India’s most valuable listed company with over Rs 14 trillion market capitalisation, Reliance Industries Limited announced the acquisition of Future Group for Rs 24,713 crore, aiming to boost its presence in the offline retail market. Reliance Retail Ventures Ltd (RRVL), a subsidiary of Reliance Industries Ltd, will acquire the retail & wholesale businesses and the logistics & warehousing businesses of the Future Group as going concerns on a slump sale basis which means that the Future group will transfer one or more undertakings to RIL as a result of the sale for a lump sum consideration (Rs 24,713 crore) without values being assigned to the individual assets and liabilities in such sales.

As a part of the acquisition, Future Retail, Future Lifestyle Fashions, Future Consumer, Future Supply Chains and Future Market Networks will merge into Future Enterprises Ltd (FEL). Shareholders of each companies will be allotted a fix number of shares of Future Enterprises Ltd subject to their holdings. Reliance Retail will then acquire Future Enterprises Limited businesses.

What’s in it for Reliance?

India’s retail market is expected to reach $1.3 trillion by 2025, compared to $700 billion in 2019, according to consultancy firm BCG and Retailer’s Association of India. Being the largest retailer in India, Reliance has over 11,000 stores across the country. Majority of Reliance Retail’s revenue is generated from consumer electronic segment which also accounts for nearly three-fourths of its overall store count. To compete with the global competitors like Amazon and Walmart, Reliance needed to boost its grocery and fashion & lifestyle segment in its retail arm which currently accounts for only 7% and 20% of the store count respectively.

Kishore Biyani who is known as “Father of India’s organised Retail”, understood the Indian market very well and brought the middle-class Indian consumer in his stores and retained the consumers. Big Bazaar and Easyday of Future Group made grocery shopping an event for the Indian consumers where they trusted the stores as they used to do with local kirana shops. Also, pricing was an important factor which Kishore Biyani realised was important to cater for attracting the consumers. He built the customer base over the last three decades and for Reliance it will be crucial to grow in this segment.

So, the answer to the acquisition of Future Group’s businesses is the Grocery and Fashion & Lifestyle segment. Reliance Retail will have access to around 1800 stores across Future Group’s Big Bazaar, FBB, Easyday, Central, Food hall formats, which are spread in over 420 cities in India.

Future Group after the acquisition:

Post the transaction, Future Enterprises Limited will retain the manufacturing & distribution of consumer products, fashion sourcing & manufacturing, insurance joint venture with Generalli and Textile partnership with NTC Mills. For Kishore Biyani, as a result of the agreement, he cannot enter the retail business for at least 15 years since the commencement of the deal.

Reliance Retail and Fashion Lifestyle Limited (RRFLL) also proposes to invest in Future Group post the acquisition at total sum of Rs 2800 crore in two ways,

Rs 1,200 crore in the preferential issue of equity shares of FEL to acquire 6.09 percent of post-merger equity.

Rs 400 crore in a preferential issue of equity warrants which, upon conversion and payment of balance 75 percent i.e. Rs 1200 crore, will result in RRFLL acquiring additional 7.05% stake.

Other Deals in Reliance Retail

To gain a significant market share in every segment it caters to, it has been expanding its fleet through acquisitions and new launches. In 2019, Reliance Brands acquired the British toy retailer Hamleys and Reliance Retail has the master franchise for the brand and operates across 29 cities. Also, the company launched JioMart – an online grocery service which will offer free express delivery of groceries from neighbouring local stores.

Recently, Reliance Retail announced an investment from Silver Lake worth $1.02 billion. It will grant Silver Lake a 1.75% stake in the entity and the deal values Reliance Retail at $57 billion.

Conclusion

With the recent acquisitions, Reliance Retail aims to widen the spread between the India’s largest retailer and the second largest retailer (Avenue Supermarts Limited). The Future Group’s retail and logistics will definitely give Reliance Retail an edge in grocery and fashion lifestyle segment. Amazon and Flipkart pose a threat to Retail with the online delivery of these products but in response to that, RIL has launched its JioMart. Thus, the future definitely looks promising for Reliance Retail.

ITC Ltd. or Indian Tobacco Company established as Imperial Tobacco Company was established in Calcutta in 1910. It began as a Tobacco Conglomerate, later on expanding to a variety of areas such as Luxury Hotels, Paperboards, Agri-Business and FMCG sectors. ITC is a blue-chip stock and for long been known as a safe investment that gives a high dividend. In case you are planning to invest in ITC, here are __ things you need to know.

Company Profile

ITC’s Revenue Channels. Pre-COVID

ITC is India’s leading tobacco company. It has a near-monopoly when it comes to cigarettes. ITC manufactures more than 84% of India’s cigarettes and controls 75% of India’s entire tobacco industry.

In the late 70s, ITC ventured out into the world of luxury hotels and hospitality. It currently operates more than 100 hotel chains. ITC has been expanding on its FMCG sector having faced a massive growth in revenue from it in the past 10 years. Its Agri-business has gained a fair amount of traction last year with a 9% revenue growth (YoY) between Q1FY20 and Q1FY21 in its Agri-Business segment.

ITC’s inter-segment revenue stood at Rs. 5907 Crores facing a revenue growth of 20% as compared to the same quarter last year. This portrays the efficiency of ITC on being able to manufacture its own raw material and the fair dependability of companies on each other. Over the last 10 years, Total Shareholder Return has grown at a CAGR of 11%, significantly outperforming Sensex (CAGR: 6.9%)

Efficiency

ITC as a company is a virtually debt-free company. Cash generated by ITC is significant for it to fund its own new ventures.

ITC’s ROCE(Return on Capital Employed) stood at 72%. This means for every Rs. 100 worth of Capital Employed ITC earns Rs. 72 on it.

In the past 5 years, ITC’s Basic EPS has seen a growth of 9.1% CAGR. Basic EPS is the net-income generated by the company per outstanding share. Its Cash EPS or cash flow generated per share stood at Rs 13.59/share. Its Cash EPS grew at 9.7% CAGR over 5 years. CAGR stands for Compounded Annual Growth Rate.

Ex-Company Chairman (Late) Y C Deveshwar had set the target of making ITC the biggest player in the FMCG segment by year 2030 targeting revenue of Rs. 100,000 crore from the FMCG business.

Net Cash Flow ITC (Source: Neha Rawat, SCAC)

ITC’s Profitability ratios are better than Godfrey Philips and HUL this means that ITC as compared to industry peers, is financially sounder and is in a better financial position to commit to growth and expansion.

The company’s dividend payout ratio as of March 20′ was 42% which is expected to pump up once the dividend is announced in the future. Dividend Payout Ratio of 42% means the company is giving out 42% of its net profit as dividend.

Coming to the shareholding of the company, the company has 0 promoter holding. Often times in corporates, the management makes decisions that support the interest of promoters or major stakeholder. In ITC, majority stake lies in the hands of public shareholders, the company is likely to make decisions in the public interest.

Tobacco and Diversification.

Cigarette has an inelastic demand. This means that compulsive smokers won’t stop smoking even if the price of cigarettes rise. When the government increases the duty, the cost of it get passed down to the consumer

The COVID-19 pandemic has reduced the contribution of cigarettes in the revenue of the company. It faces a temporary ban for sale and/or public smoking in few states as well. Before the pandemic as well, ITC had been reducing its focus on Cigarettes and Tobacco Products. This has many reasons behind it. According to an ITC report:

India is the 4th largest market for illegal cigarettes in the World; causing a revenue loss of over 15,000 crores every year.

42% of adult Indian males consume tobacco. Only 7% of adult Indian males smoke cigarettes as compared to 14% who smoke bidis and 30% who use smokeless tobacco.

Since 2010/11, legal cigarette industry volumes have declined by about 20% while the illicit duty-evaded cigarette segment has grown by 36%.

Contribution to Tax of Tobacco is Disproportionate to Legal Sales

The above reasons have led ITC to diversify into other sectors like FMCG and Agri-Business. For ITC, Cigarette Business’ share in the revenue of ITC has reduced over the years and increased in other sectors.

ITC has started pumping into FMCG segment like never before. The graphical representation below shows the expansion of ITC into FMCG products over the past decade.

Gross Revenue Reported over the decade. (Amount: Rs. Crores)

Supply and Distribution Chain.

ITC has the most unparalleled supply and distribution chain in the country. The reason why it has managed to capture 75% of the tobacco market is its supply and distribution chain. ITC has managed to access the remotest areas in the country. To know more about ITC’s supply chain. Click Here

E-Choupal is a business initiative by ITC Limited that provides Internet access to rural farmers. The purpose is to inform and empower them and, as a result, to improve the quality of agricultural goods and the quality of life for farmers. ‘e-Choupal’ services today reach out to over 4 million farmers growing a range of crops – soybean, coffee, wheat, rice, pulses, shrimp – in over 35000 villages through 6100 kiosks across 10 states (Madhya Pradesh, Haryana, Uttarakhand, Uttar Pradesh, Rajasthan, Karnataka, Kerala, Maharashtra, Andhra Pradesh and Tamil Nadu). To Read More about E-Choupal, Click Here.

The Future

ITC has started to shift its dependency from cigarettes to other areas. It suffered a huge reduction in cigarette sales by almost 33%. ITC has realised that its dependency on cigarettes won’t be viable in the long term. During COVID-19, the only two sectors showing positive growth were FMCG and Agri-Business.

ITC is diversified in FMCG and foods segment, with a wide variety of products to offer the company has recently crossed 10,000 crore revenue mark and targets 100,000 crore revenue from FMCG by 2030. A good financial history and a stable distribution setup make it a good company to invest in the long term. However, it is necessary that one performs their own research before investing.

Many borrowers like you and me are facing deep economic stress due to the pandemic. Some of the people have lost their jobs and some are working with significant pay cuts. This has caused people to default on their loan repayments. RBI has to come to their aid since the start of the pandemic by issuing out a loan moratorium from March 2020.

This moratorium period ended on 31st August 2020. Till then, borrowers were allowed to defer from their repayments. Now RBI has advised the banks to restructure the loans of stressed assets so that the banks do not have to count them into NPAs. But the central bank is still very sceptical about this step.

What is Loan Moratorium?

When a borrower takes a loan, he is obligated to pay his monthly instalments to the banks. Loan Moratorium is a period during which the borrower is relieved from the obligation to pay fixed instalments. Once the loan moratorium period is over, he is again bound to pay the fixed instalments at fixed regular intervals.

Restructuring of loans

RBI has allowed banks to restructure loans of borrowers who are struggling to repay because of the pandemic. The last date for banks to restructure the loans is December 31, 2020.But what does this restructuring of loans means? The borrowers have to make a fixed payment against the loans issued to them. The restructuring of loans’ plans will help them on a few of these criteria:

Reschedule their loan payment

Lower interest rates on their existing loans

A limited loan repayment holiday

Possible loan moratorium to a maximum of 6 months

All banks and non-banks including small finance banks, Local Area Banks, NBFCs, housing finance companies and all the other Indian financial institutions can help their borrowers by restructuring their loans.

The eligibility criteria

Those borrowers who were making repayments for their loan in less than the 30 days after the repayment deadline as of 1st March 2020 are eligible for the benefit. Financial services providers and MSME borrowers who have total loans outstanding of less than Rs 25 crore are not eligible.

For corporate borrowers, banks have to come out with a restructuring plan before the start of 2021. They will have a 6-month time period, till June 30, 2021, to implement it. When it comes to personal loans, the banks have the same duration to invoke a new plan but will have only 90 days to implement it. If the banks fail to implement the resolution plan in the specified duration then no restructuring will be approved and the banks will be forced to set aside higher provisions.

Impact on Banks

Banks are the central figure of this resolution plan. The restructuring plan will help in keeping things static but what implications will it have on medium and long-term in still to be seen. With this in mind, RBI has asked banks to maintain additional 10% provisions against post-resolution debt.

As loan moratorium is not extended for the first time since March, banks will get a better picture of how much their NPAs has risen. With this new move, banks do not have to count every default as an NPA. Thus, saving themselves from a lower bottom line in their Profit and Loss statement. During the revival window, if the borrower can get his business running, he will be paying the loan accrued back. Hence, benefitting all parties.

Is everyone better off?

Restructuring of loan is a win-win situation for both banks and the borrowers but not so much for the economy as a whole. By not naming defaulters, banks do not have to keep higher provisions. When the banks are forced to keep high provisions due to NPAs, their losses mounts. This loss leads to negative emotions among the investors in the stock market which further drives down the bank’s market value. As borrowers are not termed as defaulters, their credit score is not impacted and they can avail loan from other banks. For the general public, their deposits are at risk as banks are giving out its depositor’s money to people who may not pay under the it back under the name of moratorium.

In 1987, Infrastructure Leasing & Financial Services (IL&FS) was incorporated as an initiative to form “RBI registered Core Investment Company”. It is a non-banking finance company (NBFC) which was initially promoted by Central Bank of India, HDFC and Unit Trust of India (UTI). Over the past 30 years, IL&FS has aided in developing some major infra projects around the nation.

Few projects to name are Gujarat International Finance Tech-City (GIFT), Delhi-Noida Toll Bridge, Tripura Power Project and Chennai-Nashri tunnel (India’s longest road tunnel). Currently, Life Insurance Corporation of India, ORIX Corporation and Abu Dhabi Investment Authority (AIDA) are the largest shareholders for the company.

What is the crisis?

IL&FS ran out of cash due to a severe liquidity crunch. This resulted in the company to default on a few payments. They also failed to service its commercial papers (CP). The first hint of downfall in the public domain came in March 2018 when the company postponed a $350 million bonds issuance. During the same month, their consolidated total debt stood at whopping Rs 91,091 crore. IL&FS defaulted on inter-corporate deposits and commercial papers of about Rs 450 crore.

Later that year, IL&FS Financial Services cleared their dues related to Commercial Paper on 31st August, three days after the due date. IL&FS and it’s Financial Services subsidiary had a combined Rs 270 billion of debt rated as junk by CARE Ratings. Soon are the defaults came into the knowledge of the public, rating agency ICRA downgraded their borrowing ratings which came as a huge dent on the lendor’s business image.

The Asset-Liability Mismatch

This was one of the biggest reasons why IL&FS hit rock bottom. The company was borrowing loans in the form of commercial papers. You would be thinking, what are Commercial Papers? CPs are short-term unsecured debt-market instruments. These debt instruments have a maturity period varying from 7 days to one year.

The company was taking short-term debt and using it for financing long-term projects which would give returns only after 5-10 years. With the company’s rapidly depleting cash, they were unable to meet the demand and defaulted on several of its obligations. IL&FS’ leverage ratio jumped from 10.6x in September 2017 to 16.8x as of March 2018. That means, 6.2x jump inside a mere 6 months!

PPP Model Inefficiency and LARR

The Government of India introduced the Public-private partnership (PPP) model to aid companies for better efficiency and thus better output. With the launch of this model, the company was assured that the government will help them in financing big projects. With this assumption, they invested heavily in infrastructure projects. The company started acquiring lands on a very big scale, took numerous infrastructure projects and financed them.

But the government did not cooperate with the company to the level they expected and launched LARR (land acquisition rehabilitation and resettlement act) in 2013 instead. When LARR was passed, landowners claimed their compensation for the lands which were theirs. With the rules of LARR and no help from the government in this regard, IL&FS has to pay Rs 17 crore plus worth of compensation to the landowners. This resulted in the overshooting of the cost of the projects and future defaults. This gave birth to the huge difference between the estimated cost of the project and the executed cost.

Other Reasons

IL&FS was incorporated as a finance company. Their purview of work was to fund the infra projects. But from 2015 onwards, they started taking ownership of several risky projects. To meet this, they took short-term loans and diverted the funds for long-term applications. This was done to take loans at a cheaper rate as short-term loans incur less rate of interest when compared to long-term loans.

The company was incurring losses and having very poor cash stability from the past 5 years. Yet the remunerations to the top management was not reduced.

IL&FS operates in a very risky business. No return could be derived from the infra projects until it is successfully completed. Yet, the top risk management team did not hold any meeting for over two years.

Going Forward

More than 30 funds across all categories, such as liquid funds, short-term funds, etc. had IL&FS in their portfolio. Inside two weeks short-term scrips of IL&FS were downrated ‘D’ from ‘A4’. This severely affected the fund houses and forced to mark down the value of the schemes. This led to a steep fall in the NAV (Net Asset Value) of these funds. Recently, Franklin Templeton announced the shut down of its six Debt Mutual Funds with Rs.26000 Crore Asset Under Management. IL&FS crisis played a huge role in the liquidity crunch here as well.

IL&FS defaulting was a very big blow for the Indian economy. Even after two years, the country is still feeling the effects of its downfall. The government should aim to make strict laws to be made so that transparency is restored. The auditors also did a terrible job as they failed to detect the fraud numbers behind the company’s financial. They even failed to flag some of the blatant errors. As big the IL&FS mess is, everything cannot be explained in one article. Marketfeed will come up with more pieces on this topic so that the readers can understand the aftermaths of IL&FS blowout in detail. Until next time.

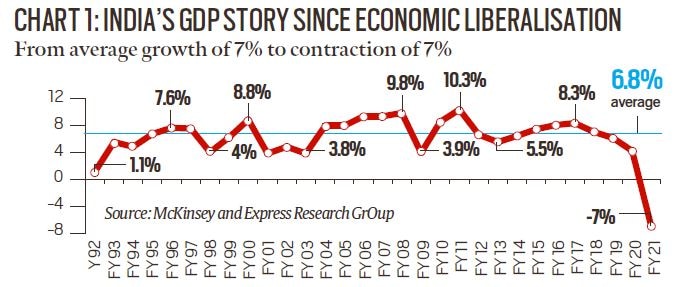

The National Statistical Office of India’s GDP(Gross Domestic Product) estimates and National Accounts for the period of April-June were published on 31st August 2020. Gross domestic product (GDP) is the money value of all finished goods and services made within a country during a specific period. Observers of the Indian economy keenly awaited the NSO GDP data because it would provide the first benchmark of the state of the Indian economy after the Covid-19 pandemic disrupted it and forced the country into widespread and repeated lockdowns. The highlights of the result were as follows:

India’s Real GDP (GDP adjusted for yearly rise in prices) contracted by 23.9% as compared to Q1 2019-20. It contracted from ₹35.35 lakh crore to ₹26.90 lakh crore. Real GVA or Value of Goods and Services Produced in the economy)contracted by 22.8%.

Production of Coal reduced by 15%, and that of Crude Oil by 6.5%. The production of crude oil didn’t fall much since India imports crude oil from other countries. The production of cement reduced by 56.8%

Indicators of Production of Key Goods.

Industrial production (IIP) took a huge hit. The Metallic Minerals industry contracted by 43.3% followed by Manufacturing Industry at (-)40.7%. This was evident looking at the slumped metal consumption this quarter. Read More about India’s metal sector Here.

Index of Industrial Production(%)

The only industry in India with positive growth was Agriculture, Forestry and Fishing which was up by 3.4%. To read why the agriculture and other rural industries prospered during the lockdown, Click Here.

The Hospitality ( -50.3%) and Construction (-47%) industries were the most affected.

Gross Value Added By Different Industries.

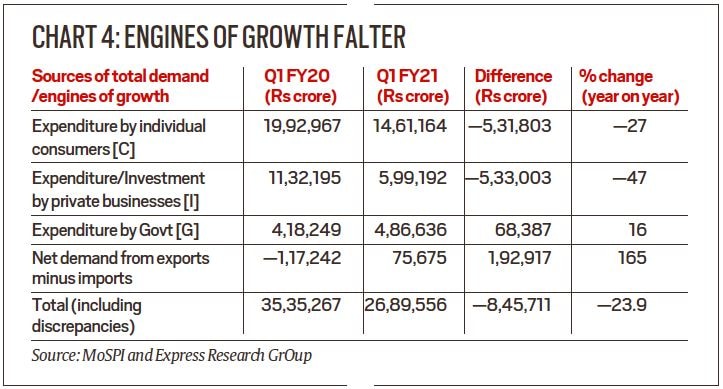

Components of GDP

GDP(Y)= C + I + G + NX

The formula of GDP is as given above. Where:

C = Consumption. Money spent by people or private expenses.

I = Investment. The investment made by private players into local entities and businesses.

G = Government. Government. Government expenditure or transfer payments such as education, healthcare, social protection.

NX = Net Export (Export Minus Import)

Lets understand how each of the four engines of GDP worked out this Quarter.

The private consumption expenditure (C) fell 27%. Additionally, investments into businesses(I) also slumped by 47%. Government Expenditure increased by 16%. This is due to the Aid which the government had provided in the wake of the COVID-19 Pandemic.

The net exports increased by 165%, but is this a good thing? Generally, India’s imports are always more than its exports. Now, imports have fallen because India’s total demand has fallen as well, which is not good.

Conclusion

India’s contraction of GDP was unexpected. The GDP Growth estimate by World Bank was (-)4.5%.

According to the Centre for Monitoring Indian Economy (CMIE), salaried jobs suffered the biggest hit during the lockdown, with a total loss estimated stands at 18.9 million during the first quarter. Meanwhile, recovery in the second quarter has also not picked up as expected with various states announcing lockdowns due to rise in coronavirus cases in July and August.

When private consumption(C) falls sharply, businesses stop investing. Since both of these are voluntary decisions, there is no way to absolutely force people or businesses to spend more or indulge in expansionary economic activity. Lower interests in your Fixed Deposits and saving account is one way to try and make people spend money. Also, loans given out by banks have all-time low interests now to incentivise businesses to expand.

India is increasing Government Expenditure(G) with multiple PSUs announcing huge expansion projects. The second way out is Monetary policy. RBI has been involved recently in important Open Market Operations and Long Term Repo Operations(LTRO). Read more about it over here. Hopefully, these measures taken by the government will see quick reactions from the economy.

The 41st GST Council meet chaired by Finance Minister Nirmala Sitharaman was conducted on August 27, 2020. Finance ministers of all the states were a part of this meeting. The meeting comes at a time when there is rising tensions in states regarding revenue shortfall.

As manufacturing and services have taken a major hit during this pandemic, taxing revenue in turn was affected for the states as well as central government. Amid these crucial times, several state governments and citizens expected the meeting to discuss various issues like compensation to states and GST rates revision; revenue shortfall; need of tax rate cut in two-wheeler industry and centre providing a relief to states in FRBM (Fiscal Responsibility and Budget Management) Act.

The meeting focused on the issue related to state compensation and GST rate cut will be reviewed in later phase.

The key outcomes of the meeting are as follows,

Major concern regarding compensation cess, which is the compensation paid to the states by the centre for the possible revenue losses due to the consumption-based nature of the GST was addressed. The centre estimated the Annual GST compensation requirement to be around Rs 3 lakh crore and the cess collection is expected to be Rs 65,000 crore, which means that the total shortfall in the GST collection is at Rs 2.35 Lakh crore.

Out of the total shortfall, Rs 97000 crore is on account of GST shortfall, while the rest is due to COVID-19 pandemic. To compensate the states on account of revenue shortfall, the council proposed two options to the state –

Borrowing Rs 97000 crore which is significantly less amount and keeping the cess entitlement intact i.e. getting cess later till the decided period.

Borrowing the entire Rs 2.35 Lakh crore shortfall and pay for it using the cess collected in transition period.

Important point here to note is that the centre assured that it will facilitate the talking with RBI. It will help getting G-security linked interest rates so that each state does not have to struggle for loans. However, the loan will be taken in the names of states and the rates will be same for all the states.

For the states opting for option 1 i.e. Borrowing less and keeping their cess entitlement, they will be given an additional relaxation of 0.5% in FRBM for market borrowing. It means that they can keep their fiscal deficit up to 4% of their GDP.

Not considering any rise in interest rates to make up for shortfall will be welcomed by the state but proposing to move to a market borrowing mechanism would extend the tenure of the cess beyond five years after July 2022. This will be a concern for businesses as well as consumers as they would be required to pay compensation cess.

It was assured by the Finance Minister that two-wheeler GST rate cut has merit and surely needs to be reviewed

A brief GST council meet may be held again as States have requested to lay down both the options and provide a window of 7 working days to deliberate on it and get back with a decision.

Conclusion

In case of both the options, the interest payments will start once the transition period for compensation cess ends. It will be paid from compensation cess which the states are liable to receive. Taking a higher amount, which is opting for second option, the states, for a long period of time will lose out on the revenue which compensates for the losses. GST revenue accounts for around 42% of taxing revenue for state. So, opting for option 1 would provide enough fund to sustain the revenue shortfall. If a state requires additional fund, they can go for market borrowing up to the amount required.

As the council is planning to extend the transition period for compensation cess payment to the state, it would not be beneficial to the public. Citizens will have to pay GST cess even after a pre decided transition period. It means that the citizens and businesses will be affected on account of this move. Certain items classified by the government will remain in the higher tax bracket.

The Reserve Bank of India has been in news lately for the implementation of the Operation Twist and/or LTRO(Long Term Repo Operations) in order to boost and infuse liquidity into the economy. The RBI did this so to recover from the economic downturn caused by COVID pandemic. However, they have been doing something similar since November 2019, when COVID was not even around. The liquidity crunch made RBI undertake multiple Open Market Operations(OMO) and Repo rate cuts. Let’s find out the story behind this.

Where It All Started…

The story goes back to when the IL&FS fraud and credit default which shook the country’s vigilance and credit system. The rising number of loan defaults caused the banks to restrict the supply of cash into the economy, that is, the banks became more cautious and vigilant while giving out credit. When the supply of money stopped in the economy so did economic progress. This caused RBI to undertake multiple repo rate cuts and Open Market Operations. To find out more about how repo rate works, click here.

Essentially, before implementing LTRO, the Reserve Bank implemented two liquidity tools namely LAF(Liquidity Adjustment Facility) and MSF(Marginal Standing Facility). So what do these terms mean exactly?

LAF or Liquidity Adjustment Facility is a monetary policy tool used to induce liquidity in the market wherein the RBI lends money to all banks(Private and Otherwise) at the repo rate for a short period( Overnight upto 7 days) depending on the situation in exchange for government securities or bonds.

MSF or Marginal Standing Facility is the rate at which scheduled banks can borrow funds from Reserve Bank of India (RBI) overnight at repo rate + 3%(300 basis points).

However, neither MSF nor LAF did any good. The RBI’s intention was to put money into the system, and the money did reach the banks. However, it failed to reach the market. People refused to borrow money. The rate cuts only reduced the interest received on bonds, whereas the banks couldn’t reduce their interest rates. This failed to drive up investments. The problems of LAF and MSF were:

Lack of Policy Transmission. Even though RBI had rate cuts, this didn’t reflect in the banking system which failed to deploy the funds into the market.

Credit Flow was inadequate, the market’s borrowing didn’t increase substantially.

Liquidity Issues.

Coming to LTRO or Long Term Repo Operations

After the LAF and MSF failed to boost the economy. The RBI decided to come up with LTRO or Long Term Repo Operations and the Operation Twist.

Fun Fact: Operation “Twist” was implemented for the first time in the USA by the Kennedy Administration in the mid-1960s. It was named after a dance form which was a craze back in the day.

LTRO is a tool that lets banks borrow funds for one to three years from the central bank at a fixed repo rate, by providing government securities with similar or higher tenure as collateral. Essentially, instead of a repo operation for a short term, RBI is lending money to the banks for a longer-term (greater than 1 year).

The government implemented the LTRO in three stages:

LTRO. Notified on Feb 07. Read Here.

TLTRO I (Targeted Long Term Repo Operation).

TLTRO II.

In the first LTRO, RBI had deployed ₹50,000 crores worth of funds. By 18th March, RBI had lent out₹1.5 Lakh crores worth of funds banks for a period of one to three years. To RBI’s dismay, the COVID-19 pandemic forced the entire nation to go under a lockdown. This meant banks had no reason to deploy funds. Banks held on the funds instead of deploying them.

RBI couldn’t get the banks to deploy funds in the market even through LTRO

The RBI had to figure out a way to ensure that the banks deployed the funds in the market instead of holding on to them. Therefore, RBI came up with Targeted LTRO (TLTRO).

Under TLTROs the banks had to invest the amount received in TLTROs in primary and secondary markets. This involved corporate bonds, commercial paper, debentures, NBFCS, MFIs and other securities. Thereafter, In TLTRO 2.0 banks had to :

Invest at least 50% of the total funds in bonds issued by small NBFCs of asset size of Rs 500 crore and below

Invest in Mid-sized NBFCs of asset size between Rs 500 crore and Rs 5,000 crore

Invest in MFIs or Micro Finance Institution

However, TLRTO was a no show with very few bidders participating in it. Essentially, it wasn’t a success as well.

Operation Twist

There were certain pre-conditions set by banks to avail TLTROs by banks. It involved banks requiring to invest a certain amount of borrowed amount in the primary and secondary markets. On 25th August 2020, the RBI announced that it was going to conduct the second stage of Operation Twist to induce liquidity into the market.

Let’s understand a few terms before understanding Operation Twist.

Operation Twist– Operation Twist is an Open Market Operation(OMO) by the central bank where it sells short term bonds and buys more long term bonds. These are mostly government securities(G-Sec)

Long Term Bonds– These bonds are redeemable in the far future or are far from maturity.

Short Term Bonds– These bonds are redeemable in the near future or closer to maturity.

Liquidity– Money supply for an individual or a group of individuals or the market.

Yield – A bond yield is the return an investor realizes on a bond.

What goes on in Operation Twist

In Operation Twist, the central bank sells short term bonds. The proceeds received from selling short term bonds are used to buy more of long term bonds.

Operation Twist

What this does is that it creates a shortage of long term bonds, which in turn increases its price. This brings down its yield or interest rate. Likewise, the opposite holds true for short term bonds.

Note: Price and Yield of a bond are inversely proportional.

When the RBI sells the short term bonds, the supply of it increases, which in turn decreases the price of the bond, which in turn increases yield, which then drives up short term interest rates.

When the short term bonds mature and its payout time, the ones who own the bonds will get a higher payout than usual. This increases the ‘supply of money‘ in the system. Which brings down overall interest rates. The lower interest rates encourage the market to borrow more and invest in market activity. This way the economy starts to prosper.

Summing it up

The Operation Twist in recent times was first adopted post the 2008 economic crisis to lift the country out of recession. The RBI had been trying its best to revive the Indian money market after the IL&FS fraud and default case. It had tried various different monetary policy tools, LAFs, MSFs, OMOs and LTROs all to its dismay. This move has been praised by many as a masterstroke. Well, many such operations were in the past. Whether or not the Operation Twist turns out to be a masterstroke, only time can tell.

Life insurance is an agreement between the insuree (customer) and the insurer (insurance company). According to this contract, the insured person has to pay regular premiums to the insurance company. In return, the family of the insured person will receive a lump-sum amount in the event of the insured person’s death. New types of life insurance also provide you with periodic returns and a maturity benefit amount if the insured person remains alive until the expiry of the policy.

The Indian Life Insurance industry is dominated by the publicly-owned Life Insurance Corporation (LIC). It has a market share of 69.25%. The rest of 30.75% of the market is shared between 24 private life insurers. In the private sector, SBI Life and HDFC Standard are the two biggest players with a market share of 7.68% and 6.56% respectively. Till 1993, private players were not allowed in the industry but reforms in other sector provoked the government to bring reforms in this industry as well.

COVID-19 has impacted almost all the industries, mostly negatively. What about the life insurance industry? Let’s have a look.

The Impact on Investment mentality

COVID-19 has changed the way customers behave. Life Insurance demands that people need to invest more in the initial years. They have to wait for several years to get their benefits. The modern type of insurance helps you in gaining returns from year one. But those returns are way less than the premium which has to be paid by the customer for a first few years.

All in all, life insurance helps you to decrease your risk of income in future but for that one has to pay now. Currently, people want to reduce their risk exposure but are not ready to pay now for that. If the insured person has to invest right now, and that too, without getting any benefits, why would he do that in the middle of the pandemic when he has unstable cash inflow?

Many people have faced wage cuts, job losses and business failures. This has substantially decreased their income, though their expenses are still similar to pre-COVID times. Many of them have to use their savings to run their households. So, when you have a reduction in the inflow of money with similar outflow, one would think twice before investing his/her money at a place where he/she has to wait for years to get benefits. This is a case when we say that people are looking to fulfil their short-term needs and are avoiding to make any long-term plans for which they have to incur the cost right now.

Numbers confirming the fall

New business premiums decreased by 32.6% in April of this year. Only Rs 6,728 crore was collected in April 2020 when compared to Rs 9,928 crore in April 2019. It is reported that the sector has faced a 12% fall in first-year premiums. First-year premiums were amassed to be Rs 72,321.5 crore from April to July 2020. This was Rs 82,146.5 in the same period last year. The overall sum assured also faced a steep reduction of 9.2% between April and July this year.

The state-owned LIC witnessed its new business premium dipped to 2/3rd in April 2020 of what was in the previous year. Life Insurance Corporation recorded Rs. 3,582 crore of new business premiums in April. This number was Rs 5,639 crore one year ago.

Among private insurers, HDFC Life insurance and ICICI Prudential Life Insurance saw a big fall in their new business premiums. The former recorded a decline of 53% whereas the latter recorded a decline of 60%.

Headache for the insurers?

Unfortunately, COVID has taken a lot of lives. With no vaccine out in the market, more people will succumb to this disease. Many of them will be insured as well. Thus, whenever their family files for mortality claims, these life insurance companies are liable to pay them. As the claims have increased, insurance companies’ outflow has also increased. This has added more pressure on these companies financially.

Claim settlement ratio is one of the most important metrics to judge any insurance company. It refers to the percentage of claims the company has paid out relative to the claims which were filed inside one year. A life insurance seeker is always advised to look at this percentage before choosing the life insurance entity.

If the insurance companies do not pay the claims which have been filed recently due to COVID, this ratio will face a fall which will give a negative outlook to the potential customers. Thus, companies will lose more business next year.

Positive output in the long-term?

Not many Indian are aware of life insurance benefits. A very few numbers of people might be knowing that paying insurance premiums also helps you in making tax savings. The people who have awareness about life insurance, don’t want to invest now and wait for benefits which will be received only after a few years. All this leads to a very less number of people insured in our country. According to the data, India has a life insurance penetration of mere 3.69%.

With Covid-19 pandemic, the awareness and the need for insurance have risen sharply. People are realising that they could have been better off if they have invested their money. This global crisis will make them understand that it is very important to have a safety cover because one cannot predict what can happen in future. Thus, the industry can hope for a revival once the people starting having a stable cash position. The insurance company leaders have a dual fight in front of them. Firstly, to manage their operations in these disrupted times and secondly, making new policies which can attract people after the spread of virus decreases.

Tea and Coffee are two of the most common beverages in the world. They have been regarded as a holy potion. It is has a high medicinal value. In fact, Chinese immigrants to the USA who helped build the First Transcontinental Railroad in the 19th Century survived on Black Tea, which helped stave off dysentery and other waterborne illnesses. Out-of-home consumption itself is 40% of the total consumption of tea.

The cultivation of Coffee started with the sowing of 7 Coffee beans smuggled from Yemen by an Indian Saint. Thereafter, the seeds were sown in the present-day district of Chikkamagaluru. It is estimated that India now consumes 120,000 tons of coffee per year.

Tea and Coffee Key Data.

Annual Tea and Coffee Statistics(FY-19)

The market consumption for Tea is expected to grow at a CAGR of 4% in the forecast period of 2020-2025. It is expected to attain 1.40 million tons of production by 2025.

As of 2019, India was the second-largest tea producer in the world with production of 1,339.70 million kgs. Furthermore, during Jan-Feb 2020, the estimated production of tea stood at 30.54 million kgs.

Revenue in the Coffee segment amounts to US$808m in 2020 in India. The market is expected to grow annually by 8.9% (CAGR 2020-2025).

India’s % Export Country WIse

According to CoffeeBi, The urban consumption dominates with about 73 per cent of total volumes. The remaining 27 per cent it is speculated to account for rural consumption, especially in South India. Moreover, Coffee is consumed more in South India than in North India.

Among the South Indian States, Tamil Nadu accounts for 60 per cent of consumption, while Karnataka, Andhra Pradesh, and Kerala account for 25%, 10%, and 5% respectively.

Nearly 30% of Coffee produced in India is Arabica and 70% produced is Robusta.

Tea, Coffee and the Tickers; and of course COVID-19.

Tea and Coffee stocks have shown excellent performance this quarter. According to Trendlyne, 10 out of the 12 Tea and Coffee stocks have shown a positive profit growth this quarter and share prices of Tea and Coffee stocks zoomed substantially. However, Production and Consumption figures speak the opposite, What is the paradox we are looking at? Let’s find out.

Tea

After the COVID-19 pandemic, there was a 40% reduction in production in Tea due to disrupted supply chain and loss of lively hood. Moreover, Assam, which is the highest producer of tea faced devastating floods. The production of the state fell from 44 Million Kilograms (M. Kgs) on April 19′ to just about 14 M.Kgs on April 20′.

The price of tea skyrocketed from a meagre Rs. 121.34 per Kg in March to Rs. 188.77 per Kg in July, according to Auction Price Data from Tea Board. The average monthly domestic consumption is 90 million kg. Of this, out-of-home consumption accounts for 36 million kg. In April and May, there was a loss of around 72 million kg of tea consumption.

As tea prices soar in India due to lower output this year, tea players and tea traders are considering importing teas from Kenya and Vietnam, where tea prices have crashed due to overproduction.

If the government approves, India may have to import tea for the first time. India has been importing teas only for re-export and that too at a small volume of 9-10 million kg annually.

Coffee

India’s coffee exporters are amidst deep financial crisis with the state and Central governments announcing a lockdown to contain the spread of Covid-19 across the country. Restriction of coffee exports from India to Europe has had an unprecedented impact on the Indian Coffee Industry.

As a result, around 21,000 metric tonnes of coffee valued at over Rs 400 crore is stuck at coffee curing centres and various ports for non-availability of permissions to export.

Likewise, India’s coffee export declined by 17.2% per cent to 168,435 tonnes for the period from January 1 to July 23, 2020, compared with the same period in the previous year. The plunge has been severe in the case of robusta variety beans at 26 per cent.

Coffee prices have been on the rise due to high demand and low supply, is a trend that is likely to continue.

The Tickers

The Top Gainers in the Tea and Coffee Industry for the month of July 20′ are as follows:

Average Revenue Growth of Tea and Coffee companies was 27.74%. EBIT Growth for Tea and Coffee companies was 72.4%. Operating Profit growth for the companies was 68%. All of this over a year. The tea market just luke other companies initially slumped which was followed by a spikey/volatile recovery as the companies started posting excellent results.

How was is it that reduced production still resulted in tea and coffee companies making a profit?

India is the largest consumer of tea in the world. The production slowed down, but the demand never went down very much. After the lockdown was imposed the demand for out-of-home Tea slumped, but demand for Tea inside households covered up for it to some extent.The demand for Tea overall can never die down in a country like India.

According to data from the Indian Tea Board, there is a reserve inventory or a buffer stock for at least 145-165 Days when the lock-down was imposed. The Tea picking season had just ended in March when the lockdown was imposed. It is THIS Tea that met with the consumption demand and added to the profits of Tea companies

Why the panic in the newsroom then? The demand for three months of Tea was met, but the non-availability of labour and resources during the lockdown is what caused panic in the market. There was an uncertainty about when the production of Tea would resume. This made it difficult for companies to plan prospects or ordersof Tea causing prices to skyrocket. This was a supply constraint.

June-July 2020 data from Indian Board show that India’s Tea production has started closing up to pre-COVID levels. It will be clearer through August-September data whether India will be able to supply the consumption and export demand or not.

On the other hand, Coffee conglomerates like Tata Consumer Products and Tata Coffee managed to perform well because of its international presence with the likes of Eight O’Clock Coffee and Tata Coffee Vietnam Company (TCVCL).

Medium and small farmers were already having difficulty covering operating costs. The decrease in prices in recent years has made their livelihood increasingly difficult. Therefore, the main risk is the possible shortage of manpower due to the spread of the virus and the measures of lockdown.

What drives Tea and Coffee Prices?

The concentration of production: Brazil and Vietnam happen to be the top two producers of coffee, This concentrated output means that supply disruptions in one or both of these countries can have a significant impact on the price of coffee.

Substitution to cheaper beans or leaves: In the Tea and Coffee business, there are cheap beans/leaves and expensive finer beans/leaves. If it so happens that the price spread between the cheap and expensive one’s increases then companies will start substituting the cheaper ones into their blend. This is a positive signal for India in terms of coffee This is because 70% of India’s produce is Robusta.

The price of substitute products: Tea and Coffee are substitute goods, one should analyse the trend in either side to be able to speculate which good will be more in demand and where? Other substitutes for caffeine include energy drinks and supplements.

The weather: Coffee in India mostly depends on monsoon and humidity. A poor monsoon or irrigation facility means that coffee production will be hampered. If climatic conditions are unfavourable for tea plantations owing to less or heavy rainfall that also poses severe problems affecting the production of tea and lives of tea industry labourers.

Yield: There is a fair possibility that the Tea bush or coffee plant might rot or be rendered unsuitable due to conditions like pest, disease or climatic conditions. It is necessary to check the yield provided by Tea and Coffee plantations. The data for which is available on India Tea Board or Indian Coffee Board.

Supply Chain and Logistics: The customs duties exposed on the import and export of coffee has a huge impact on the price and demand of the coffee. One should look out for trade and policy changes between countries.

What’s the Future Like?

During the period of the lockdown Tea and Coffee, production was impacted. However, June-July numbers of production show some sign of positivity in terms of production as it returns to normalcy. Tea has a huge potential export value as the international market shifts towards a more healthy lifestyle and the adoption of Tea increases as a substitute for widely preferred coffee.

On the other hand, the Chai drinking nation of India sees greater potential in rising demand for premium coffee as people’s disposable incomes rise and so does their taste for good tasting coffee. Moreover, the North Indian Market isn’t as penetrated as the South Indian market in terms of coffee consumption.

Tea and Coffee are two products that stimulate the human mind, so much so that many around the world have made it a part of their daily routine. The possible reason why the Tea and Coffee market in India suffered in COIVD is the disruption of Logistics, Supply Chain and Labor along with the uncertainty of things getting back to normal. Huge potential lies in the future ahead for the two to prosper.

The COVID-19 pandemic left economies devastated, and people without jobs. And as we all saw in the headlines of every newspaper, there was a rather difficult mass migration from urban to rural India. This left two dilemmas, what shall happen to the decreased urban demand? In the absence of income, how will consumer spending thrive in rural areas?

There was rising a rising sense of uncertainty. The suddenness of events left many confused. The lack of knowledge and research about the virus caused panic throughout caused by rumours. What many failed to notice in India was the resurgence of a rural economy in the underbelly of COVID-19 lockdown.

Many migrant workers started returning to their home states by every means possible and other Govt. initiatives like the shramik express. This would mean that urban consumption and demand for goods would go down whereas it would increase in the rural areas. To sustain in rural areas the most suitable source of income is Agriculture. How exactly was agriculture impacted in COVID-19 pandemic?

How do I catch the Rural Theme in markets?

There is almost no other reliable source of income in rural areas apart from agriculture and dairy. When the lockdown was imposed it was amidst the Rabi Crop Harvesting Season(April-May), the seizure of the supply chain and logistics served a major blow to it.

However, there were multiple stimulus packages aimed specially to benefit the rural areas. MNREGA(Mahatma Gandhi National Rural Employment Guarantee Act), Pradhan Mantri Garib Kalyan Anna Yojana (PMGKAY) and other direct benefit transfer schemes.

Spurt in rural spending will not only benefit a lot of agri-related equipment but also other aspirational products. Look out for greater demand for FMCG products, two-wheelers, entry-level cars etc. All these are aspirational products for the rural population and could see a distinct rise in demand in the coming month

Rural housing could be a big theme in the coming months. The government has already laid emphasis on low-cost housing by giving it infrastructure status. Companies that operate in this space with a credible and sustainable business model will be among the names to benefit from this development.

The rural population has managed to adapt and invest in its own setting. There has been an encouragement in enabling farmers to obtain long-term debt in order to kick start the agrarian economy.

As the monsoon season approaches, there has been more than normal sowing of “Kharif” crops to ensure a healthy income in the harvesting season in the coming winter season.

As many parts of India face a water crisis till date you can expect a fair share of a boost in the irrigation systems like motors, pipes, channels etc.

Automobile

As People started migrating to rural areas, there was a rise in rural population. 70% of rural household occupationally rely on agriculture as a source of livelihood. When the sales of a passenger vehicle, two-wheeler and commercial vehicles slumped, those of Farm Equipment Sector (FES) such as tractors and tillers rose. Some players in the industry include Mahindra and Mahindra, Escorts and VST Tillers.

Read more about Automobile sector during COVID by clicking here.

Agro-Chemicals, Pesticides and Fertilizers.

The use of pesticides and agro-chemicals in agriculture increase marginally.

Kilpest India Ltd. showed an amazing performance, both in terms of Quarterly (1,093.2%) and Yearly (1814.86%) Net Profit. Kilpest India Ltd is one of India’s leading Agri based companies. Kilpest is an ISO certified company and has representation in India in the field of agriculture business comprising Crop Protection Products and Public Health Products, Bioproducts, Micro-Nutrients and Mix fertilizers.

United Phosphorus Ltd (UPL) and PI Industries (PIIND) are the two of the biggest players in the pesticide and agrochemical industry in India. United Phosphorus recorded 200% Net Profit Growth QoQ and PI Industries had a .

Price levels of KILPEST UPL and PIIND

Coming to fertilizers, government data states that fertilizer sales jumped 83% to 111.61 lakh tonnes in Apr-June. Read more over here.

Growth in Fertilizers sector(Amount in Rs. Crores)

Another company that is worth taking note of isRallis India Ltd. which is a subsidiary of Tata Chemicals, the company filed a quarterly Net Profit of 13,000%(Between April and June)! Rallis India Ltd. specialises in crop-care, pesticide, agrochemical and other agri-care products.

How have “rural themed” FMCG companies performed?

Dabur and Emami are two FMCG companies with a strong ruralpresence. While Dabur has a market cap of more than Rs.90,000 Crores and Emami has a market cap of Rs.14,860 Crores.

Dabur and Emami recorded Net Profit growth% of 21% and 60.8% each respectively. They are an essential bridge between rural areas and FMCG market considering that rural India accounts for 37 per cent of India’s FMCG spends, both these companies have a very strong rural presence.

Did the Rice Market Benefit?

India had the highest export volume of rice worldwide, at 9.8 million metric tons as of 2018/2019. India’s rice export fell due to slowdown and seized the supply chain but increased by 52.5% in April-May.

India handles 25% of global rice exports, However, rice contributes only 2 per cent to the Indian export basket. The COVID situation caused many non-agricultural and developing countries to put a cap on rice exports to meet local supplies. On the other side, India maintains a surplus of rice making exports of huge volumes possible.

We have taken two companies that benefited from this rising foreign demand.

Chaman Lal Setia Exports Ltd (Market Cap: Rs. 532 Cr)– Chaman Lal Setia Exports Ltd. is an India-based manufacturer and exporter of basmati rice. Chaman Lal Setia Ltd declared a Net Profit growth of (+)21.6%

GRM Overseas Ltd (Market Cap: Rs. 122 Cr) – GRM Overseas Limited engaged in the business of manufacturing and trading of rice. The Company produces a range of rice items to its customers spread across the world. GRM Overseas Ltd declared a Net Profit growth of (+)351.7%

Sale of Seeds in India.

Kaveri Seed Company Ltd. and Mangalam Seeds are one of the top seed companies. Indian stock markets have had a long affair with monsoons. Although Mangalam Seeds Ltd. has not declared its quarterly result, there is a strong sentiment regarding the forecast due to rising agriculture and pre-monsoon sowing both on the rise. Kaveri Seeds’ QoQ Net Profit Growth was 3,794.67%

JK Agri Genetics Ltd. is an India-based seed company. The Company is engaged in growing of non-perennial crops. It provides Agricultural and allied products and isalso involved in research and development, production, processing and marketing. It showed growth of +308.1% in Net Profit QoQ with a +295.7 Revenue Growth QoQ.

Nath Bio-Genes (India) Limited is engaged in the hybrid seed business. The Company is engaged in the business of production, processing and marketing of hybrid and genetically modified (GM) seeds. The Company’s segments include agricultural activities (seed production) and trading activities. Nath Bio-Genes Ltd.’s Net Profit multiple over FOUR TIMES after the lockdown.(~+411%)

NIFTY FMCG outshines NIFTY 50

NIFTY FMCG is the index that is closest to the agriculture sector than other indices. We take a 6-month time frame to analyse which index has suffered from COVID-19. While NIFTY 50 overall faces an overall decline of -6.65% NIFTY, NIFTY FMCG managed to recover and shine 3.79% more.

Surge in Rural Area Usage.

Shortly after the lockdown, there was a dip in data usage for a very small period. Post this the amount of data usage surged massively. Such that a majority of these data users belonged to the rural area. Data consumption under BharatNet(Read More Here) across the country in the April-June quarter was 5.52 lakh gigabyte (GB) as compared to 2.47 lakh GB in January-March. Overall, rural areas accounted for 83.3 per cent of the total 6.58 lakh GB data consumed under BharatNet across India during April-June.

Sum and Substance

In a survey conducted, more than 68% of the population in rural India faced a monetary crisis. 78% suffered job losses because of stringent lockdown measures put in place to control the spread of the virus, said the survey, The Rural Report, conducted by news portal Gaon Connection and Delhi-based Centre for Study of Developing Societies.

As much as 23% of the respondents were forced to borrow money to manage their households, while 8% had to sell a valuable possession The survey said that 28% of migrant workers were not paid for the work they had done in cities.

Only 27% of the economically poor households, which did not have ration cards to access the central scheme for highly subsidized foodgrain, said they had received wheat or rice from the government.

The monetary crisis caused physical dismay, the government support and fiscal stimulus even though was the best case scenario made way only for Dalal Street to book profits in certain segments. The socio-economics scenario can’t be portrayed in numbers.

The Rural themed stocks showed great results due to lesser population densities in rural areas and therefore lesser chances of contracting COVID making economic activity possible. Despite that, there has been a rising pile of COVID-19 cases in tier 3 and tier 4 cities putting the FMCG as well in an expected dismay.

There is just one hinge around which Dalal Street is balancing itself and that is the COVID-19 Vaccine.

We are in unprecedented times with COVID-19 having a lasting effect on every industry. And then there is the aviation industry and tourism industry which has hit rock bottom, and not recovered. Today, we are going to talk about how the Indian aviation industry has fared during these unusual times.

The aviation industry might be facing the worst turbulence in its history. To reduce the spread of the virus, the domestic airline industry came to a screeching halt in March. After a month and a half, the airline’s services were given the nod to continue subject to numerous conditions. Data from DGCA (Directorate General of Civil Aviation) showed that air traffic has plummeted by 85% year-on-year in the month of June. It is expected that the airline traffic in the Asia-Pacific region will be the hardest hit during these times.

Competition based on Price

India had 650 aircraft in service last fiscal year. The industry generated employment for more than 75 lakh individuals. India’s business model in the aviation sector is very different from other countries. Flights like Indigo, Air India or GoAir does not offer a lot of premium services. An average Indian passenger would want to travel from X destination to Y destination safely and at a cheap price. International carriers like Etihad offer more services and charge additional fees for those services. Thus, the Indian airline sector competes on the basis of price and not on the basis of luxury service.

Here comes the component of success for this strategy : Passenger load factor.

Passenger load factor measures the capacity utilisation of an airline. The more the passengers on a flight, the more beneficial it is for an airline. This is because, with the limited number of crew members and no luxury services, the additional cost of adding one more passenger is not much. Thus, the money which comes from additional passenger adds more to the company’s profit. This passenger load factor has decreased to 50%-60% for almost all the airline during the recent months. Last December, this factor varied between 80%-90%. As the number of passengers decreased, airlines failed to break-even and earn profits.

Recent Numbers

Indigo is the biggest airline in India. It has a market share of over 40%. Their Q1 FY21 was below what market estimated and dismal, to say the least. Their revenue fell by 91% and net losses of Rs 2844 crore were recorded. To get more idea, read here. SpiceJet is yet to declare their results for the first quarter. In Q4 FY20, SpiceJet reported losses worth Rs 807.1 crore and the results for the subsequent quarter is expected to be worse.

The demand for air travel is already very low and reports suggest that the overall demand for air travel this fiscal year might fall by 45%-50%. According to ICRA ( a credit rating agency), India’s aviation sector is losing Rs 75 crore per day. It is further expected that the sector will lose Rs 17,000 crore in the current fiscal year. According to the report of Crisil (an Indian rating agency), this loss might stretch till Rs 25,000 crore for this year.

In order to conserve cash flow, Indigo has already announced 35% pay cuts for its senior employees. This was the second pay cut for the company in as many months as they had announced a 25% pay cut in May. The company has also announced to lay-off 10% of its workers.

Spicejet has not announced any lay off till now, but will not be paying full salary to 92% of their employees. Vistara also announced a pay cut of 5% to 20% for its 40% of employees till the end of this year.

One of the main reasons why the airlines are still able to stay afloat is the low prices of crude oil. Jet fuel is recovered from refining the crude oil. The prices of crude oil have consistently declined over the past 6 months due to a sharp fall in demand amid COVID. This has helped the airline by cutting their fuel expenses sharply and giving some space to their bottom line to breathe.

How can the government help?

The airlines have been forced to cut shifts, ground their fleets and reduce the workforce. Even after desperately trying to cut costs, the industry has been forced to pay for fixed costs with cash. This is a very grim sign for any business.

The airline industry is highly leveraged. It needs heavy investment and regular cashflows so that the company do not default from their payments. Their primary source of cash flows is blocked. Thus, the chances of bankruptcy for the companies belonging to this industry is very high.

One thing is clear that the airlines cannot survive on their own and they need help from outside. This leaves the responsibility on the national government to roll out friendly schemes for the revival of the industry. The national government should look to waive off taxes and other charges of landing and parking. They should also think to let the airlines take loans at a very low rate and ask the banks to be lenient during the restructuring of the loans.

Companies are also pondering over the idea to switch passenger planes into cargo planes as the demand for the latter is higher. SpiceJet also showed their intent to increase the number of aircraft flying (cargo+cargo on the seat) to more than 50%.

Can the situation change any time soon? No one knows till when this pandemic will last. There is a huge uncertainty on how the things will fold for this sector. It is fair to say that airlines are set to continue their struggle for survival. The government and the aviation ecosystem should take this pandemic as a learning event and proceed to build a robust, efficient and viable structure for the industry.

On 23rd April 2020, Franklin Templeton announced the shut down of its six Debt Mutual Funds with Rs.26000 Crore Asset Under Management(AUM) due to pressure and lack of liquidity in the bond market. Just after it shut shop it managed to secure liquidity of Rs 1,964 crore from its investments. The six debt mutual funds were:

Six Debt Funds of Franklin Templeton which Shutdown in April.

What is a Debt Fund?

A debt mutual fund is a fund which invests a majorly in fixed-income/low-risk securities like bonds, government securities, debentures, corporate bonds etc. Debt funds come with a lower degree of risk than equity funds. However, they are subject to market risk and do not guarantee fixed returns.

Debt funds come in various types depending on their maturity period, lock-in period or asset classification.

Companies/Government entities issue bonds to raise debt/funds for their activity, Mutual Funds buy these bonds and wait for the bonds to mature. The Mutual Funds and AMCs in return get the interest/payoffs on these bonds. The interest earned is the distributed amongst the investors.

Risks in Debt Funds

Debts funds fundamentally carry three types of risks:

Credit Risk – which is the default risk of the issuer not repaying the principal and interest.

Interest Rate Risk – which is the effect of changing interest rates on the value of the scheme’s securities.

Liquidity Risk – which is the risk carried by the fund house of not having adequate liquidity to meet redemption requests.

*Redemption- The process where an investor withdraws his money from a mutual fund is termed “redeeming” his fund and the process is called Redemption

Returns

Debt funds offer lower returns as compared to equity funds. Also, there is no guarantee of the returns. The NAV(Net Asset Value) of debt funds fluctuates with changes in the interest rate. If the interest rates rise, then the NAV(Net Asset Value) of a debt fund falls and vice-versa.

Why did Franklin Templeton Shut-down?

The story goes right back to November 2018. The ship that sank all around it, the IL&FS fiasco caused a credit crisis in India followed by a rise in the ocean of Bad-Debts, NPAs and defaults. Then came fraudulent activities of Vijay Mallya, Nirav Modi and Mehul Choksi adding to the crisis. This caused the enforcement agencies and NBFCs to tighten the taps. Many of the companies which sank in an around this period happened to have a not-so-good credit rating.

Credit ratings of a company’s bonds range from AAA(+/-), AA(+/-), A(+/-) to………. CCC, CC, C D. AAA is considered as the highest grade and D is considered the lowest grade.

For this case, we’ll consider any bond at A(+/-) and below to be a lower credit rating or a not-so-good credit rating. Franklin Templeton has HUGE exposure and had invested in these very high-risk instruments more than its other counterparts. Why did Franklin Templeton do that?

Asset Allocation of FT Debt Funds.

Higher risk means higher interest earned. This very method helped the fund manager Santosh Kamath earn big bucks previously at Franklin Templeton. Franklin Templeton’s strategy of investing in corporate bonds of lower-rated companies ensured that its debt funds stayed ahead of the competition for many years.

The fund house had invested in companies and corporate houses such as Dewan Housing Finance Corporation, Essel Group, Reliance Anil Dhirubhai Ambani group, Yes Bank and Vodafone-Idea. See a pattern?

All these companies have either defaulted huge loans, made fraudulent transactions or have undergone bankruptcy. Franklin Templeton had invested Rs. 560 crores in DHFL, Rs. 1009 Crores in Essel Group, Rs.960 Crores in Reliance ADAG Group Companies, Rs. 2058 Crores in Vodafone-Idea and 1088 in YES Bank.

The MAIN reason for the meltdown of Franklin Templeton were defaults made by these companies on interest payment obligations. This caused a certain amount of panic, to which COVID-19 was an additive, causing redemptions to rise, investors pulled out their money from the funds. This caused a liquidity crisis.

There has been a dramatic fall in liquidity in the Indian Bond Market due to the Covid-19 lockdown. The increasing redemption pressure on the funds has mounted additional pressure on the fund managers to sell the more liquid bonds and pay the investors back

Between March 31st and 20 April, the company faced a redemption(investors pulling our money) of almost Rs.14,000 Crores, this was fueled by the rising number of COVID-19 cases till the decisions to windup the mutual fund was made.

Who is to be blamed? Markets or Franklin Templeton?

A forest fire can be prevented by a glass of water, provided it is used at the right time.

Analysts’ opinion remains that having such a huge exposure to high-risk bonds without evaluating the position of the asset is uncalled for. The COVID-19 pandemic added fuel to the fire, people feared a credit default considering the lockdown. Debt funds and Credit risk became the lesser opted for instruments. The classification of assets was done in an unprecedented manner.

How are Debt Funds for Now?

Franklin Templeton Mutual Fund’s six closed schemes have received Rs. 4,280 crores from maturities, pre-payments and coupon payments since the announcement of their closure in April. This is 5 per cent of the remaining ~Rs.20,000 Crore.

Fixed income securities or debt funds witnessed an inflow of Rs 91,392 crore in the month of July as compared to Rs. 48,000 Crores in April. The recent RBI MPC meeting too had no effect on the bond market whatsoever.

Debt funds with fewer risks remain viable. Corporate bonds, banking, and PSU bond funds are among mutual funds that are generally known to carry the lowest risk. Liquid funds and overnight funds are also comparatively safe in this scenario. Some select low duration and short-term schemes may also be counted as low risk.

This has a lesson for many investors who simply look at the returns of a particular mutual fund before deciding to invest in it. It is necessary to go through the mutual fund’s fact sheet and profile which is published by every AMC publicly. And as they say,

Mutual funds are subjected to market risk, read all scheme related documents carefuly!