Investing through Systematic Investment Plans (SIPs) can be a powerful way to grow your wealth over time. However, many investors unknowingly make mistakes that can severely limit their returns. These mistakes often allow brokers or banks to benefit at your expense, leaving you with lower profits than expected. In this article, we’ll explorefive common mistakes SIP investors make and how to avoid them. Learn how to maximise your profits and safeguard your financial future!

1. Choosing Regular Mutual Funds Over Direct Mutual Funds

One of the most common mistakes investors make is not understanding the difference between regular and direct mutual funds. Regular mutual funds involve a middleman—often an agent or broker—who takes a commission on your investments. This commission can range from 1% to 1.5% or even higher, depending on the mutual fund scheme. Over time, this seemingly small percentage can have a massive impact on your returns.

For example, if you invest ₹10,000 every month in a regular mutual fund with a CAGR (Compound Annual Growth Rate) of 22.8%, your returns after 20 years could amount to ₹4.63 crores. However, if you had chosen a direct mutual fund with a slightly higher CAGR of 24.6%, your returns would have increased to ₹6.33 crores— a difference of ₹2 crores!

Solution: Always opt for direct mutual funds when possible. You can easily switch from regular to direct funds by stopping your regular SIPs and starting new ones with direct funds. While there may be a small tax implication, the long-term benefits are worth it.

How to Identify Regular and Direct Mutual Funds?

When investing, look for clear indicators on the mutual fund’s platform. Most reputable mutual fund houses will display both regular and direct options. If you’re approached by a bank or broker, they will likely recommend regular funds. If you prefer to manage your investments independently, opt for direct mutual funds to enhance your returns.

2. Selecting IDCW Mutual Funds Instead of Growth Plans

Another common mistake is choosing Income Distribution cum Capital Withdrawal (IDCW) mutual funds instead of Growth Plans. IDCW funds distribute dividends to investors, which might seem attractive for those seeking regular income. However, this option can hinder the compounding benefits of your investment, ultimately reducing your long-term returns. In contrast, growth mutual funds reinvest profits back into the fund, allowing your investment to compound over time.

For instance, an HDFC Flexi Cap mutual fund with an IDCW option might yield a 12% CAGR, whereas the same fund with a growth option could yield over 23% CAGR. The difference in returns can be substantial over time. Moreover, the taxation on IDCW could further reduce your net gains.

Solution: Always choose the growth option if your goal is long-term wealth creation. This allows your returns to compound within the fund, leading to higher gains over time.

3. Lack of Diversification: Investing Solely in Small-Cap Funds

Diversification is a fundamental principle of investing that many SIP investors overlook. Investors often get swayed by the impressive returns of small-cap funds, leading them to allocate all their investments into these high-risk funds.

While small-cap funds may have outperformed the market recently, they can also be highly volatile. Investing all your money in small caps without diversifying into large-cap or mid-cap funds exposes you to increased risk. During market downturns, small-cap funds often underperform, which can lead to significant losses.

Solution: Diversify your investments across large-cap, mid-cap, small-cap, and flexi-cap funds. You can also consider a portfolio that includes various asset classes, such as gold and debt instruments. For example, gold often performs well during market crashes. This provides a safety net that can be leveraged when equity investments decline in value. This strategy allows you to capitalise on different market conditions and helps mitigate risks.

Identifying Overlap in Mutual Funds

Even when diversifying, it’s crucial to ensure that your funds are not investing in the same underlying stocks. Use platforms to check the fund’s holdings and understand their investment philosophy. If multiple funds have significant overlaps in their holdings, it reduces the effectiveness of your diversification strategy.

4. Not Having an Emergency Fund

Investing in SIPs without first establishing an emergency fund is a mistake that can jeopardise your financial goals. Life is unpredictable, and an unexpected event, such as job loss or a medical emergency, could force you to sell or liquidate your SIP investments prematurely. This could result in losses, as you may need to sell your holdings during a market downturn.

Solution: Before starting any long-term investments, ensure you have an emergency fund in place. This fund should be easily accessible and sufficient to cover at least six months of living expenses. You can keep this fund in a high-interest savings account or a liquid mutual fund.

5. Ignoring Health and Term Insurance

Many individuals are eager to grow their wealth through SIPs but overlook the importance of protecting themselves and their families against unforeseen events. Health emergencies can arise at any time. Without proper insurance, you may be forced to dip into your investments to cover medical expenses.

For instance, let’s say you’ve been investing ₹10,000 monthly in SIPs, targeting ₹6.33 crores over 20 years. However, a health emergency after five years forces you to withdraw from your SIPs, leaving you with only ₹11.8 lakhs—far below your goal.

Solution: Ensure you have a comprehensive health insurance plan and a term insurance policy before committing to long-term SIP investments. If you have limited funds, it’s better to reduce your SIP contributions to allocate some funds towards insurance premiums. This safety net will protect your investments and help you stay on track to achieve your financial goals.

Conclusion

Investing in SIPs can be a rewarding strategy for wealth accumulation, but it’s essential to avoid common mistakes that can undermine your efforts. By understanding the differences between regular and direct mutual funds, choosing the right fund type, diversifying your investments, establishing an emergency fund, and securing adequate insurance, you can enhance your investment outcomes significantly.

Take the time to review your current investment strategy and make necessary adjustments to avoid these mistakes. By doing so, you will not only protect your wealth but also maximise your potential returns over the long term. Start today by addressing these critical areas and watch your investments flourish!

Before you learn about the stock market, it is essential to understand why it should interest you, how you plan to generate income from it, and what kind of activities you should do in the market. There are a lot of different perspectives out there when it comes to the world of the stock market. Some people think it’s a great way to make money, while others think it’s a huge gamble. The core objective of this article is to change mindsets and set a strong perspective.

Why Should You Be Interested in the Stock Market?

To understand why you should become interested in the stock market, we must first understand what everyone is striving for in today’s socio-economic environment. What is the absolute goal of an average person? It’s financial freedom!

What is Financial Freedom?

Financial freedom is a desirable condition of having enough money in your bank account to cover your expenses without having to work, run a business, or rely on others. Many people aspire to achieve it before they retire. Financial freedom allows you to pursue your passions without worrying about expenses, even if your passions do not generate income.

Normally, people save a part of their income and deposit it in their savings account, fixed deposit, or recurring deposit. They invest to generate wealth, which can then be used to take care of any long-term financial goals or expenses after retirement. However, it is impossible to achieve financial freedom by such methods as the annual returns generated by these financial instruments are only 5-7%. They cannot help you generate enough income to beat inflation.

Inflation in India stands at ~6%, and if you keep your money in a savings account or deposit it into FDs or RDs, you’re barely beating inflation. You won’t even make enough money to keep aside as savings after accounting for all expenses. So what can you do?

The stock market can be one of the most convenient and easy ways to achieve financial freedom as it offers more returns on your investments.

How to Use the Stock Market to Achieve Financial Freedom?

There are mainly two types of activities in the stock market that a retail participant can take part in:

Trading

Investing

Trading is the buying and selling of stocks for short periods (intraday or for less than a year) or futures and options to generate income in a short period. There are different types of trading such as intraday trading, swing trading, and positional trading, which we will discuss in later sessions. People trade to generate cash flow instead of generating wealth through long-term investing.

Long-term investing involves buying and holding stocks, bonds, commodities, mutual funds, and exchange-traded funds (ETFs) for extended periods to grow your wealth.

How do Trading and Investing Solve the Problems of an Average Person?

If you recall, the key issue most people face is the inability to beat inflation. So an average person can beat inflation by investing in the stock market for the long term instead of depositing their savings in a fixed deposit, recurring deposit, or even their bank savings account. Long-term investing can help you amass great wealth by generating higher returns. We should view it as a fundamental duty of every citizen.

The second pressing issue for many people is insufficient income to start investing. With rising expenses, they may not have enough salary or wages to set aside to make investments. To fix this issue, a person can upskill for a higher-paying job, start a business, or trade in the stock markets. You can trade both actively and passively.

Should Everyone Trade?

The only motive for trading is to make money or an extra income. Trading is a choice. If you have the potential to make enough income by increasing your skills in your current job or business, then trading is not necessary.

The stock market is a great way to make money. However, it can also be risky. So it’s important to learn the fundamentals of the stock market before you invest or trade. We hope that you have gained clarity on why you should be interested in the stock market and whether you should engage in trading, investing, or both.

Index funds have gained popularity in the world of investing, offering a simple and effective way for individuals to participate in the stock market. There are funds that invest in a broader market index like Sensex or Nifty. Index funds replicate the risk and return of the market. In this article, explore some of the best index funds to invest in India.

Index funds are those which are not actively but passively managed by the portfolio managers. If an investor invests in an index fund, the maximum return he can receive is the market return. This return is lesser than the market return because of additional costs involved in investing.

How do Index Funds Work?

Consider an index fund that follows the NSE’s Nifty Index. There will be 50 stocks in this fund’s portfolio, all of which will be distributed in the same way. The index fund makes sure to invest in each and every security that the index monitors.

A passively managed index fund attempts to replicate the returns the underlying index provides, whereas an actively managed mutual fund strives to surpass its underlying benchmark. The low expense ratio of an index fund is one of its main unique selling points (USPs). The expense ratio is a small portion of the fund’s total assets that the fund house charges for fund management services.

How are Index Funds Different from ETFs?

An exchange-traded fund (ETF) may be traded (bought and sold) easily in the stock market, while index funds can only be traded at the set price point at the end of the trading day. Since ETFs trade like shares of stock on exchanges, they may be easier for retail investors to access and trade. Furthermore, they often charge lower fees and are more tax efficient.

What are the Pros and Cons of Index Funds?

Pros

Cons

Easy diversification

Cannot outperform the market

Little research/knowledge necessary

Lower potential returns

Reduced risk compared to actively managed funds

Little protection from the downside (particularly during bear markets)

Lower costs compared to actively managed funds

No control over fund composition

Which are the Best Index Funds to Invest in India?

S. No.

Index Funds

3-Year CAGR

1

Motilal Oswal Nifty Bank Index Fund Direct-Growth

25.94%

2

UTI Nifty Next 50 Index Fund Direct-Growth

28.64%

3

Nippon India Index S&P BSE Fund Sensex Plan -Direct Plan – Growth Plan

23.08%

4

Motilal Oswal Nifty Smallcap 250 Index Fund Direct-Growth

36.51%

5

UTI Nifty Next 50 Index Fund Direct Growth

19.42%

(Returns as of July 13, 2023. Past performance is no guarantee of future results)

1. Motilal Oswal Nifty Bank Index Fund Direct-Growth

Motilal Oswal Nifty Bank Index Fund Direct Growth has outperformed all other funds in its category during the past three years. It gave CAGR returns of 25.94% over the last 3 years.

The index fund has assets under management (AUM) of ₹403 crores. AUM refers to the current market value of the funds that the mutual fund is managing.

The expense ratio for Motilal Oswal Nifty Bank Index Fund Direct Growth is comparatively low at 0.33%

This index fund saw a 23.7% increase in AUM during the past three months, going from ₹326.48 crore to ₹403.77 crore.

2. DSP Nifty 50 Equal Weight Index Fund Direct Growth

DSP Nifty 50 Equal Weight Index Fund Direct Growth has given a CAGR of 28.64% in the last three years.

It has a low expense ratio of 0.4%.

This is an equity index fund with NIFTY 50 Equal Weight TRI as its benchmark. So an equal amount of your money is invested in the stocks of each company that makes up the index.

Over the last 1 month, DSP Nifty 50 Equal Weight Index Fund Direct Growth has experienced a 15.2% growth in AUM, moving from Rs 500.1 crore to Rs 576.19 crore.

3. Nippon India Index Fund S&P BSE Sensex Plan Direct Growth

Nippon India Index Fund S&P BSE Sensex Plan Direct Growth has given a CAGR of 23.08% over the last three years.

It has one of the lowest expense ratios in the category (index funds) at 0.15%.

Nippon India Index S&P BSE Fund Sensex Plan – Direct Plan – Growth Plan saw a 22.1% increase in AUM during the past three months, going from ₹367.4 crore to ₹448.45 crore.

4. Motilal Oswal Nifty Smallcap 250 Index Fund Direct-Growth

In the last 3 years, Motilal Oswal Nifty Smallcap 250 Index Fund Direct Growth has outperformed all funds in its category giving a CAGR of 36.51%.

The expense ratio for this index fund stands at 0.36%.

Motilal Oswal Nifty Smallcap 250 Index Fund Direct Growth saw a 7% increase in AUM during the past month, going from ₹315.36 crore to ₹337.35 crore.

5. UTI Nifty Next 50 Index Fund Direct Growth

The UTI Nifty Next 50 Index Fund Direct Growth has given a CAGR of 19.42% over the last 3 years.

The expense ratio for this index fund is 0.33%.

Over the last 3 months, UTI Nifty Next 50 Index Fund Direct Growth has experienced a 17.8% growth in AUM moving from ₹1,920 crore to ₹2,260 crore.

Which are the Sector-Specific Index Funds in India?

The objective of sector-based funds is to make investments in companies operating in the same sector or industry. For instance, there are index funds for the banking, IT, pharma, infrastructure, and consumer goods sectors. Typically, these sectoral funds serve broader categories. However, there are index funds with considerably more narrow and specific goals. A PSU bank-only or a private bank-only index fund is an option for investors, whereas a banking sector index fund is focused on the larger banking category.

A few good examples of best sector-specific index funds to invest in would include Aditya Birla Sun Life Banking ETF, ICICI Prudential Bank ETF, Axis Banking ETF in the banking sector, Axis Healthcare ETF, ICICI Prudential Healthcare ETF in the pharma sector, and Kotak IT ETF, SBI-ETF IT in the technology sector.

Benefits of Sector-Specific Investments

Targeted Exposure: Investing in specific sectors allows you to focus on industries you believe will perform well, potentially leading to higher returns.

Expertise and Knowledge: Utilize your understanding of a particular sector to make informed investment decisions and spot opportunities others may miss.

Diversification within a theme: Investing in sectors related to a specific trend or theme (like renewable energy) allows you to diversify while capitalizing on growth in that area.

Risksof Sector-Specific Investments

Concentrated Risk: Putting all your investments in one sector increases vulnerability to industry-specific challenges or downturns, potentially resulting in significant losses.

Volatility: Sector-specific investments tend to be more volatile and sensitive to sector-specific factors.

Limited Diversification: Overemphasizing a single sector may leave you exposed to risks and missed opportunities from other industries.

Regulatory and Legislative Risks: Changes in regulations or laws specific to a sector can impact its performance and profitability.

Should You Choose an Index Fund?

Since Index Funds track a market index, their returns closely resemble those of the index. As a result, these funds are preferred by investors who desire consistent returns and wish to engage in the equity markets without taking on too many risks. In an actively managed fund, the portfolio’s composition is altered depending on the fund manager’s prediction of the potential performance of the underlying securities. This increases the portfolio’s level of risk. Such risks are eliminated by the passive management of index funds. The returns will not, however, be significantly higher than those provided by the index. The best choice for investors looking for greater returns is actively managed equity funds.

Disclaimer: The index funds mentioned in the article are solely for educational purposes. Please do your own research before investing.

In the world of investing, mutual funds have emerged as a popular choice for both seasoned and beginner investors. Mutual funds pool money from multiple investors to create a professionally managed portfolio.

However, navigating the world of mutual funds can be overwhelming without a clear understanding of the common types and terminologies associated with them. This article aims to provide an insightful introduction to mutual funds, its common types, and a few basic terminologies.

What are Mutual Funds?

Mutual funds are professionally managed investment vehicles that pool money from multiple investors. They invest this pooled money in a diversified portfolio of stocks, bonds, or other securities. Investors buy units/shares in the mutual fund. A unit represents proportional ownership. Experienced professionals manage the funds and make investment decisions on behalf of the investors.

This professional management allows investors to benefit from the expertise of seasoned professionals. The Securities and Exchange Board of India (SEBI) regulates the mutual funds industry in India. Mutual funds offer a convenient and cost-effective way for individuals to invest in the financial markets.

Investors can choose from various types of mutual funds, each with specific investment objectives. These types include equity funds, debt funds, liquid funds, balanced funds, index funds, funds of funds, ELSS funds, etc. Investors can easily buy or sell mutual fund shares at the fund’s net asset value.

Types of Mutual Funds

Equity Mutual Funds

Equity Mutual Funds (EMFs) generate returns by investing in stocks of publicly listed companies across market capitalisations (large-cap, mid-cap, and small-cap). They typically generate better returns than fixed deposits (FD) or debt-based funds. EMFs can be theme based, such as emerging markets, dividend yield, energy funds, tax-saving, etc. It can also be sector-based, such as financial services, automobiles, and fast-moving consumer goods (FMCG). The profits and losses generated from EMFs depend solely on the performance of the shares included in them.

Debt Mutual Funds

These funds invest in fixed-income securities such as corporate bonds, treasury bills, commercial papers, and government securities. Such debt instruments have a pre-determined maturity date and interest rate that the buyer can earn at maturity. It can be a preferred choice for passive investors with a low-risk appetite. However, movements in interest rates pose a risk to debt fund investors.

[Interest rate risk is the risk of loss from changing interest rates.]

Liquid Funds

Liquid Funds invest in short-term fixed-income instruments that invest in securities having a maturity of up to 91 days. These funds carry the lowest interest-rate risk in the debt funds category. Liquid funds are an alternative to depositing your money in a savings bank account as it offers better returns.

Index Funds

An Index Mutual Fund tracks a stock market index, such as NSE’s NIFTY50. The fund manager invests in a portfolio of stocks that constitutes an index. Index funds are passively managed funds and have exposure to the constituent securities of an index in the same proportion. It aims to match the returns offered by the underlying index. If you prefer predictable returns, Index funds will be a good choice.

Balanced Funds

Balanced Funds (aka Hybrid Funds) invest in a mix of equity and debt segments in specific ratios. Fund managers keep changing the allocation/ratio based on market risks. These funds often provide the best risk-reward balance and help to maximise the return on investment (RoI).

Fund of Funds

Fund of funds (FoFs) is a type of mutual fund that utilises the money pooled from its clients to invest in various other types of mutual funds available in the market. Thus, the returns of an FoF depend on the performance of the target fund. For example, FOF is used to invest in international funds, a fund that invests in an overseas fund.

Tax Saving Funds (ELSS)

An Equity-Linked Savings Scheme (ELSS) mutual fund helps in saving taxes. It provides the dual advantage of wealth creation and tax saving under Section 80C of the Income Tax Act. By investing in ELSS mutual funds, you can claim a tax exemption of up to ₹1.50 lakh from your annual taxable income. However, ELSS would only be effective under the old regime of taxation.

How do Mutual Funds Work?

1. Creation of the Fund

An asset management company establishes a fund with a specific investment objective, such as growth, income, or a combination of both.

2. New Fund Offer (NFO)

The fund launches an NFO, where it offers units of the fund to investors for subscription. Each unit represents proportional ownership in the fund’s assets. The funds collected during this period are pooled together with investments from other investors.

3. Portfolio Construction

Fund managers create a diversified portfolio by investing the pooled money in a variety of securities, such as stocks, bonds, or money market instruments. The specific asset allocation depends on the fund’s investment strategy.

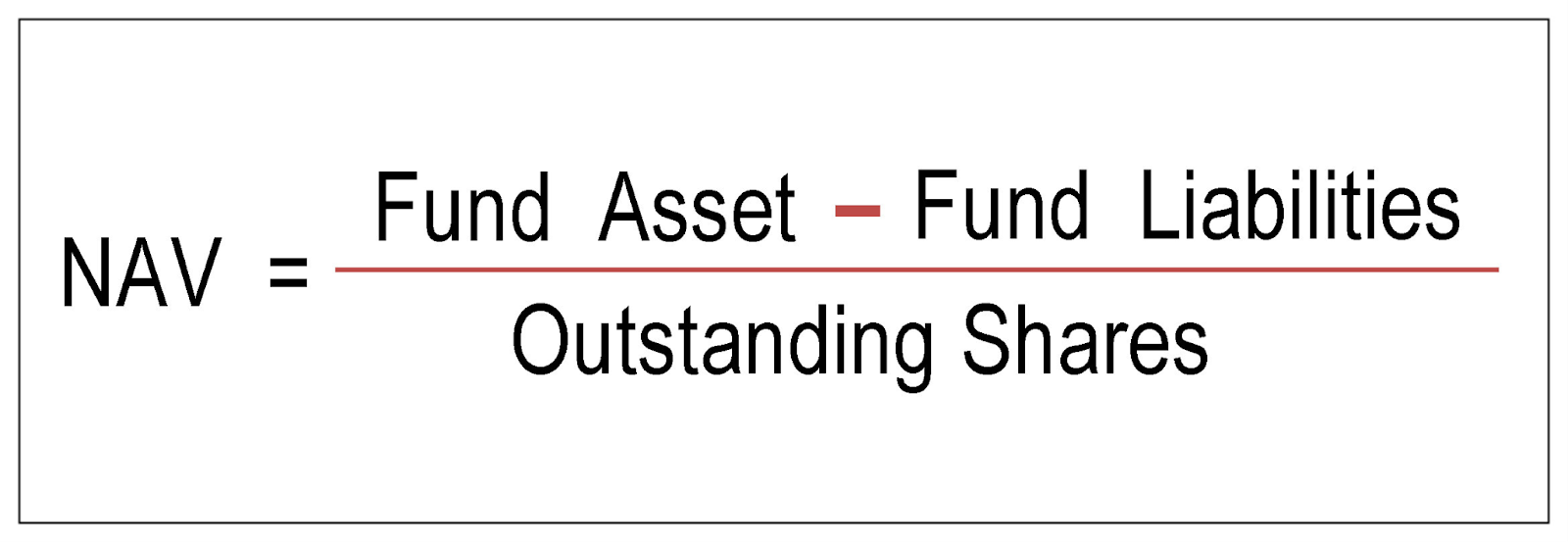

4. Net Asset Value (NAV)

The NAV represents the per-unit value of the mutual fund. is calculated by dividing the total value of the fund’s assets by the number of units outstanding. The NAV is typically calculated at the end of each trading day.

5. Buying and Selling Units

Investors can buy or sell mutual fund units at the NAV price. When investors invest in the fund, they receive units at the current NAV. Similarly, when they sell units, they receive the current NAV value.

6. Expenses and Fees

Mutual funds charge fees and expenses to cover operating costs, including management fees, entry and exit loads, etc. These fees are typically expressed as an expense ratio and deducted from the fund’s assets.

7. Distribution of Profits

Mutual funds may distribute profits to unit holders as dividends or capital gains. These distributions are typically made periodically, depending on the fund’s policy.

8. Performance Monitoring

Investors can track the performance of their mutual fund investments through regular updates provided by the fund. Performance is measured by comparing the fund’s returns against relevant benchmarks or indices.

9. Ongoing Management

Fund managers continuously monitor the fund’s investments, making adjustments as needed to align with the fund’s objectives or market conditions.

Common Terminologies in Mutual Funds

Asset Management Company

An AMC is a company registered with the Securities and Exchange Board of India (SEBI) that handles a mutual fund’s asset management and investment decisions. The top AMCs in India include SBI Mutual Fund (MF), ICICI Prudential MF, HDFC Mutual Fund, Aditya Birla Sun Life MF, Nippon India MF, and Axis MF.

New Fund Offer (NFO)

Asset Management Companies launch New Fund Offers (NFOs) to issue units of their new mutual fund schemes. The Units are similar to shares issued by companies during an initial public offering (IPO). Through an NFO, investors can purchase units of a mutual fund at the subscription price. The offer price is usually ₹10 per unit. Funds are launched via NFOs for a limited time, following which they are traded in the market based on their corresponding net asset value.

Before applying to an NFO, make sure to review the past performance of the AMC and the fund manager. Also, ensure that the fund matches your investment strategy and risk appetite.

Net Asset Value

Net Asset Value, or NAV, is the price of each mutual fund unit. It is the weighted average value of the stocks and other assets in the scheme/portfolio. It is calculated by deducting the liabilities from the total asset value and dividing it by the number of shares. NAV is calculated at the end of each trading day.

NAV is not an indicator of the future prospects of a scheme. Moreover, a mutual fund with a lower NAV does not mean it is not performing well when compared to a fund with a higher NAV.

Open-Ended and Closed-Ended Funds

Open-Ended Funds are mutual funds whose units are open for purchase and redemption at any time. There are no limits on the duration and amount a person can invest. All transactions of such fund units are done at the prevailing NAVs. Open-ended funds are ideal for those who want liquidity in their investments, as they are not bound to any maturity period.

Closed-Ended Funds are funds where investors can purchase units only during the initial offer period (NFO). The units can be redeemed at the specified maturity date.

Interval funds are a cross between open-ended and close-ended funds. It allows transactions at specific periods. Investors can choose to purchase or redeem their units when a trading window opens.

Expense Ratio

The expense ratio is the annual maintenance charge levied by mutual funds to finance their expenses. It includes the annual operating costs, including management fees, allocation charges, and advertising costs of the fund.

Entry Load and Exit Load

Entry Load is the amount payable by an investor while joining a mutual fund. Recent SEBI regulations have removed the entry load from the calculations of the total expense ratio of a mutual fund.

Exit load is the amount payable when an investor chooses to withdraw from a mutual fund. This charge is payable on the total investment of an individual, usually standing at 1%. It serves as a tool to discourage people from withdrawing funds from a mutual fund and encourages them to stay invested for the long term.

Advantages of Investing in Mutual Funds

A few advantages of investing in Mutual Funds are:

Diversification: Mutual funds offer a diversified portfolio of investments, reducing the impact of individual stock or bond fluctuations.

Professional Management: Experienced fund managers make investment decisions on behalf of investors, leveraging their expertise and research capabilities.

Accessibility: Mutual funds provide easy access to a wide range of investment opportunities, even for small investors, with low minimum investment requirements.

Liquidity: Investors can buy or sell mutual fund shares at the fund’s net asset value on any business day, providing liquidity and flexibility.

Transparency: Mutual funds disclose their holdings regularly, allowing investors to review the investments made on their behalf.

Regulations: SEBI regulates the Mutual funds industry in India. SEBI ensures investor protection and adherence to investment guidelines.

Convenience: Investors can rely on professional management, avoiding the need for extensive research and monitoring of individual securities.

Choice of Investment Objectives: Mutual funds offer a variety of investment objectives, catering to different risk appetites and financial goals.

Dividend Reinvestment: Many mutual funds offer the option to reinvest dividends automatically, compounding returns over time.

Risks and Challenges of Investing in Mutual Funds

A few of the risks and challenges of investing in Mutual Funds are:

Market Risk: Mutual funds are subject to market fluctuations, and the value of investments can go up or down.

Lack of Control: Investors have limited control over the specific securities chosen by the fund manager.

Fees and Expenses: Mutual funds charge various fees, including entry and exit loads, which can impact overall returns.

Underperformance: Despite professional management, mutual funds can underperform their benchmarks or other investment options.

Over diversification: Some mutual funds may become overly diversified, diluting potential returns and making it harder to outperform the market.

Style Drift: The fund manager might deviate from the stated investment strategy, leading to a mismatch with investor expectations.

Market Timing Risk: If investors try to time their entry or exit from a mutual fund, they may miss out on potential gains or incur losses.

How to Choose the Right Mutual Fund?

Choosing the right mutual fund requires careful consideration of several factors.

Investment goals: Decide whether you seek growth, income, or a balanced approach.

Risk tolerance: Understand how much risk you are comfortable with.

Fund Performance: Look for consistent returns over time and compare against benchmarks.

Expense ratio: Lower expenses can positively impact your overall returns.

Evaluate the fund manager: Assess their experience, track record, and investment philosophy.

Diversification: Look for funds with a diversified portfolio to reduce risk.

Read the prospectus: Understand the fund’s investment strategy and potential risks.

Minimum investment and fees: Consider if the fund’s requirements align with your budget.

Comparison with Benchmarks: Measure the fund’s performance against relevant indices.

Seek professional advice: Consult a financial advisor for guidance and expertise if needed.

What is NAV in Mutual Funds?

Net Asset Value, or NAV, is the price of each mutual fund unit. It is the weighted average value of the stocks and other assets in the scheme/portfolio. It is calculated by deducting the liabilities from the total asset value and dividing it by the number of shares. NAV is calculated at the end of each trading day.

NAV is not an indicator of the future prospects of a scheme. Moreover, a mutual fund with a lower NAV does not mean it is not performing well when compared to a fund with a higher NAV.

How to Invest in Mutual Funds?

You can invest in mutual funds online through a broker. A trading & demat account is not necessary to invest in mutual funds. However, it is useful if you have one. Platforms such as Zerodha Coin and Groww offer mutual funds. You can also set Systematic Investment Plans (SIPs) on these platforms.

What is Direct Mutual Fund & How to Buy Mutual Funds?

Direct mutual funds allow investors to purchase units from the mutual fund company directly. This bypasses intermediaries like brokers or distributors. These funds do not charge any distribution or commission fees, resulting in lower expense ratios compared to regular mutual funds. With direct mutual funds, investors can potentially earn higher returns over time due to the lower expenses.

You can buy direct mutual funds through Zerodha Coin.

Which Mutual Funds Come Under Tax Benefits?

An Equity-Linked Savings Scheme (ELSS) mutual fund comes with tax benefits. It provides the dual advantage of wealth creation and tax saving under Section 80C of the Income Tax Act. By investing in ELSS mutual funds, you can claim a tax exemption of up to ₹1.50 lakh from your annual taxable income. However, ELSS would only be effective under the old regime of taxation.

We would like to remind our readers to invest in mutual funds only after thoroughly understanding the objectives, theme, expenses, and risks involved. Ensure that the strategy deployed by the fund manager aligns with your investment goals. HAPPY INVESTING!

Another week, another IPO! Aditya Birla Sun Life AMC has launched its three-day initial public offering (IPO) today— Sept 29. It will be the fourth major fund house to list on the Indian stock exchanges. Let us dive into the details surrounding the company and its IPO.

Company Profile – Aditya Birla Sun Life AMC Ltd

Aditya Birla Sun Life AMC is the largest non-bank affiliated asset management company (AMC) in India in terms of quarterly average assets under management (QAAUM).It is a joint venture between Aditya Birla Capital Ltd and Sun Life (India) AMC Investments Inc. An AMC pools funds from clients and invests them into various financial instruments such as stocks, bonds, real estate units, etc. Established in 1994, ABSL AMC has a well-diversified product portfolio with innovative schemes. It manages equity schemes, debt schemes, liquid schemes, exchange-traded funds (ETFs), and domestic fund-of-funds (FoFs).

ABSL AMC has automated and digitised several aspects of its operations, including customer onboarding, online payments, fund management, accounting, and data analytics. However, the company is highly dependent on third-party channels for the distribution of its mutual funds. It is a well-recognized and trusted brand with experienced promoters. You may have come across their offerings while analysing mutual fund schemes.

Factsheet

The company had a total AUM of Rs 2.93 lakh crore under its suite of mutual funds (excluding domestic FoFs), portfolio management services, offshore and real estate offerings as of June 2021.

Since its inception, ABSL AMC has established an extensive pan-India presence, covering 284 locations. It has over 240 national distributors and ~100 bank/financial intermediaries.

As of June 30, 2021, the AMC managed a total of 118 schemes— 37 equity schemes, 68 debt schemes, two liquid schemes, five ETFs, and six domestic FoFs. In addition, the company manages a total AUM of ~Rs 11,515 crore as part of its portfolio management services and offshore real estate offerings.

The company’s monthly average assets under management (MAAUM) from institutional investors stood at Rs 1.503 lakh crore as of June 30, 2021, and was the fourth-largest amongst its peers.

About the IPO

Aditya Birla Sun Life AMC’s public issue opens on September 29 and closes on October 1. The company has fixed Rs 695-712 per share as the price band for the IPO.

The offer for sale (OFS) of up to 3.88 crore equity shares from existing shareholders aggregates to Rs 2,768.26 crore. Individual investors can bid for a minimum of 20 equity shares (1 lot) and in multiples of 20 shares thereafter. You will need a minimum of Rs 14,240 (at the cut-off price) to apply for this IPO. The maximum number of shares that can be applied by a retail investor is 280 equity shares (14 lots).

The main objective of the IPO is to provide an exit strategy (or liquidity) to ABSL AMC’s shareholders and early investors. Thus, the company is not raising any funds through the public issue. It aims to achieve the benefits of listing the equity shares on NSE and BSE. The total promoter holding in the company will decline from 100% to 86.5% post the IPO.

Financial Performance

From the table, it is clear that ABSL AMC has been reporting growth in profits despite declining revenues. The surge in profits can be attributed to declining fees and commission expenses every once in a while. The company’s revenue from operations rose 29.85% quarter-on-quarter (QoQ) to Rs 333.24 crore in the April-June quarter (Q1 FY22). Meanwhile, the profit attributable to owners increased by 59.15% QoQ to Rs 154.94 crore during the same period.

The company’s market-leading position across categories, product mix, and scale have contributed to a strong financial performance. Aditya Birla Sun Life AMC is the third-largest AMC in terms of total income and had the highest Return on Net Worth (RoNW) of 30.87% in FY21. RoNW signifies how well the company uses shareholders’ capital to generate profits.

Risk Factors

The company’s revenue and profits are dependent on the assets under management (AUM) of their schemes. Any adverse changes in AUM can result in poor financial performance.

The extent of the impact of Covid-19 on its operations is highly uncertain and unpredictable. High volatility in stock markets could cause investors to reduce their investments in the funds managed by ABSL AMC and eventually reduce its AUM.

The underperformance of ABSL AMC’s investment products could lead to loss of investors and a reduction in AUM. The company’s business would be severely affected if they are unable to retain investors.

Unfavourable interest rates, defaults, and credit risk related to the debt portfolio of funds may expose the company’s funds to losses. Similarly, any unfavourable investment opportunities and poor economic conditions could restrict AUM growth.

ABSL AMC’s historical growth rates may not be indicative of its future growth. The company’s overall performance would be adversely affected if it does not successfully implement business plans.

The company’s business is subject to extensive regulation, including periodic inspections by SEBI. Non-compliance with existing regulations or the failure to obtain and renew regulatory approvals could expose ABSL AMC to penalties.

IPO Details in a Nutshell

The book-running lead managers to the public issue are Axis Capital, BofA Securities India, Citigroup Global Markets India, HDFC Bank, ICICI Securities. Other lead managers include Kotak Mahindra Capital, Motilal Oswal Investment Advisors, SBI Capital Markets, and IIFL Securities. Aditya Birla Sun Life AMC Ltd had filed draft papers for its IPO in November 2020. You can read it here.

Ahead of the IPO, the company raised Rs 788.95 crore from anchor investors. The marquee investors include HSBC, International Monetary Fund, Abu Dhabi Investment Authority, Morgan Stanley Asia, BNP Paribas, and Societe Generale.

Conclusion

Aditya Birla Sun Life AMC caters to a wide range of retail investors, high net-worth individuals (HNIs), and institutions through its vast network. It has maintained a market-leading position in B-30 (beyond top 30 cities) penetration over the years. This factor has contributed to the growth of its investor base as well as improvement in profitability. The Indian mutual fund industry’s overall AUM is projected to sustain a higher growth trajectory of 11-13% CAGR to reach Rs 57 lakh crore by 2026. The industry is witnessing a significant increase in net inflows from investors every month. The company is well-positioned to attract a large segment of the Indian mutual fund market that varies across customer requirements and risk profiles.

ABSL AMC will be directly competing with leading players such as HDFC AMC, Nippon Life AMC, and UTI AMC once it gets listed. There is scope for asset management companies to grow even further.

Before applying for the IPO, we will wait to see if the portion reserved for institutional investors gets oversubscribed. The company’s IPO shares were trading at a premium of Rs 27 in the grey market today. As always, make sure you carefully weigh out the pros and cons of the company and come to your own conclusion.

What are your opinions on this IPO? Will you be applying for it? Let us know in the comments section of the marketfeed app.

As of late, we have noticed that many of our readers are confused about how to start their investment journey. The primary motive behind investing your hard-earned income is to fight inflation or a general rise in the prices of goods. The purchasing power of cash in hand or your bank account continuously reduces with time. In order to beat inflation and achieve future goals, you need to invest your money in a variety of financial products.

Our primary mission here at marketfeed is to show the path for every individual to become financially independent. We help you make informed decisions in the beautiful world of finance. However, it is important that we start from the very basics and slowly work our way up. So, let us have a clear understanding of some of the best investment options that can help you achieve financial freedom.

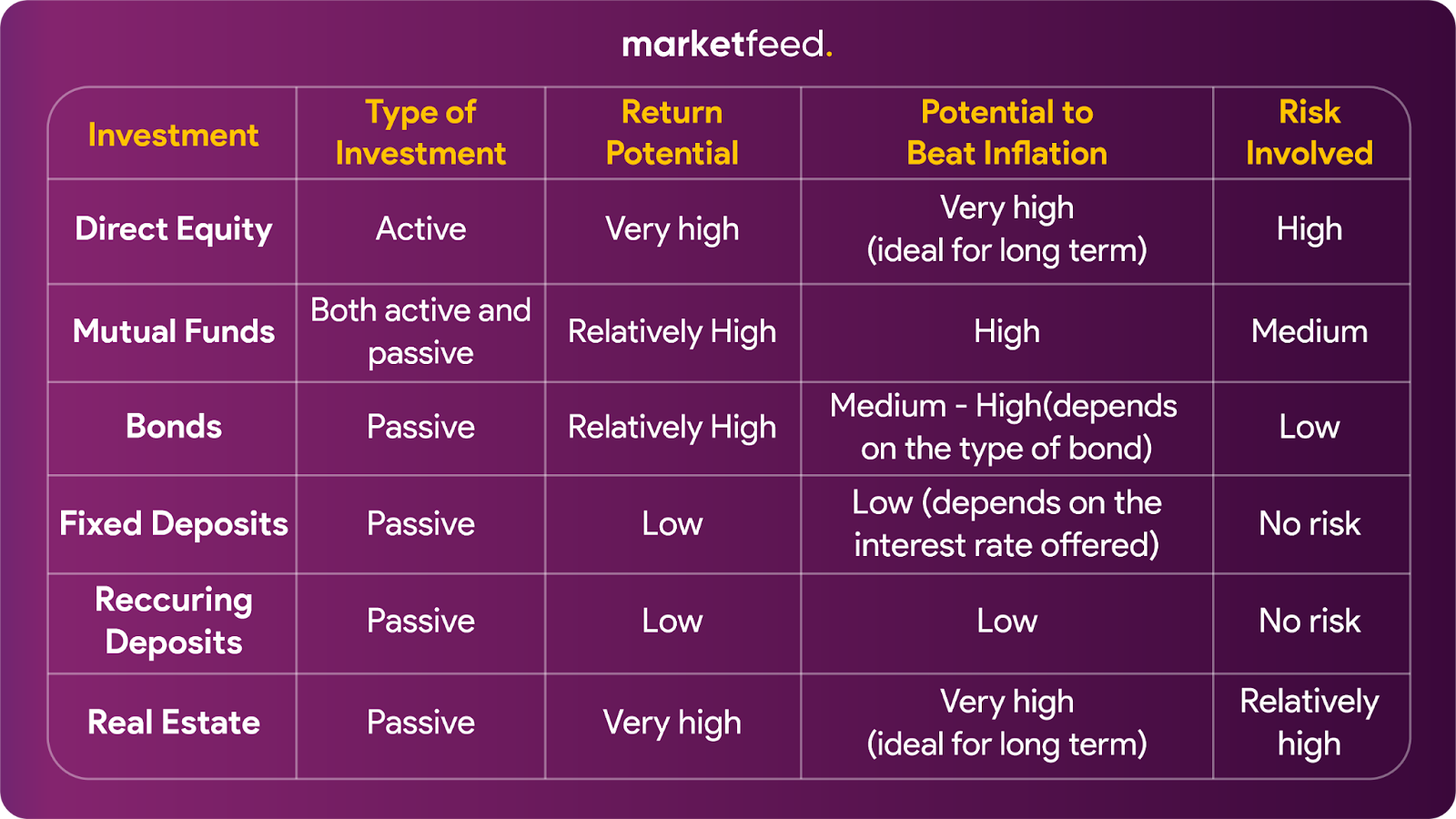

Direct Equity

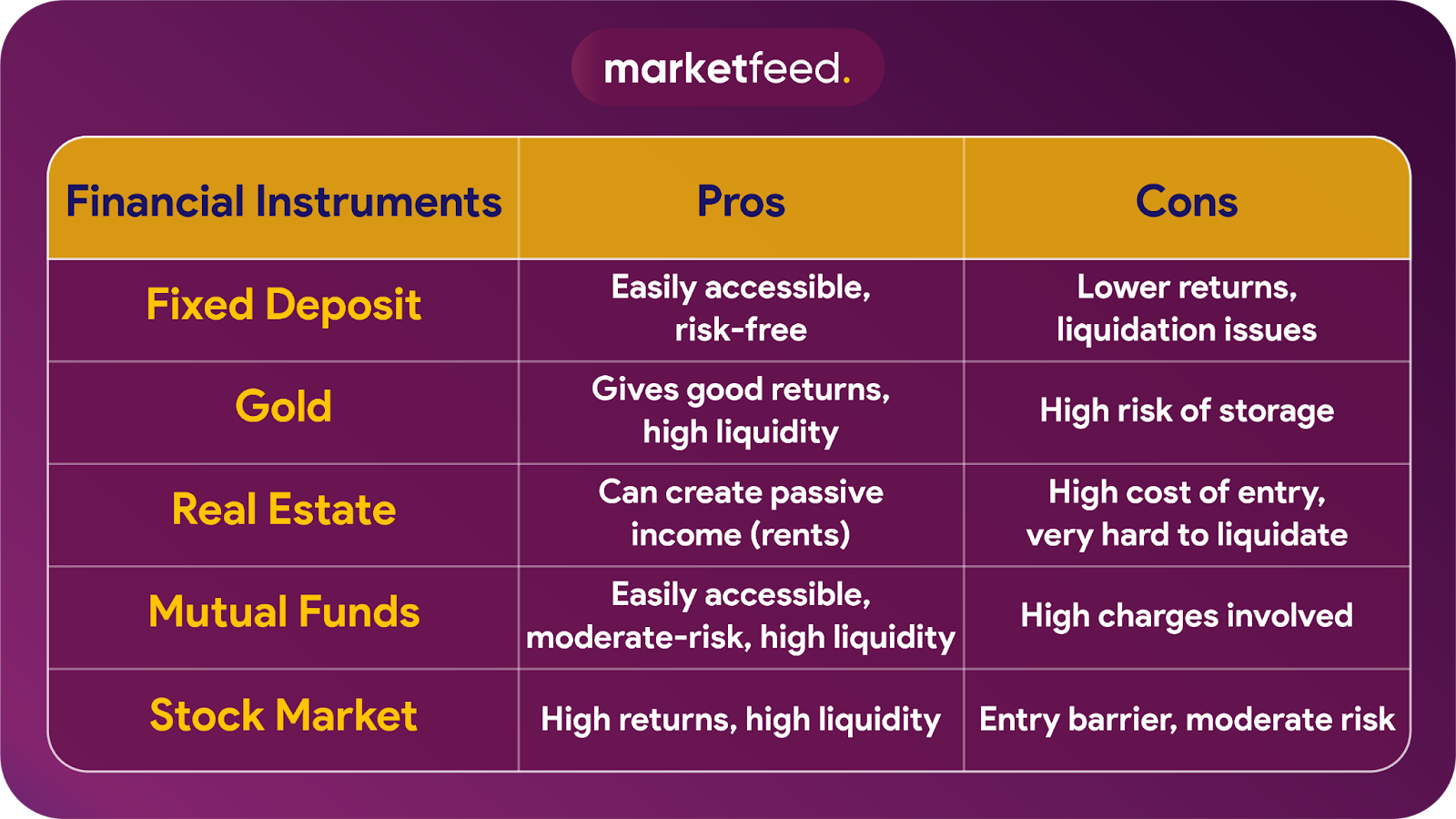

Direct equity means investing in stocks. When you buy stocks (or shares) of a listed company, you become part-owner of the firm (even though it’s a very tiny fraction). This means that you are directly investing in the company’s development and growth. In the long run, stock markets have always beaten inflation and have delivered higher returns than other asset classes. Thus, stocks are always ideal for long-term investments. To directly invest in shares or equity, you would need to open a Demat account.

However, investing in stocks contains a high level of risk. Stock markets are often very volatile, as a variety of factors (including interest rates, government policies, economic figures, company operations) influence the performance of stocks. You will have to actively manage your investments to limit losses. One needs to have a lot of patience and gain market knowledge to get sufficient returns. With time, you will learn how to pick the right stock and time your entry and exit. Target-oriented and well-researched stock market investments can definitely help you beat inflation.

Mutual Funds

If you are not comfortable with investing directly in stocks due to the risks involved, you can always invest in mutual funds. A mutual fund takes money (investments) from different individual and institutional investors who have a common investment objective. This pooled sum of money is managed by a professional fund manager, who invests in securities and assets to generate returns for investors.

You can find equity, debt and hybrid mutual funds as a general classification. Equity mutual funds invest in stocks and equity-related instruments, while debt mutual funds invest in bonds and other debt instruments. Hybrid mutual funds invest in a mix of equity and debt instruments. There are various equity mutual funds based on market capitalization, tax-saving funds, sectoral funds, and much more. As per reports, the 5-year and 10-year returns of these equity fund categories were above 10% as of April 2021.

Mutual funds are a very attractive investment option as you do not have to spend much time and effort tracking them. Instead of investing a large sum of money all at once, you could start a Systematic Investment Plan (SIP) and invest small amounts of money periodically (usually every month) in mutual funds. They are very flexible, as you can begin and stop investing according to your convenience. However, one needs to conduct a proper analysis or study before investing in a particular mutual fund. Element of risk is also present as the returns are dependent on market movements.

Bonds

A bond is a fixed-income instrument issued by companies or even government entities to raise funds. Investors can lend their money to organisations in return for fixed yearly interest. At the time of maturity of the bond, you will receive the initial money you had invested and the interest offered on it. Nowadays, bonds offer fixed returns that are at least 2-3% higher than fixed deposits (FDs). Government bonds in India are an ideal investment option as it provides more than 7% guaranteed returns.

Before investing in bonds, you need to consider and analyse important factors such as coupon rate (fixed interest that the bond pays annually), payment frequency (the number of times the interest is paid to the bondholder), maturity date, and credit rating. A higher-rated bond carries a higher level of safety of investment. AAA-rated bonds are the most secure.

Gold

Gold is one of the best asset classes that can be used to counter inflation. This is because the increase in gold prices and the returns from it have always been able to offset inflation in the past. According to the World Gold Council, for every 1% increase in inflation, there is a 2.6% rise in gold demand. This ultimately leads to an increase in gold prices. However, acquiring and holding gold in the form of jewellery has its own concerns such as safety and high cost.

An alternative way of owning gold is through paper gold or gold ETFs. These are units representing physical gold which may be in paper or dematerialised (electronic) form. One Gold ETF unit is equal to 1 gram of gold and is backed by physical gold of very high purity. The investments made in paper gold are less costly.

What are ETFs?

As the name suggests, an exchange-traded fund (ETF) is a fund that can be traded on the stock exchange. It is a method through which you can buy and sell a basket of assets without having to buy all the components individually. ETFs are managed by finance professionals who own certain underlying assets (such as stocks, bonds, currencies, and commodities). They design a fund to track the performance of these assets and then sell shares of these funds to investors.

ETFs are a great method to diversify your portfolio and manage risks. It is also a cost-effective method of investing and also offers several tax benefits.

Fixed Deposits, Recurring Deposits

Fixed Deposits (FDs) are an investment option offered by banks and financial institutions. It is something that most of us are familiar with. You deposit a lump sum of money for a fixed period and earn a predetermined rate of interest on it. The interest rate of FDs differs from one bank to another. However, the average rate of FDs in India is only 5-6%, which may be insufficient to beat inflation. FDs are favorable for those investors who wish to receive guaranteed, yet conservative returns.

Recurring Deposits (RDs) are a fixed-tenure investment option provided by banks and other institutions that allow individuals to invest a fixed amount every month for a pre-defined time period. The interest rate on RDs is determined by the institution offering them. RDs also offer complete capital protection as well as guaranteed returns.

Government Schemes

Public Provident Fund (PPF) is a long-term investment scheme provided by the Government of India (GoI) that has a lock-in period of 15 years. Currently, the annual rate of interest offered on PPF is 7.10%. The entire amount withdrawn at the end of the 15 years is entirely tax-free for the investor. You can also take loans and make partial withdrawals if certain conditions are met.

Employee Provident Fund (EPF) is a retirement-oriented investment scheme that helps salaried individuals. EPF deductions are a specific percentage of your salary every month, and the same amount is matched by the employer as well. This entire amount is pooled into your EPF corpus or account every month, and you receive interest on it. Currently, the annual rate of interest offered on EPF is 8.50%. At the time of maturity, the entire amount withdrawn from the EPF corpus is entirely tax-free.

The National Pension Scheme (NPS) is another tax-saving investment option offered by the Government of India. Anyone between the age of 18-65 years can make voluntary contributions to this scheme. Investors who subscribe to NPS will mandatorily stay locked in until their retirement and can earn better returns than PPF or EPF. Historically, NPS has delivered ~8-10% returns every year.

Real Estate

Investing in real estate is one of the best ways to diversify your portfolio. Since the value of a real estate property appreciates (or increases) with time, you can earn exponential returns on it. Acquiring a property and renting it out would be an ideal way to earn passive income. However, the location of the property is the most important factor that will determine its value and also the rental income that can be earned from it. In the case of residential properties, investors must always conduct a thorough study of home loan interest rates, offers provided by developers, and government regulations. Another important factor to consider is that real estate is highly illiquid. Properties cannot be sold off and converted into cash quickly.

If you don’t have adequate capital for acquiring real estate properties, you could always invest in a real estate investment trust or REIT. This is very similar to a mutual fund, wherein you can invest small amounts of money on certain income-generating assets and earn a good return from them. A REIT owns and operates several properties such as complexes, infrastructure projects, healthcare units, apartments, and more. The money pooled in from the REIT is used to manage these assets. And, the income derived from these properties or assets is shared among all investors (or unitholders) of the REIT.

Types of Investments in a Nutshell

Conclusion

Now, you have an idea of how to grow your hard-earned income to beat inflation and lead a better life. However, it is up to you to figure out the right investment that fits your profile and financial goals. Start your investment journey only after carefully going through the risks and costs associated with each of them. Go for those investments that you clearly understand from your own research. At the same time, it is vital that you invest your money in different products and diversify your portfolio. More importantly, make sure you do not fall for scammy schemes that promise high returns in a short period. The sooner you start investing, the longer you will stay invested and earn higher returns.