Credit ratings play an important role in the world of finance. It indicates the safety or risks associated with different securities (stocks, fixed-income securities like bonds, etc.) and their issuers. It provides crucial insights into the world of investments. In this article, we will discover what credit ratings are, how they work, and their role in the financial markets. We will also explore the different credit rating agencies and their credit ratings.

What are Credit Ratings?

A credit rating is an assessment of the creditworthiness of a borrower, whether it’s an individual, a corporation, or a government. It is a symbol assigned to a security or issuer that represents its creditworthiness or safety. Credit rating agencies (CRAs) are responsible for assigning these ratings. Their primary goal is to provide a standardised evaluation of credit risk, which allows lenders and investors to make informed decisions regarding lending or investing in debt securities.

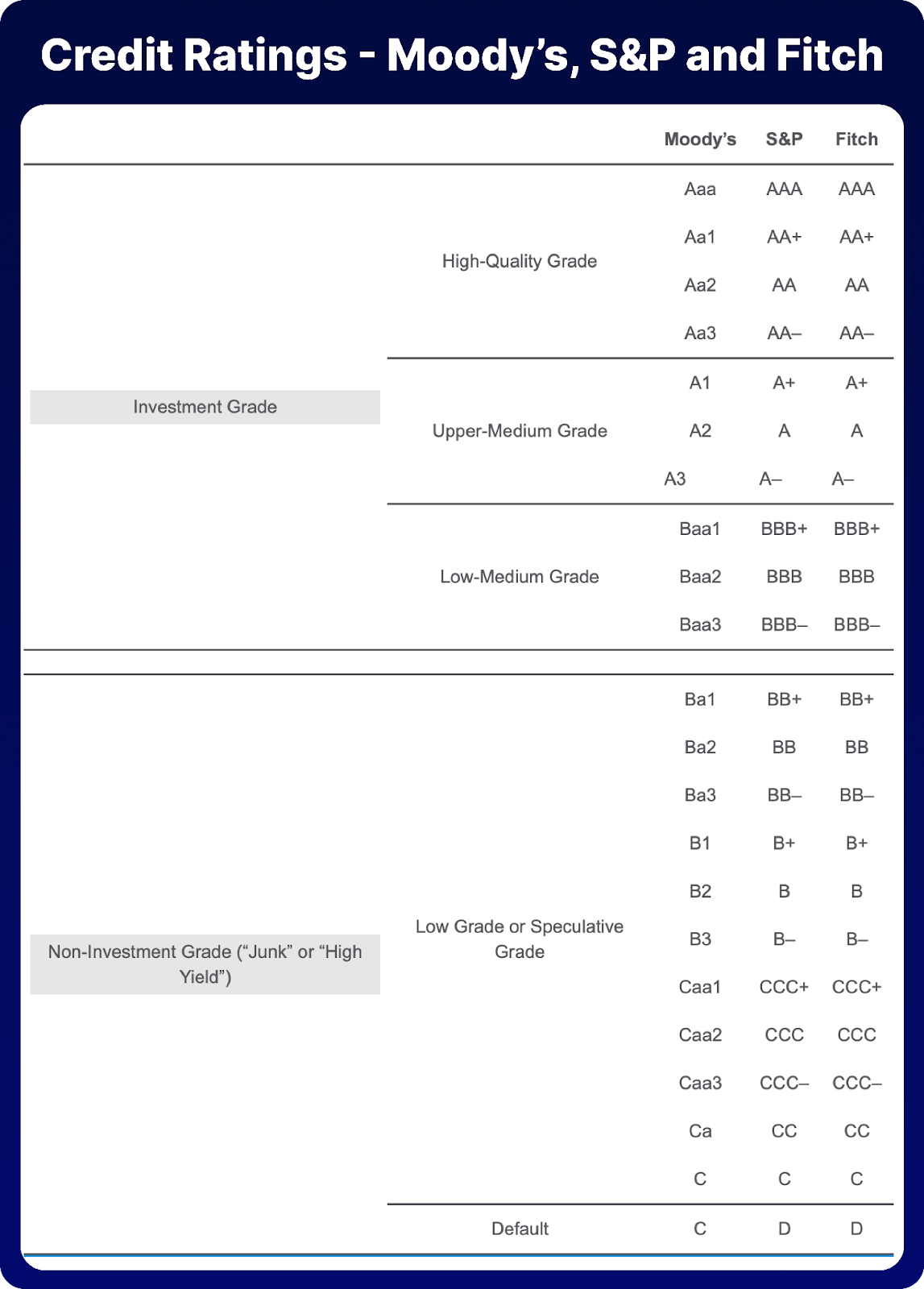

Credit ratings are generally expressed as letter grades, such as “AAA,” “BBB,” or “C.” Each rating corresponds to a level of credit risk and reliability. The specific rating scale may vary slightly between different credit rating agencies, but the core principles remain the same. The three major global credit rating agencies (CRAs) – Moody’s, S&P, and Fitch use similar, symbol-based ratings to assess a bond issue’s risk of default.

The chart given below ranks the long-term ratings of CRAs from highest to lowest.:

Bonds with high-quality grade ratings are the safest and carry lower interest rates. On the other hand, low-grade or speculative-grade issues are the riskiest and carry high interest rates as they involve greater risk. Credit rating agencies assign default ratings to bonds that have defaulted on their payment obligations.

Moreover, rating agencies will typically provide outlooks on their respective ratings. The outlook can be positive, stable, or negative. They may also offer additional signals about the possible future direction of their ratings, like indicating that a bond is ‘On Review for Downgrade’ or ‘On Credit Watch for an Upgrade’.

What is Credit Risk?

Credit risk is the risk of loss resulting from the issuer’s failure to make full and timely payments of interest and/or principal. Credit risk has two components:

1. Default Risk/Default Probability: It is the probability that a borrower defaults. A borrower is said to be in default if they fail to make full and timely payment of principal and interest as per the terms of the debt security.

2. Loss Severity: The second component is the loss severity in the event of default. It is the portion of a bond’s value (including unpaid interest) an investor loses. A default can lead to losses of various magnitudes.

You can summarize the credit risk of a security or issuer as the expected loss.

Expected loss = Default probability × Loss severity

You can express the expected loss either as a monetary amount (e.g., ₹4,50,000) or as a percentage of the principal amount (e.g., 45%).

What are Credit Rating Agencies?

Credit Rating Agencies (CRAs) are independent entities that assess and assign credit ratings to various debt issuers and their securities. These agencies provide valuable insights into the creditworthiness of governments, corporations, and other entities.

CRAs are independent organisations, which means that they are separate from the entities they rate. These agencies must be independent to avoid conflict of interest. They evaluate the issuer based on various criteria and assign a credit rating. The rating symbols vary depending on the rating agency. Moody’s, Standard & Poor’s (S&P), Fitch Ratings, Credit CRISIL, CARE, and ICRA are among the top credit rating agencies.

Common Credit Rating Categories

Here are some of the common credit rating categories:

- Investment Grade:

- AAA (or Aaa): The highest credit quality with the lowest risk of default.

- AA (or Aa): High credit quality with a very low risk of default.

- A: Good credit quality with a low risk of default.

- BBB (or Baa): Adequate credit quality with a moderate risk of default.

- Speculative Grade (or Non-Investment Grade):

- BB: Speculative credit quality with a moderate risk of default.

- B: Highly speculative credit quality with a significant risk of default.

- CCC: Substantial credit risk with a high risk of default.

- D: In default or near default.

How Do CRAs Assign Credit Ratings?

Credit rating agencies evaluate both quantitative and qualitative aspects of borrowers, including:

- Financial Statements: They review financial statements such as balance sheets, income statements, and cash flow statements to assess the financial health and stability of the borrower.

- Credit History: CRAs analyse the credit history of individuals and the repayment history of corporations and governments to assess their ability to meet financial obligations.

- Economic and Industry Factors: Agencies consider the broader economic environment and the specific industry or sector in which the borrower operates to understand the challenges and growth opportunities it may face.

- Debt Structure: CRAs examine the structure of the borrower’s debt, including the types of debt securities issued and their terms to evaluate repayment capacity.

- Market Conditions: Current market conditions and trends, including interest rates and inflation, are considered to assess potential risks.

- Management and Governance: Credit rating agencies scrutinize the quality of management and governance practices of corporations to understand how effectively the entity is managed.

After analysing these factors, credit rating agencies assign a rating that reflects the borrower’s creditworthiness and likelihood of default. The specific rating categories can vary between agencies, but they generally follow a similar pattern.

How do Credit Ratings Affect Borrowing Costs?

Lenders and investors consider borrowers with higher credit ratings as less risky. As a result, they can access loans and credit at lower interest rates. Meanwhile, borrowers with lower credit ratings are considered riskier. So lenders charge higher interest rates to compensate for the increased risk. Entities with better credit ratings pay lower interest rates on their debt.

For example, a bond with an AAA rating will have lower interest rates, compared to a BBB-rated bond (if all other factors remain the same).

Why are Credit Ratings Important?

- Risk Assessment: Credit ratings help investors and lenders assess the credit risk associated with a particular borrower. A higher credit rating indicates lower risk, while a lower rating suggests higher risk.

- Pricing of Debt: Borrowers with better credit ratings can access credit (loans) at lower interest rates because they are considered less risky. Meanwhile, borrowers with lower ratings may face higher borrowing costs.

- Investment Decisions: Investors, including individuals, mutual funds, and institutional investors, use credit ratings to make informed decisions about investing in debt securities. Investors often consider higher-rated securities as safer investments.

- Regulatory Compliance: Many financial institutions and regulations require a minimum credit rating for certain types of investments or transactions to ensure a level of risk management.

- Risk Diversification: Credit ratings help diversify risk in investment portfolios by allowing investors to allocate funds to securities with varying risk levels.

What are the Risks of Relying on Credit Ratings?

- Credit rating agencies are paid by the companies and governments that they rate. This can create a conflict of interest, as the agencies may be incentivized to give higher ratings to their clients.

- CRAs can make mistakes, and these mistakes can have a significant impact on investors. For example, in 2008, Standard & Poor’s gave high ratings to many mortgage-backed securities in the US that later defaulted. This led to billions of dollars in losses for investors.

- These agencies are not required to disclose their rating methodologies. This makes it difficult for investors to assess the accuracy of their ratings.

- Credit ratings tend to lag the market’s pricing of credit risk.

It’s important to note that investors should use credit ratings in combination with other factors, especially their own research & analysis, while making investment decisions.

In conclusion, credit ratings are essential tools in the financial world, providing a standardized way to assess credit risk and make informed investment and lending decisions. Whether you’re an investor looking to diversify your portfolio or a borrower seeking to access capital, understanding credit ratings is key to navigating the complex landscape of finance.