice and data tariffs were not tolerable to players like Vodafone and Idea, who were running a highly leveraged business (high debt). Many telecom operators were forced to shut shop, or merge to sustain in the market, including Tata Docomo’s merger with Airtel and the Vodafone-Idea merger.

Hope you all know about the recent AGR case, which has become a huge headache for telecom operators in India. Read more about it here, if you haven’t already. In the recent verdict to the case, The Supreme Court of India has given a period of 10 Years for Vodafone-Idea to pay Rs 54,754 crore, in pending AGR dues.

The Future

On 7th September, Vodafone and Idea rebranded and completely merged into a single brand ‘Vi’. The rebranding was a welcomed move as it came right after the the company’s Annual General Meeting where fundraising prospects were discussed. The share price rose 3% the day the rebranding was announced.

The merged entity is looking to raise Rs 10,000 crore via the sale of its fibre and data centre business, and another Rs 25,000 crore through debt and equity.

The rebranding of Vodafone-Idea along with its fundraising initiative has unlocked many possibilities. Vi is also exploring possibilities of the future 5G spectrum where Jio stands as a tough competition, with its homegrown 5G hardware.

Vodafone-Idea still has long term borrowings worth Rs 1,05,388 crore. It has a cash reserve of Rs 525 crores. Looking at results for Q1FY21, the company can meet its short term obligations, however, it needs to focus on enhancing its cash flow. It cannot afford to finance itself on debt. A cautious investor should watch out for Q2 results, which is likely to tell us how the company has restructured its finances.

Whether or not VI gains traction depends on how it manages to gain back its lost faith by customers and investors. They are currently forced to concentrate on both gaining lost customers and paying their AGR dues. As an investor, one needs to watch out for every single move made by the management of the company. Certainly, the company is too big to fail, with its high levels of debts from leading banks in the country. With the upcoming 5G spectrum sale, the government will want more than just Airtel and Jio to get a healthy bid value. The economy will not be able to handle the fall of this titan.